Mainland Investors Ask Foreign Investors “Do You See What I See?”

4 Min. Read Time

Key News

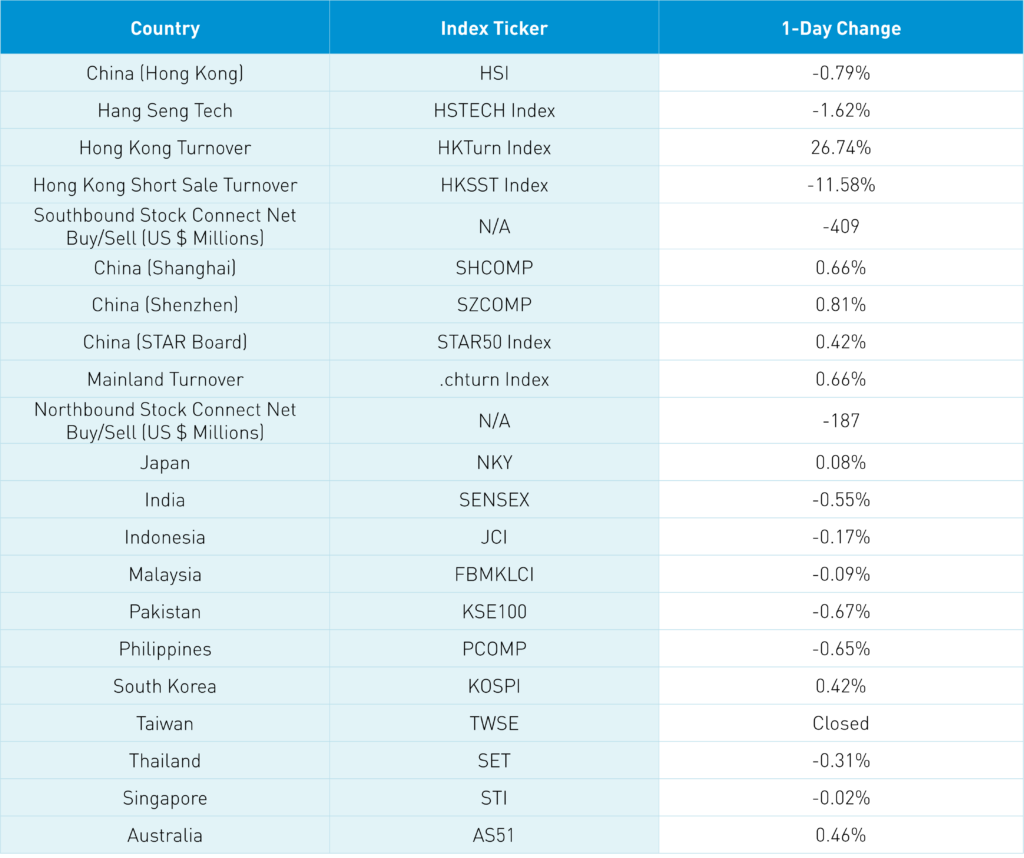

Asian equities were largely lower with China and South Korea managing to close positive while Taiwan was off for Peace Memorial Day.

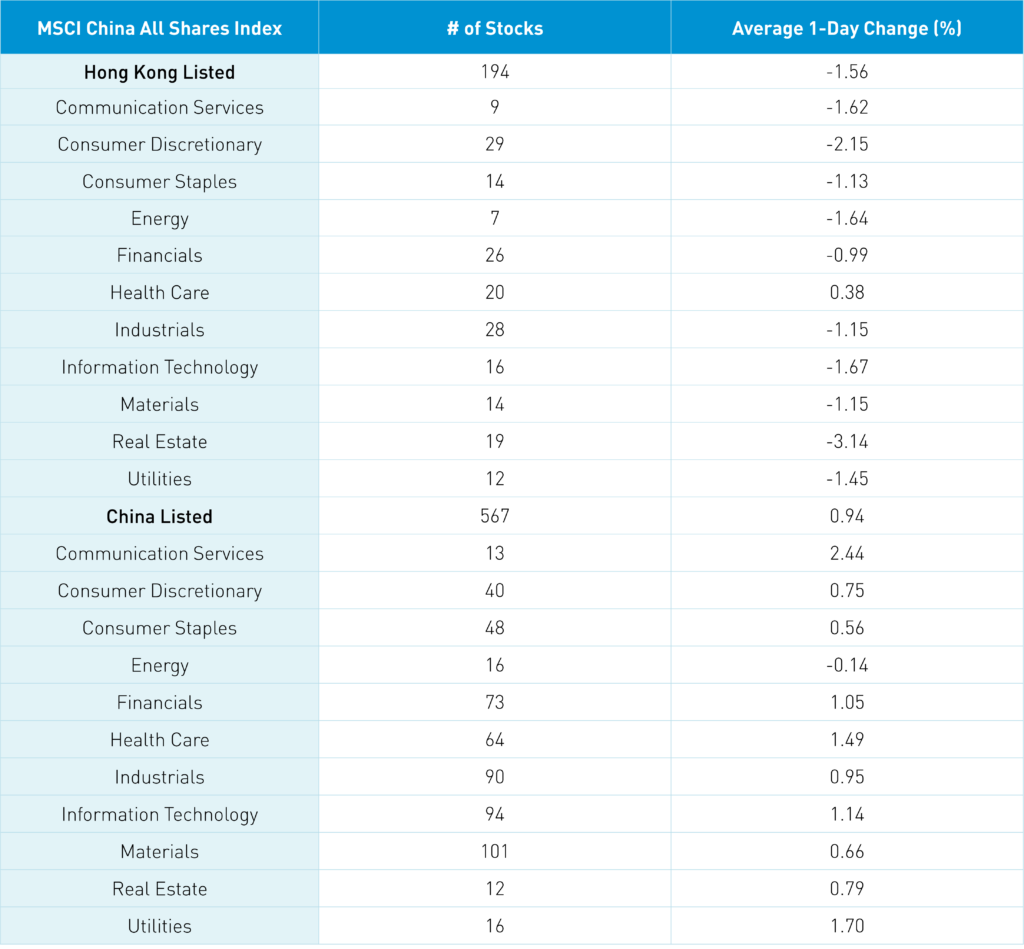

Mainland investors focused on several small positive developments that were ignored by foreign investors. China posted small gains versus Hong Kong falling despite US listed China ADRs posting gains yesterday. Mainland markets posted small gains with the communication sector gaining +2.44%, lifted by telecom related sub-sectors like 5G on government reports of investment support to assist the broader digital economy. Separately, support for traditional Chinese medicine lifted Mainland healthcare higher +1.48% with Hong Kong taking notice as healthcare gained +0.38%.

As the Dual Sessions take place, we’ll have more announcements culminating in the full must-see TV on March 5th when the full economic agenda and policies are released. Hong Kong lifting its mask mandate didn’t lift sentiment as political rhetoric continues with Congress launching committees as the two political parties work to outdo one another. We also had chatter about hedge funds taking profits in Chinese tech/internet stocks. I have no doubt many such investors bought low, so they are selling high. Less this type of investor, who is buying the stocks? Our pain trade is higher thesis is going through a correction without question though we shouldn’t be surprised by this.

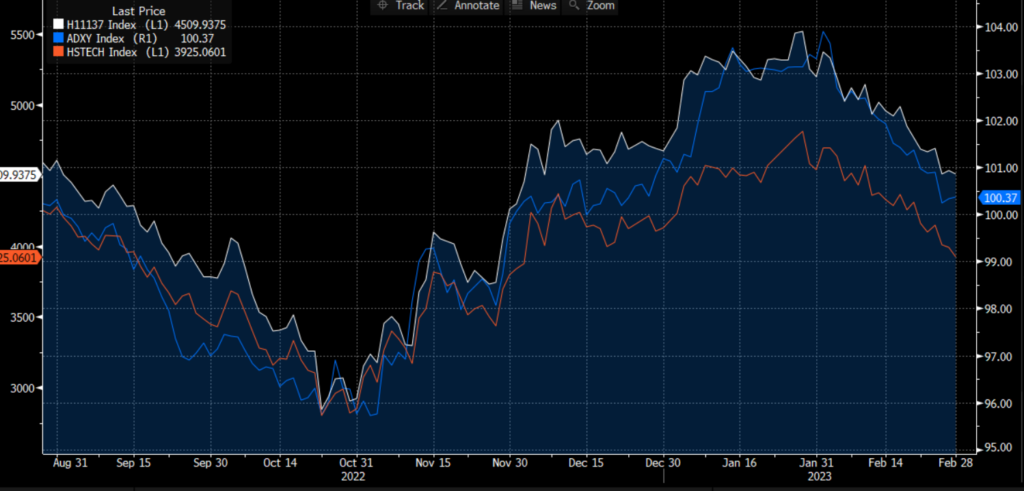

While the political rhetoric isn’t helpful the real culprit is driven by the US dollar’s significant rebound which is hurting risk assets globally as the Fed gets tough on inflation. The Asia dollar index has an eerily similar chart to offshore Chinese equities (see below chart of Asia dollar index -blue, CSI China Internet Index -white, and Hang Seng Tech Index -orange). A currency desk we utilize noted somewhat too cheerily that the Fed and other central banks might have more work to do which will weigh on risk assets i.e., stocks.

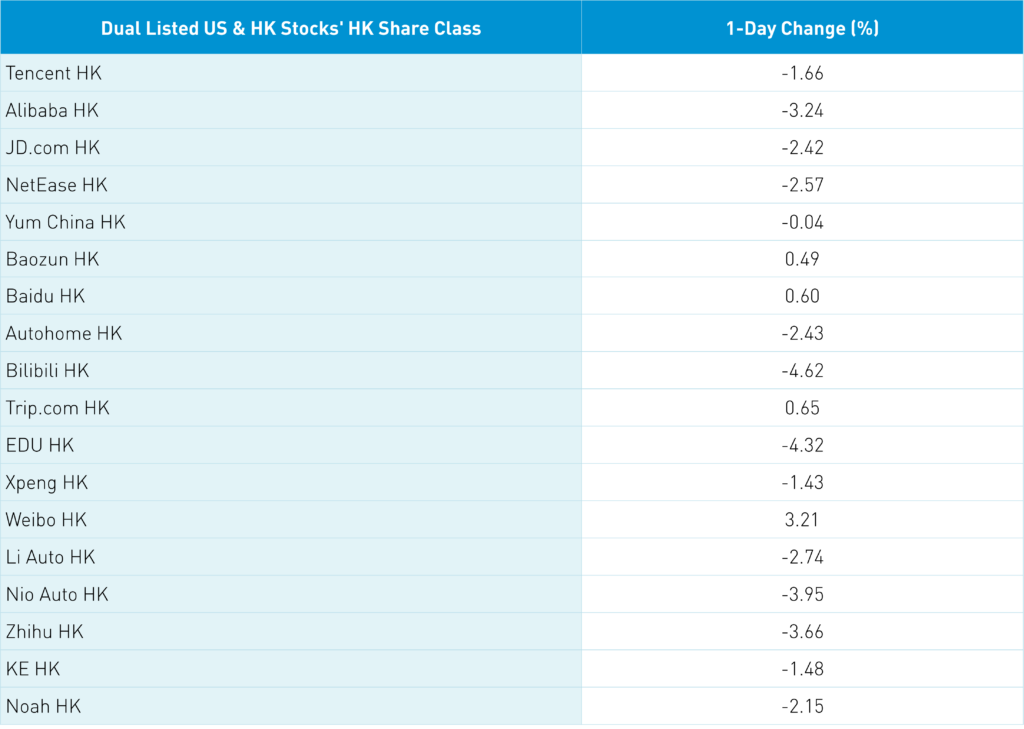

As we discussed yesterday, looking at inflation rates globally is shocking! All of this leads to one of the few countries with a central bank not raising rates, money supply is growing not shrinking, equity valuations are reasonable and Treasury yields have fallen over the last year. That country starts with a C and ends in A! Apologies to my Canadian friends, it is China! It didn’t matter for offshore investors today in Hong Kong but as we get more pro-active policy support it will become harder to ignore. Hong Kong’s most heavily traded were Tencent -1.66% despite a strong net buy via Southbound Stock Connect, Alibaba HK -3.24%, Meituan an inverse James Bond -0.07% despite moderate net buy from Southbound Stock Connect, and JD.com HK -2.42%. Real estate stocks were off after a distressed property developer had trouble making a bond payment. This problem isn’t going away for real estate equities as policy support includes allowing them to issue more stocks i.e., dilution, which is a good thing for their bonds as it bolsters their balance sheet.

At today’s close, passive index managers benchmarked to MSCI indices will have to rebalance their ETFs and index funds which has led to elevated volumes globally. The Hong Kong Exchange announced Monday a refinement to their Stock Connect trading holidays that expands the number of trading days/eliminates the number of days one can’t trade Connect. Remember, this was a factor in MSCI halting the inclusion of Chinese A shares in their indices. Remember, MSCI China only has approximately 20% exposure to Chinese A shares when it should be closer to 50%. That’s a shame as Chinese A shares are less influenced by political rhetoric as evidenced by today! We also have month end option expiration which will exacerbate today’s volumes.

Baidu will hold a press conference on March 16th on the firm’s technology efforts.

US government spending accounts for 25% of GDP. Wouldn’t cutting government spending fight inflation?

The Hang Seng and Hang Seng Tech fell -0.79% and -1.62% respectively on volume +26.74% from yesterday which is 114% of the 1-year average. 162 stocks advanced while 327 stocks declined. Main Board short turnover fell -11.63% from yesterday which is 89% of the 1-year average as 14% of turnover was short turnover. Growth and value factors were mixed as small caps “outperformed” large caps. Healthcare was the only positive sector up +0.38% while real estate fell -3.14%, discretionary closed lower -2.15%, and tech closed down -1.67%. Top sub-sectors are telecom, household products, and pharma/bio while auto, semis, and retailing were among the worst. Southbound Stock Connect volumes were light as Mainland investors sold -$409 million of Hong Kong stocks as Tencent was a large net buy, Meituan a moderate/large buy, and Kuaishou a small net buy.

Shanghai, Shenzhen, and STAR Board gained +0.66%, +0.81%, and +0.42% respectively on volume +0.67% from yesterday which is 84% of the 1-average. 3,663 stocks advanced while 1,020 declined. Growth and value factors were mixed while small caps outpaced large caps by a small caps. Top sectors were communication gaining +2.44%, utilities up +1.7%, and healthcare closing higher +1.48% while energy was the only down sector falling -0.15%. Top sub-sectors were telecom, computer hardware, and office supplies while coal, power generation, and fertilizer were on the bottom. Northbound Stock Connect volumes were moderate as foreign investors sold -$187 million of Mainland stocks. CNY appreciated +0.09% versus the US dollar to 6.398, Treasury bonds rallied, while Shanghai copper had a small gain and Shanghai steel fell -0.74%.

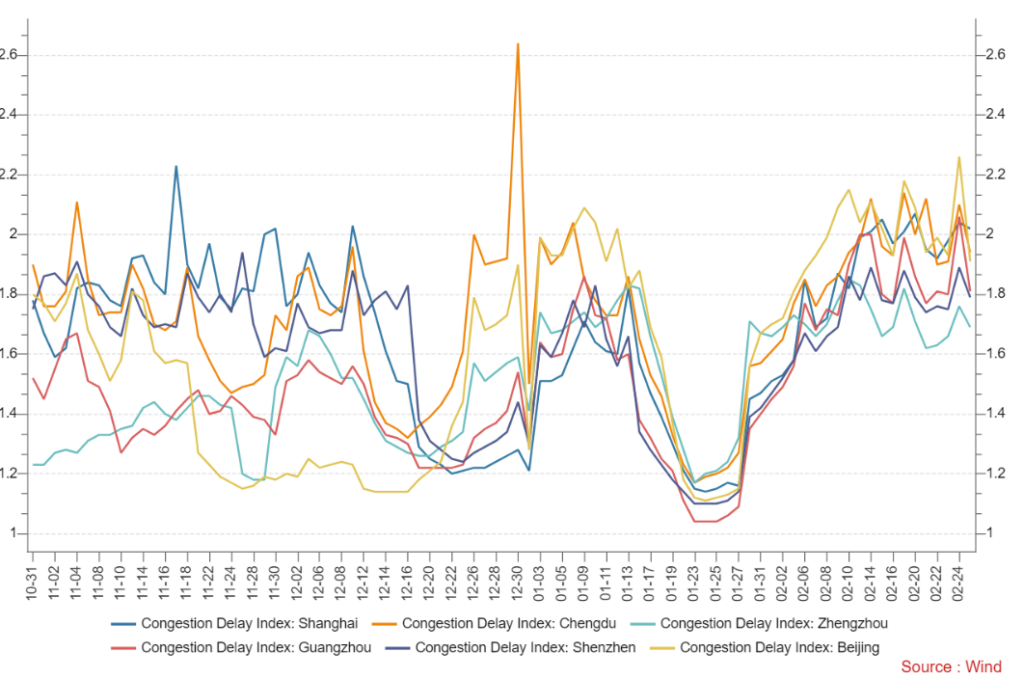

Chinese Major City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.93 versus 6.95 yesterday

- CNY per EUR 7.36 versus 7.35 yesterday

- Yield on 10-Year Government Bond 2.90% versus 2.91% yesterday

- Yield on 10-Year China Development Bank Bond 3.09% versus 3.10% yesterday

- Copper Price +0.03% overnight

- Steel Price -0.74% overnight