BYD Crushes The Bug as Hong Kong Internet Names Rebound & Xi Calls Zelensky

3 Min. Read Time

Key News

Asian equity markets were mixed overnight as investors cheered the first round of US mega-tech earnings from Microsoft and Google.

Hong Kong rebounded despite a steep selloff in US-listed China stocks yesterday, in what felt like the first time in two weeks. Intra-day yesterday, several US Senators asked for Chinese cloud companies to be added to export control lists including Alibaba’s cloud unit (banking crisis, debt ceiling crisis, and this is the focus?).

Early investor Prosus cut its stake in Tencent again while a well-respected analyst’s report on China equity positions being reduced weighed on sentiment. These may have contributed to yesterday's sharp/disappointing move which one of our trading partners/friends called “capitulation” (fingers crossed).

Overnight, we had news that Tencent has stepped up its buyback, which minimizes but doesn’t eliminate the impact of Prosus selling, while Alibaba’s cloud unit, with a 30% market share in China, announced competitive price cuts. It was also announced that inbound foreign visitors to China will not need PCR tests. Meanwhile, data for China’s upcoming Labor day travel look strong.

The Politburo will meet this week, which will provide policy makers the venue to announce economic policies. Despite China’s incremental economic rebound, stocks haven’t performed well of late. We would expect policy support for China tech and self-sufficiency in light of the US export controls though consumption should receive attention. Yes, there is the geopolitical overhang of poor US-China political relations, driven by a lack of communication, but also the strong US dollar, which, since the last week of January has been a headwind.

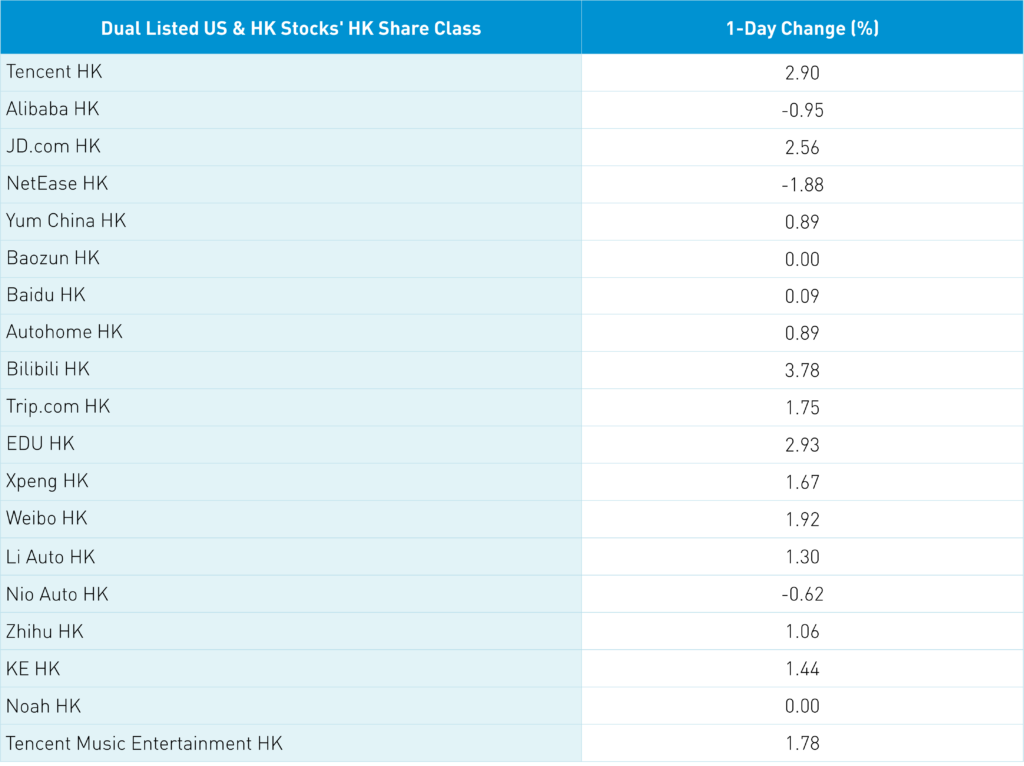

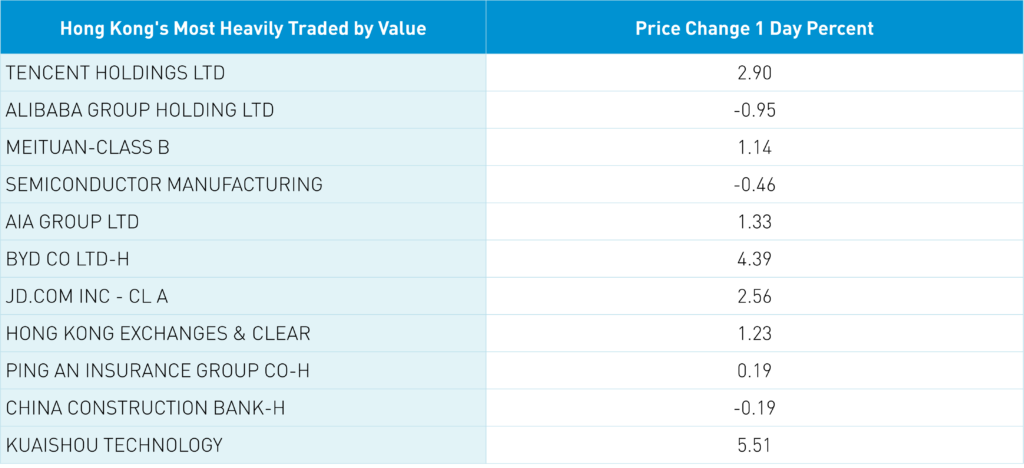

This morning it was announced President Xi and President Zelensky spoke. Hong Kong opened lower but grinded higher with today’s most heavily traded being Tencent gaining +2.9% versus the US ADR falling -2.33%, Alibaba HK -0.95% versus the US ADR falling -4.57% yesterday, Meituan +1.14% versus the US ADR falling -4.36%. Similar for JD.com HK +2.56% and Baidu HK +0.09% versus their ADRs -2.83% and -4.63%.

BYD gained +4.39% after Bloomberg News reported the company sold 440,000 EV cars in Q1 which dethrones Volkswagen, the #1 automaker since 2008, which sold 427,000 cars with only 6% being electric vehicles. Hong Kong short volume was high though concentrated in ETFs for the most part. China was mixed with Shanghai off and Shenzhen up on another high turnover day as plans for a real estate tax is progressing which would a first. A tax would help disincentivize household’s infatuation with real estate though the timing is apt to be kicked out to allow the sector to recover.

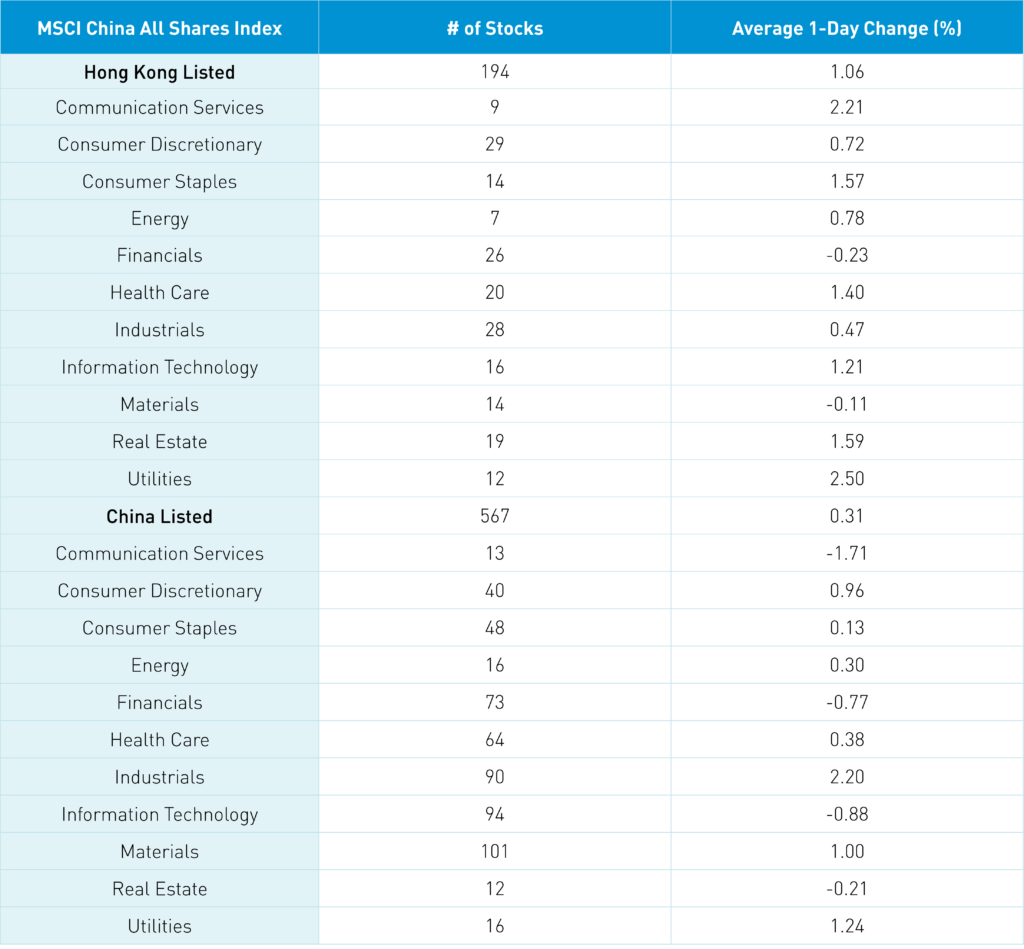

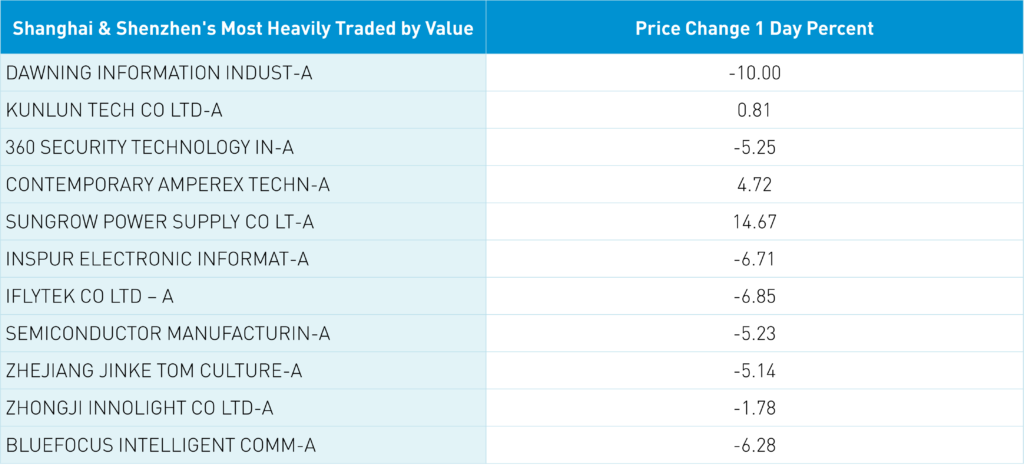

Tech and communication were off as investors take profit in recent highflying stocks/sectors. Foreign investors appear to be participating as the top Northbound Stock Connect buys in the last 7 days and 1 month are tech and communication plays versus the top buys over the last year being liquor stocks like Wuliangye and Kweichow Moutai, EV battery maker CATL, appliance maker Midea, medical equipment maker Mindray, solar company Longi Green Energy, and insurance giant Ping An. Northbound Stock Connect volumes were very high indicating some rebalancing is occurring. Domestic and foreign investor favorite Sungrow Power Supply (300274 CH) jumped +14.67% post strong Q1 results helping the clean tech space.

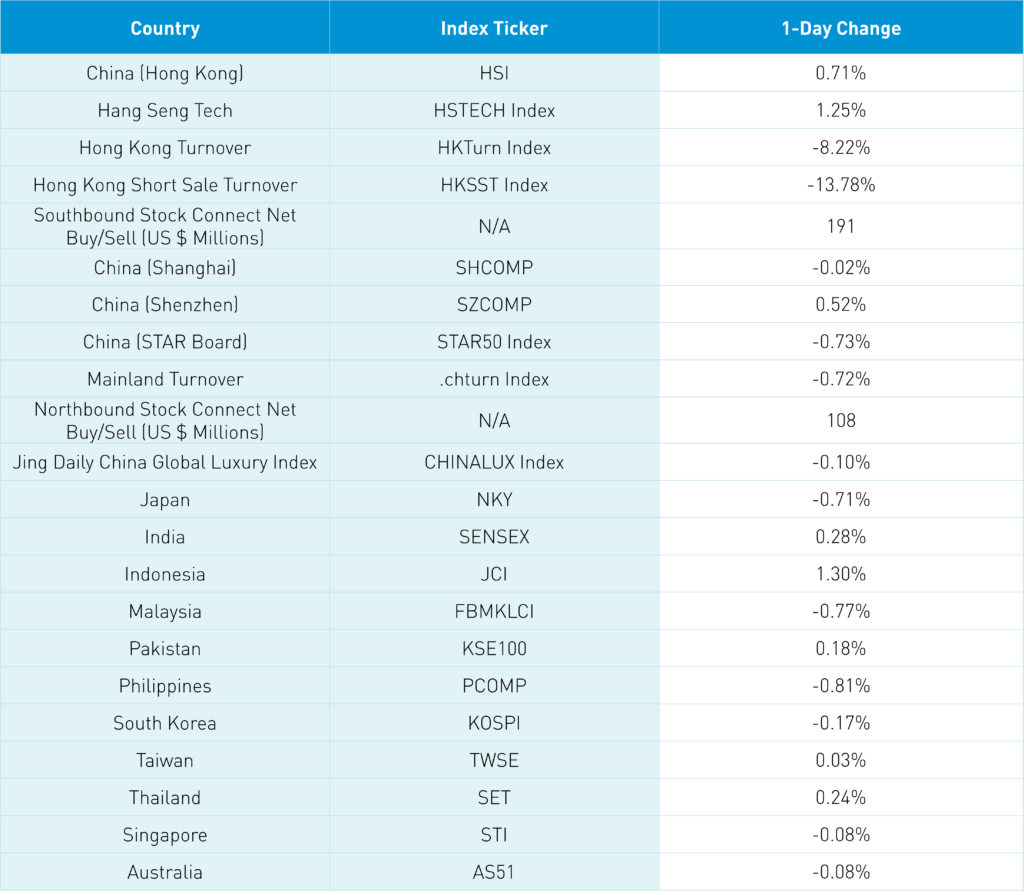

The Hang Seng and Hang Seng Tech gained +0.71% and +1.25% respectively on volume -8.22% from yesterday which is 81% of the 1-year average. 363 stocks advanced while 124 declined. Main Board short turnover fell -13.77% from yesterday which is 84% of the 1-year average as 18% of turnover was short turnover. Growth outperformed value while small caps outperformed large caps. Top sectors were utilities, communication, and real estate while financials and materials were off -0.23% and -0.11%. Top sub-sectors were auto, software, and utilities while food, telecom, and banks were the worst. Southbound Stock Connect volumes were LIGHT as Mainland investors bought $191 million of Hong Kong stocks with Meituan a small net buy, Tencent, and Kuaishou were moderate net buys.

Shanghai, Shenzhen, and STAR Board were mixed -0.02%, +0.52%, and -0.73% respectively on volume -0.72% from yesterday which is 124% of the 1-year average. 3,484 stocks advanced while 1,253 stocks declined. Growth outperformed value while small caps outperformed large caps. Top sectors were industrials +2.19%, utilities +1.23%, and materials +0.99% while communication -1.73%, tech -0.89%, and financials -0.78%. Top sub-sectors were power generation equipment, electric power grid, and soft drinks while computer hardware, software, and communication equipment were the worst. Northbound Stock Connect volumes were high as foreign investors bought $108 million of Mainland stocks with Kweichow Moutai and Ping An were small net sells. CNY and the Asia dollar index were up slightly versus the US dollar. Treasury bonds rallied while Shanghai copper and steel were off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.92 versus 6.92 yesterday

- CNY per EUR 7.65 versus 7.63 yesterday

- Asia Dollar Index +0.10% overnight

- Yield on 10-Year Government Bond 2.80% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 2.98% versus 3.00% yesterday

- Copper Price -1.57% overnight

- Steel Price -0.46% overnight