Alibaba’s Birthday Bash Announcement, Anti-Involution Comes to Restaurant Delivery

5 Min. Read Time

| Upcoming Live Webinar |

| Join us Thursday, September 11th, at 10:30 am EDT for: China, Land of Breakthroughs? A Conversation With Gavekal’s Louis-Vincent Gave Please click here to register |

Key News

Asian equities ended mixed today, as Hong Kong, Taiwan, and South Korea outperformed amid a weaker US dollar backdrop.

The renminbi (CNY) appreciated to 7.12 against the dollar in a steady rally from April's low of 7.34 (since CNY is quoted $1 in CNY, a lower value means appreciation).

Alibaba surged +3.35% on extremely high volume, with 181 million shares traded, far above the one-year average of 102 million, driven by reports that its “word of mouth” consumer review platform, group buying initiative, and AutoNavi digital map service will be merged into a new local services push. The stock’s recent gains follow strong AI and cloud-driven financial results and further momentum from its new Qen3-Max-Preview AI model. Yesterday, rumors circulated that a new Alibaba business group will occupy a previously unused building on its new Hangzhou campus. Tomorrow marks Alibaba’s 26th anniversary, with a press conference scheduled, heightening speculation about a major restructuring.

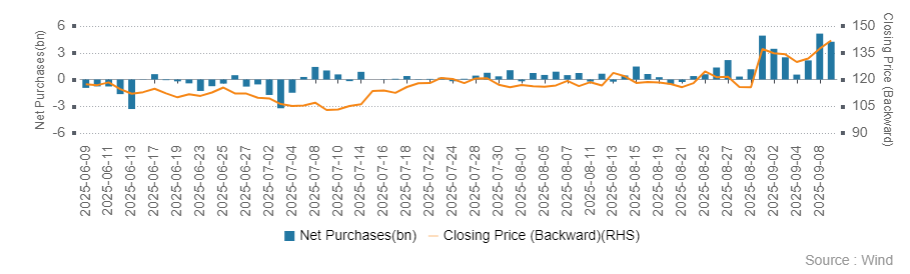

Alibaba topped the charts for trading value today, at levels five times higher than before September 2024’s stimulus announcement. Mainland investors continue to accumulate the stock via Southbound Stock Connect, as shown in the attached chart.

The State Administration for Market Regulation (SAMR) addressed the escalating “race to the bottom” in food delivery subsidies, urging companies to “resist vicious subsidies” and “end unfair competition.” SAMR announced meetings with firms in this sector, though meaningful action still appears limited. JD.com’s (+3.32%) entry has increased pressure, hurting peers like Meituan (-2.3%), which hit a 52-week low. Despite the price war’s negative impact on sector profits, SAMR's commitment to “closely monitor competition” may signal a shift.

Tencent gained +1.54% amid reports it may issue a third US dollar bond as existing bonds mature in January and April 2026. The potential offering is seen as a proxy for Tencent’s prospects and renewed foreign investor interest in China assets. Baidu slipped -0.09% after issuing a $618 million US dollar bond and unveiling upgraded AI models. Reports suggest Alibaba and Baidu could become Apple’s China AI partners.

Alibaba Health climbed +10.02% to a 52-week high of HKD 7.14, though remains "slightly below" its all-time peak of HKD 30.15. Healthcare subsectors were mixed. Non-ferrous and precious metals led gains in Hong Kong and China markets, while real estate rallied on speculation that Shenzhen may ease home-buying rules.

Mainland China opened higher but surrendered gains as technology hardware, semiconductors, electrical equipment, and telecom stocks lagged. SMIC fell -10.26% after announcing a share issuance to fund its acquisition of SMIC North, a move seen as dilutive.

Apple’s upcoming iPhone launch has weighed on expectations for local tech. Notably, clean technology was subdued despite Vice President Han Zheng’s remarks at the 2025 Global Energy Interconnection Conference, emphasizing renewable energy’s importance.

Alibaba’s Hong Kong stock price and net flow from Southbound Stock Connect:

Last Night's Performance

| Country / Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 1.2% |

| Hang Seng Tech | HSTECH Index | 1.3% |

| Hong Kong Turnover | HKTurn Index | 2.8% |

| Hong Kong Short Sale Turnover | HKSST Index | 22.7% |

| Short Turnover as a % of Hong Kong Turnover | N/A | 15.9% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 1306.66 |

| China (Shanghai) | SHCOMP Index | -0.5% |

| China (Shenzhen) | SZCOMP Index | -1.1% |

| China (STAR Board) | Star50 Index | -2.4% |

| Mainland Turnover | .chturn Index | -12.5% |

| Northbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0.3% |

| Japan | NKY Index | -0.4% |

| India | SENSEX Index | 0.4% |

| Indonesia | JCI Index | -1.8% |

| Malaysia | FBMKLCI Index | 0.1% |

| Pakistan | KSE100 Index | 0.5% |

| Philippines | PCOMP Index | 0.3% |

| South Korea | KOSPI Index | 1.3% |

| Taiwan | TWSE Index | 1.3% |

| Thailand | SET Index | 0.8% |

| Singapore | STI Index | -0.3% |

| Australia | AS51 Index | -0.5% |

| Vietnam | VNINDEX Index | 0.8% |

| Indicator | Hong Kong | Mainland |

|---|---|---|

| Today's Volume % of 1-Year Average | 127% | 133% |

| Advancing Stocks | 246 | 1103 |

| Declining Stocks | 229 | 3933 |

| Outperforming Factors | Growth, Large Cap, Buybacks | Multi Factor Score, Value, Dividend Yield |

| Underperforming Factors | Liquidity, Growth, Momentum | |

| Top Sectors | Real Estate, Staples, Materials | Real Estate, Materials, Financials |

| Bottom Sectors | Healthcare, Energy, Industrials | Tech, Healthcare, Industrials |

| Top Subsectors | Consumer Staples Distribution, Non Ferrous Metals, REITs | Precious Metals, Motocycle, Real Estate |

| Bottom Subsectors | National Defense, Machinery, Healthcare Equipment | Semis, Internet, Electronic Components |

| Southbound Connect Buys | Alibaba (Very Large), SMIC (Moderate) | |

| Southbound Connect Sells | Xiaomi (Very Large), Meituan (Large), Akeso (Moderate), Tencent (Small) |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | 1.46 |

| Communication Services | 9 | 1.64 |

| Consumer Discretionary | 28 | 1.74 |

| Consumer Staples | 13 | 2.66 |

| Energy | 6 | -0.53 |

| Financials | 24 | 1.46 |

| Health Care | 12 | -0.61 |

| Industrials | 21 | -0.29 |

| Information Technology | 10 | 1.62 |

| Materials | 10 | 2.21 |

| Real Estate | 7 | 3.48 |

| Utilities | 12 | -0.05 |

| Mainland China Listed | 395 | -0.45 |

| Communication Services | 7 | -0.79 |

| Consumer Discretionary | 29 | 0.11 |

| Consumer Staples | 24 | 0.26 |

| Energy | 13 | -0.02 |

| Financials | 64 | 0.65 |

| Health Care | 32 | -1.62 |

| Industrials | 61 | -0.98 |

| Information Technology | 90 | -2.19 |

| Materials | 54 | 0.74 |

| Real Estate | 6 | 0.91 |

| Utilities | 15 | -0.07 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 1.5 |

| Alibaba HK | 9988 HK Equity | 3.4 |

| JD.com HK | 9618 HK Equity | 3.3 |

| NetEase HK | 9999 HK Equity | 1.8 |

| Yum China HK | 9987 HK Equity | -2.2 |

| Baozun HK | 9991 HK Equity | 4.7 |

| Baidu HK | 9888 HK Equity | -0.1 |

| Autohome HK | 2518 HK Equity | 2.1 |

| Bilibili HK | 9626 HK Equity | 5.5 |

| Trip.com HK | 9961 HK Equity | -2 |

| EDU HK | 9901 HK Equity | 5.4 |

| Xpeng HK | 9868 HK Equity | 2 |

| Weibo HK | 9898 HK Equity | -1.9 |

| Li Auto HK | 2015 HK Equity | 3.1 |

| Nio Auto HK | 9866 HK Equity | 1.3 |

| Zhihu HK | 2390 HK Equity | 1.9 |

| KE HK | 2423 HK Equity | 2.4 |

| Tencent Music Entertainment HK | 1698 HK Equity | -1 |

| Meituan HK | 3690 HK Equity | -2.3 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| ALIBABA GROUP HOLDING LTD | 3.4 |

| MEITUAN-CLASS B | -2.3 |

| TENCENT HOLDINGS LTD | 1.5 |

| XIAOMI CORP-CLASS B | 2.6 |

| SEMICONDUCTOR MANUFACTURI-H | 0.2 |

| PING AN INSURANCE GROUP CO-H | 2.1 |

| BYD CO LTD-H | 0.3 |

| KUAISHOU TECHNOLOGY | 4.3 |

| AKESO INC | -1.7 |

| POP MART INTERNATIONAL GROUP | 0.2 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| VISUAL CHINA GROUP CO LTD-A | -3.1 |

| SHANTUI CONSTRUCTION MACHI-A | 3.7 |

| ZHONGJI INNOLIGHT CO LTD-A | -2.9 |

| SUNGROW POWER SUPPLY CO LT-A | -5.2 |

| EOPTOLINK TECHNOLOGY INC L-A | 0.3 |

| SEMICONDUCTOR MANUFACTURIN-A | -10.3 |

| VICTORY GIANT TECHNOLOGY -A | -5.1 |

| WUXI LEAD INTELLIGENT EQUI-A | -2.3 |

| CONTEMPORARY AMPEREX TECHN-A | -1.7 |

| GOTION HIGH-TECH CO LTD-A | 6.4 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.12 versus 7.13 yesterday

- CNY per EUR 8.37 versus 8.36 yesterday

- Yield on 10-Year Government Bond 1.86% versus 1.85% yesterday

- Yield on 10-Year China Development Bank Bond 1.91% versus 1.91% yesterday

- Copper Price -0.03%

- Steel Price +0.29%