PCAOB Arrives in Hong Kong, EU Regulation Sends Solar Stocks Lower

3 Min. Read Time

Key News

Asian equities were mixed but mostly lower overnight as uncertainty surrounding US interest rates continues to pervade global markets.

Today was a reversal of yesterday as Hong Kong managed a gain while Mainland markets declined. According to reports, a team from the US Public Company Accounting Oversight Board (PCAOB) arrived in Hong Kong this week to review the audit books of China-based firms listed in the US from the latest financial year. According to Mainland media reports, China’s banks have been lowering the deposit rates offered to their customers. This makes sense as it is further evidence of the country’s easing policies, to be contrasted with Western countries.

Xi Jinping, India’s Narendra Modi, and Vladimir Putin met at the China-led Shanghai Cooperation Summit in Uzbekistan to discuss a range of topics of global import including the war in Ukraine. China continues to take a neutral outward stance towards the nearly eight-month-old conflict. CNH, China’s currency that trades during US trading hours, has breached the psychologically important level of 7 CNY/USD. This is entirely due to US dollar strength. The People’s Bank of China (PBOC) has been diligently working to keep the exchange rate stable and the central bank has done a decent job as China’s currency has held up better than most other Asian currencies. We believe this exchange rate only means that Chinese assets are trading at an even more attractive discount.

The European Union announced new measures that may prevent the import of solar panels from China’s Xinjiang region. This move sent solar stocks in Mainland China sharply lower overnight, including Sun Grow, which fell by -8.5% overnight. The new EU measures are broad and non-specific, so we cannot be certain of their eventual impact on China’s solar energy stocks. It is important to recall the US’ and EU’s heavy reliance on solar panels produced by China-based manufacturers.

Moderna's CEO said the company is in discussions with China's government about supplying their mRNA vaccine, but no decisions have been made yet. China's local mRNA vaccine is also in development. CSPC Pharmaceutical is expediting its phase III trial of a new mRNA vaccine, which may receive emergency approval for distribution to the Chinese public.

Reuters reported that Biden plans to broaden U.S. export bans on China's semiconductor industry, including Lam Research and Applied Materials. The commerce department sent letters to Nvidia and AMD to ban their export of A.I. chips to China. It is yet to be determined the scope and implementation of this plan. More than 30% of the U.S. semiconductor industry's revenues are derived from sales in China, according to GlobalData. Boston Consulting Group (BCG) estimates that U.S. companies would lose 18 percent of their global market share and 37 percent of their revenues—leading to the loss of 15,000 to 40,000 high skilled domestic jobs—if Washington pursued a hard technological decoupling and completely banned domestic semiconductor companies from selling to Chinese clients.

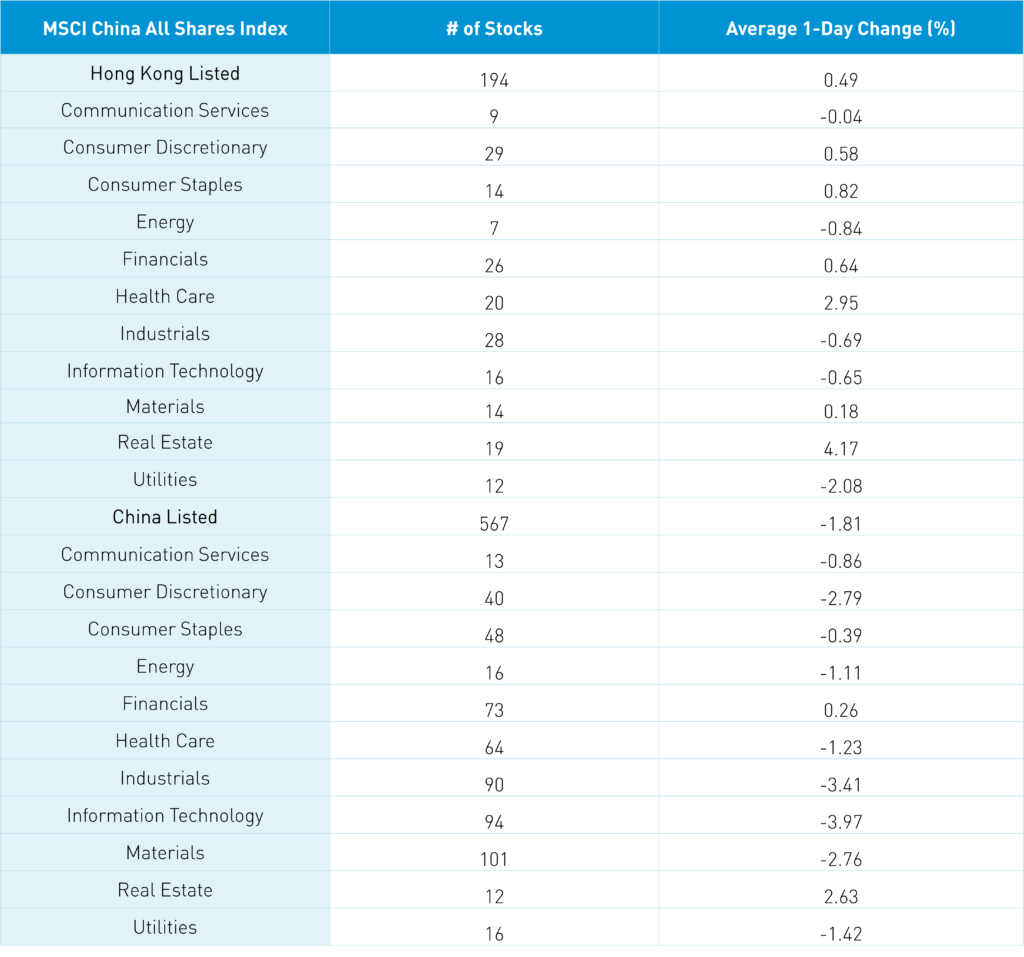

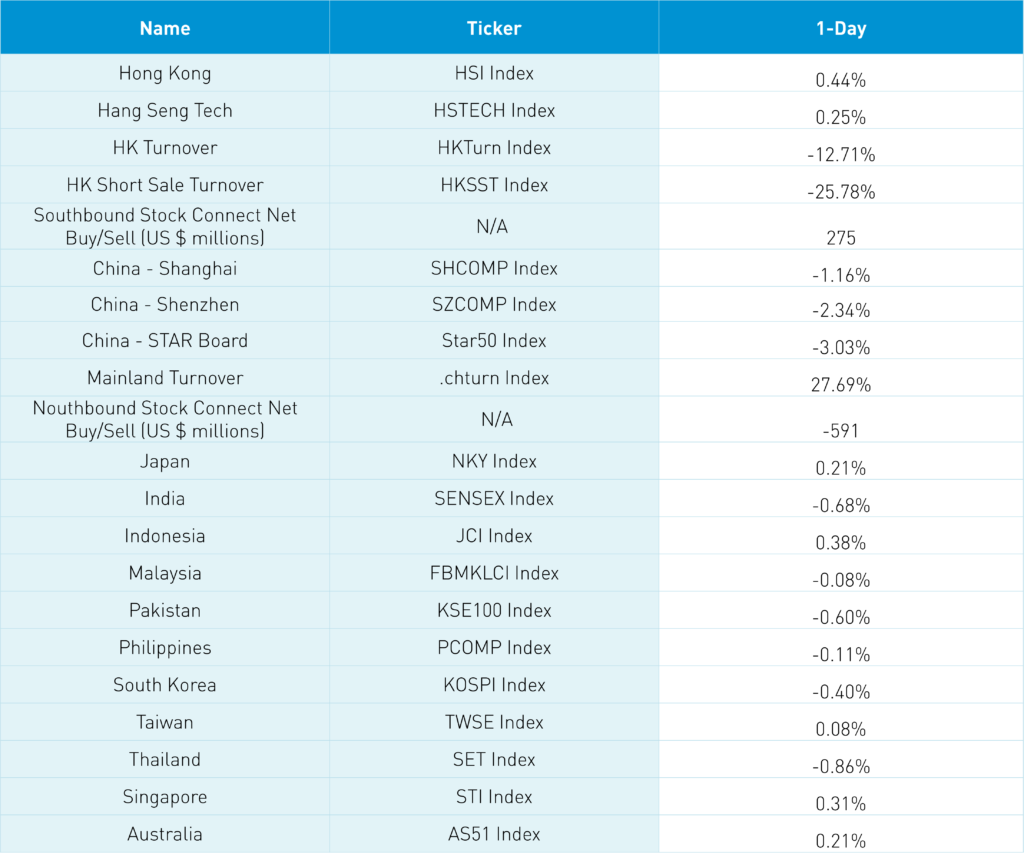

The Hang Seng and Hang Seng Tech gained +0.44% and +0.25% on volume -12.71% from yesterday which is 64% of the 1-year average. 220 stocks advanced while 251 declined. Hong Kong short sale turnover declined -25.78% overnight which is 70% of the 1-year average as short sale trading accounted for 19% of total trading. Growth and value factors were mixed as large caps underperformed large caps. Top sectors were real estate +4.17%, healthcare +2.95%, and staples +0.82% while utilities -2.08%, energy -0.84%, and industrials -0.69%. Top sub-sectors were biotech, property developers, and cement while solar, semis, and wind were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought $275 million of Hong Kong stocks with Wuxi Biologics being a large buy for the third day while Tencent and Meituan were small net buys.

Shanghai, Shenzhen, and STAR Board fell -1.16%, -2.34%, and -3.03% respectively on volume +27.69% from yesterday which is 90% of the 1-year average. Only 495 stocks advanced while 4,112 declined. Real estate and financials gained +2.69% and +0.32% while tech -3.91%, industrials -3.35%, and discretionary -2.73%. Top sub-sectors were real estate related, finance related such as insurance, and coal mining while solar, battery, semis, and auto parts were among the worst. Foreign investors sold -$591 million of Mainland stocks today via Northbound Stock Connect. CNY declined -0.45% versus the US dollar to 6.99 from 6.95, Treasuries were flat, and copper off -0.32%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.99 versus 6.96 yesterday

- CNY/EUR 6.98 versus 6.96 yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 2.82% versus 2.82% yesterday

- Copper Price -0.32% overnight