Hedge Fund 101: You Always Buy Liquidation Events

5 Min. Read Time

Key News

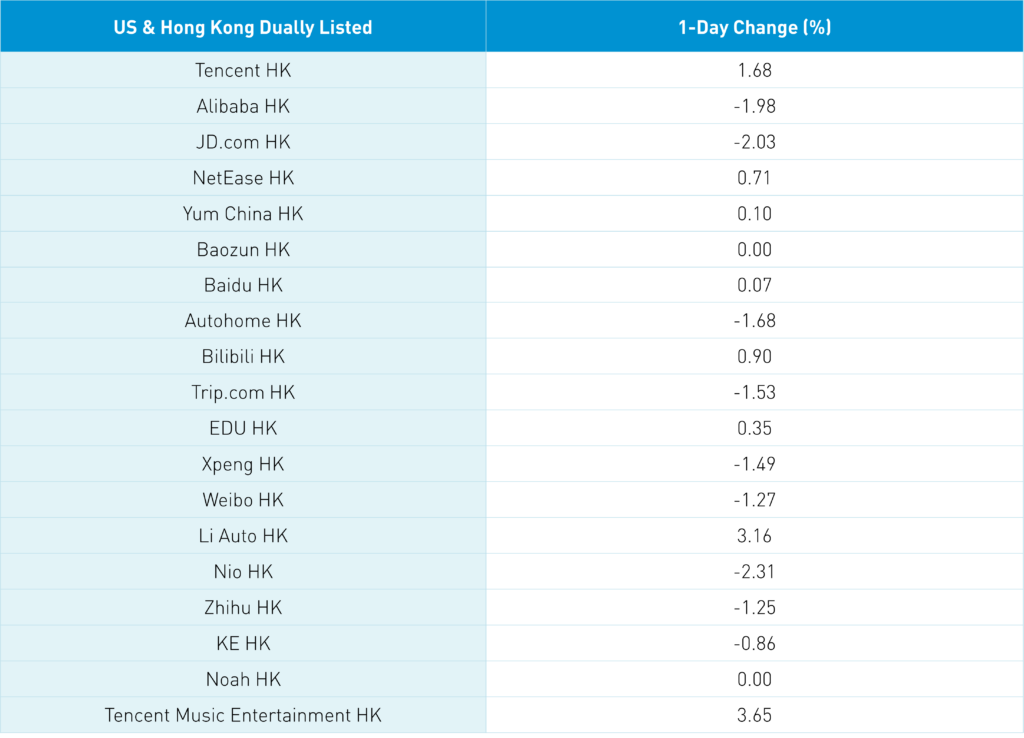

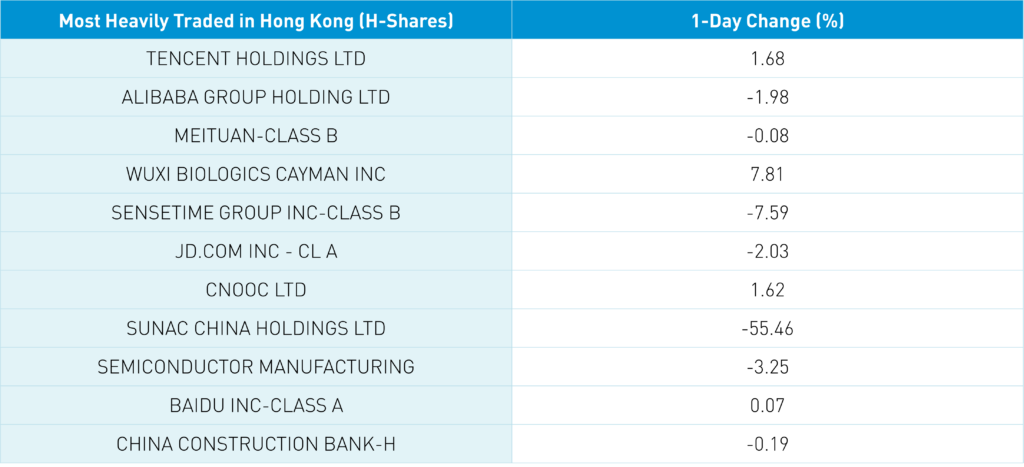

Overnight the Hang Seng Index and the Hang Seng Tech closed at +0.17% and -0.17% after US-listed China ADRs fell more than -4% yesterday! Let’s compare how Hong Kong’s most heavily traded closed in Hong Kong today versus their US-listed ADRs yesterday: Tencent gained +1.68% versus a -5.42% drop, Alibaba HK fell -1.98% versus a -5.93% drop, and Meituan closed flat at -0.08% versus a -5.61% drop. Other Hong Kong internet stocks versus their US ADRs were JD.com HK -2.03% versus -7.65%, Baidu HK +0.07% versus -0.21%, NetEase HK +0.71% versus -1.08%, and Trip.com HK -1.53% versus -4.91%. Asian investors agreed that removing Softbank as an Alibaba shareholder is a positive as it eliminates the specter of further selling.

We didn’t know why US-listed China ADRs were so weak yesterday, though, after the close, Financial Times reported Softbank reduced their position in Alibaba to 3.8% by selling forward contracts. Softbank’s stake fell from nearly 14% at year-end and 34% at its maximum. The news explains the “liquidation” feel of yesterday’s trading, which had traders scratching their heads. One does have to wonder why the Financial Times did not release the article until after US trading hours. Disappointing as a lot of damage could have been avoided.

Yesterday’s US-listed China ADRs weakness was very difficult to understand, though there were a few culprits, including:

• Prosus’ sale of Tencent led investors to front run their sale by selling Tencent; Tencent was sold two days in a row via Southbound Stock Connect Tuesday and Wednesday, which is rare; with that said, Prosus’ sale was well telegraphed/Not “new” news.

• JD.com announced a reorganization of their retail division and gave light Q1 guidance to stock analysts, who then reduced their price targets. Worth noting that even after lowering their price targets, the average price target is still +73% higher than yesterday’s.

• Buffett’s CNBC interview mentioned selling TSMC due to geopolitical risks; Berkshire Hathaway has trimmed but not eliminated its BYD position, which has been a huge success

• Buyers stayed on the sidelines/did not buy the dip as geopolitical risk/tension is a concern. There was talk yesterday that shorts pressed their bets in the China ADRs, which we haven’t seen in Hong Kong.

• Some pointed to low CPI/PPI as a sign of a weak economic recovery, though that’s a biased view as we know China’s economic recovery will take place incrementally. The key is a light inflation backdrop that allows for further monetary policy support.

Some positives that didn’t matter yesterday included: Brazil’s President Lula visiting China post France’s President Macron visit, chatter that Treasury’s Yellen and Commerce’s Raimondo will visit China and Australia, making small steps to repair trade relationship. LVMH financial results post Europe close highlight China’s consumer rebound.

What seemed very strange to me was CNH, China’s currency during US trading hours, was up versus the US dollar. CNH is a risk barometer as stocks are relatively easy to move, but the currency market is infinitely deeper/harder to move. CNH was “telling” us something very different than stock prices. CNH and the Asia dollar index posted small gains versus the US dollar yesterday. If we had adhered to our risk barometer, we would have/should have been a buyer yesterday.

Overnight we had March economic data in US dollars with exports up +14.8% year-over-year (YoY) versus expectations of -7.1% and February’s -1.3%, imports were down -1.4% YoY versus expectations -6.4% and February's +4.2%, and the trade balance was $88.1 billion versus expectations of $40 billion and February's $16.8 billion. In CNY, exports were up +23.4% and imports were up +6.1%, though everyone focuses on the trade data in US dollars. Also, it is very important to understand that as commodity prices have fallen, the value of imports fall. However, import volumes in millions of tons increased in nearly every category. Investors globally should cheer the data as it shows the global economy is holding up.

Asian equities were mixed with Thailand closed for Songkran, which is a celebration of the New Year, according to Google. Mainland China was lower as regulators jawbone investor enthusiasm around AI/ChatBot, which weighed on growth stocks and sectors. I am surprised electric vehicle (EV) names didn’t have a better day after President Xi visited GAC Aian New Energy Vehicle Co. Foreign investors were small net sellers via Northbound Stock Connect, with widely held growth stocks posting small net outflows.

Distressed real estate developer Suanc (1918 HK) opened down -55.46% after being suspended since last March after finally being able to release financial results. The stock has been kicked out of indices though you’ll notice some large passive shareholders. Sunac’s bond, due April 19th, is trading at just $22, indicating the company is dealing with significant issues. Mainland media noted real estate sales and prices picking up. The city of Harbin is providing childcare subsidies for parents with two or more children as the government continues to beta test solutions to incentivize couples to have more kids (hint: urban families don’t have many kids due to most apartments being two bedrooms. Build four-bedroom apartments and give them away IMO!).

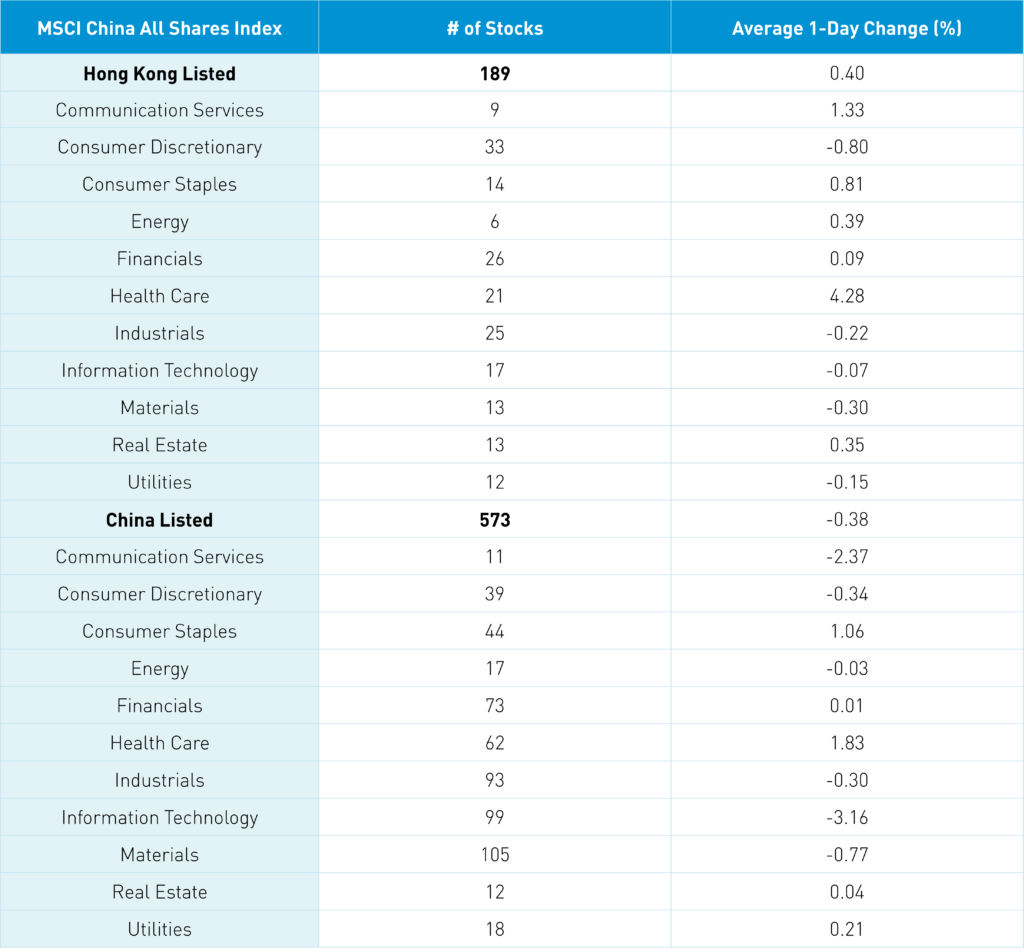

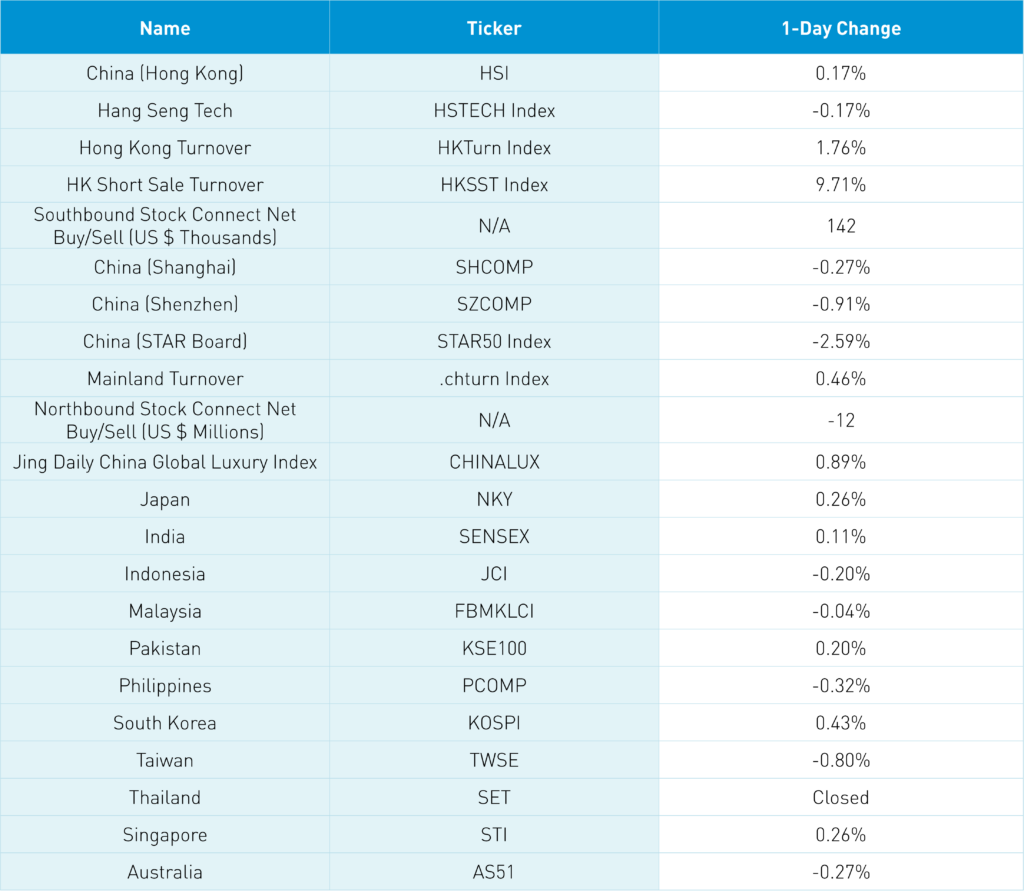

The Hang Seng and Hang Seng Tech closed at +0.17% and -0.17% on volume +1.76% from yesterday, which is 90% of the 1-year average. 277 stocks advanced, while 210 declined. Main Board short turnover increased +9.71% from yesterday, 76% of the 1-year average, as 14% of turnover was short turnover. Growth factors outpaced value factors as small caps outperformed large caps. Top sectors were healthcare gaining +4.28%, communication up +1.33%, and staples closing higher +0.81%, while discretionary fell -0.8%, materials closed lower -0.3%, and industrials were down -0.22%. The top sub-sectors were pharma, healthcare equipment, and media, while business services, retailing, and semis were the worst. Southbound Stock Connect volumes were moderate as Mainland investors bought $142 million of Hong Kong stocks, with Tencent a very small net sell, and Meituan a small net buy.

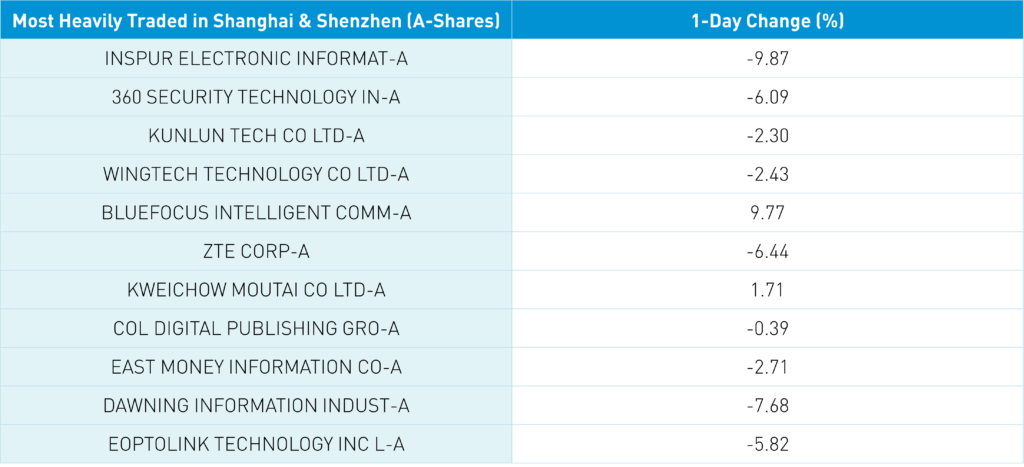

Shanghai, Shenzhen, and STAR Board were off -0.27%, -0.91%, and -2.59% respectively on volume +0.46% from yesterday, 125% of the 1-year average. 1,760 stocks advanced, while 2,887 stocks declined. Value factors outpaced growth factors as large caps outperformed small caps. The top sectors were healthcare up +1.8%, staples gaining +1.03%, and utilities closing higher +0.18%, while tech was down -3.18%, communication fell -2.4%, and materials closed lower -0.8%. The top sub-sectors were pharma, restaurants, and motorcycle, while computer hardware, communication equipment, and electronic components were the worst. Northbound Stock Connect volumes were elevated as foreign investors sold -$12 million of Mainland stocks, with foreign growth favorites seeing small net sells. CNY was flat/up slightly overnight versus the US dollar while Treasury bonds were sold. Shanghai Copper posted a small gain while steel was off.

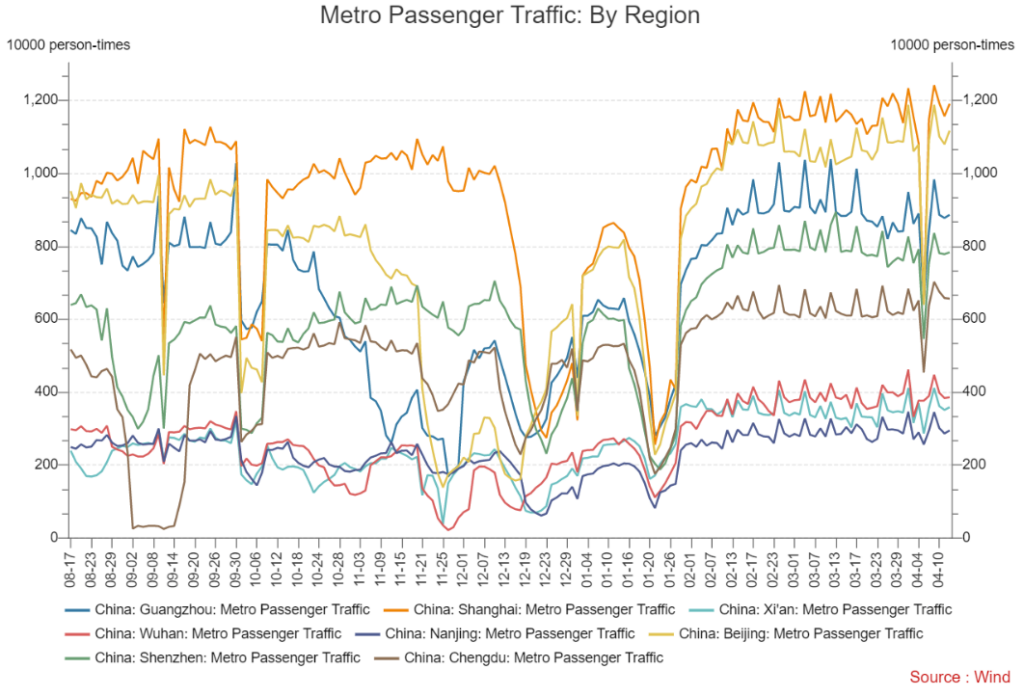

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.88 yesterday

- CNY per EUR 7.58 versus 7.52 yesterday

- Asia Dollar Index +0.24% overnight

- Yield on 10-Year Government Bond 2.83% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 2.99% yesterday

- Copper Price +0.26% overnight

- Steel Price -0.84% overnight