China Markets Rebound, Alibaba’s First Spinoff Approaches, Week in Review

5 Min. Read Time

Week in Review

- Only a few markets managed gains for the week: Indonesia, the Philippines, Hong Kong, and Mainland China. Meanwhile, Japan, Taiwan, South Korea, India, and Singapore were all lower on hawkish Central Bank speech and a jump in the US dollar.

- There were multiple diplomatic overtures between the US and China this week including US National Security Advisor Jake Sullivan’s meeting with China’s Foreign Minister in Malta and US Secretary of State Blinken’s meeting with China’s Vice President Han Zheng during the UN General Assembly, which was held in New York this week.

- Consumers in China spent more than expected this week on Huawei’s new Mate 60 phones, which were reported to be selling faster than stores can restock them, and baijiu-infused coffee, which helped liquor giant Kweichow Moutai become the largest constituent in the MSCI China A Index.

- Mainland investors bought an impressive net $14 billion worth of Hong Kong stocks this week on weakness.

Friday’s Key News

Asian equities were mixed as Mainland China and Hong Kong bucked the trend by outperforming while Japan, South Korea, and India underperformed.

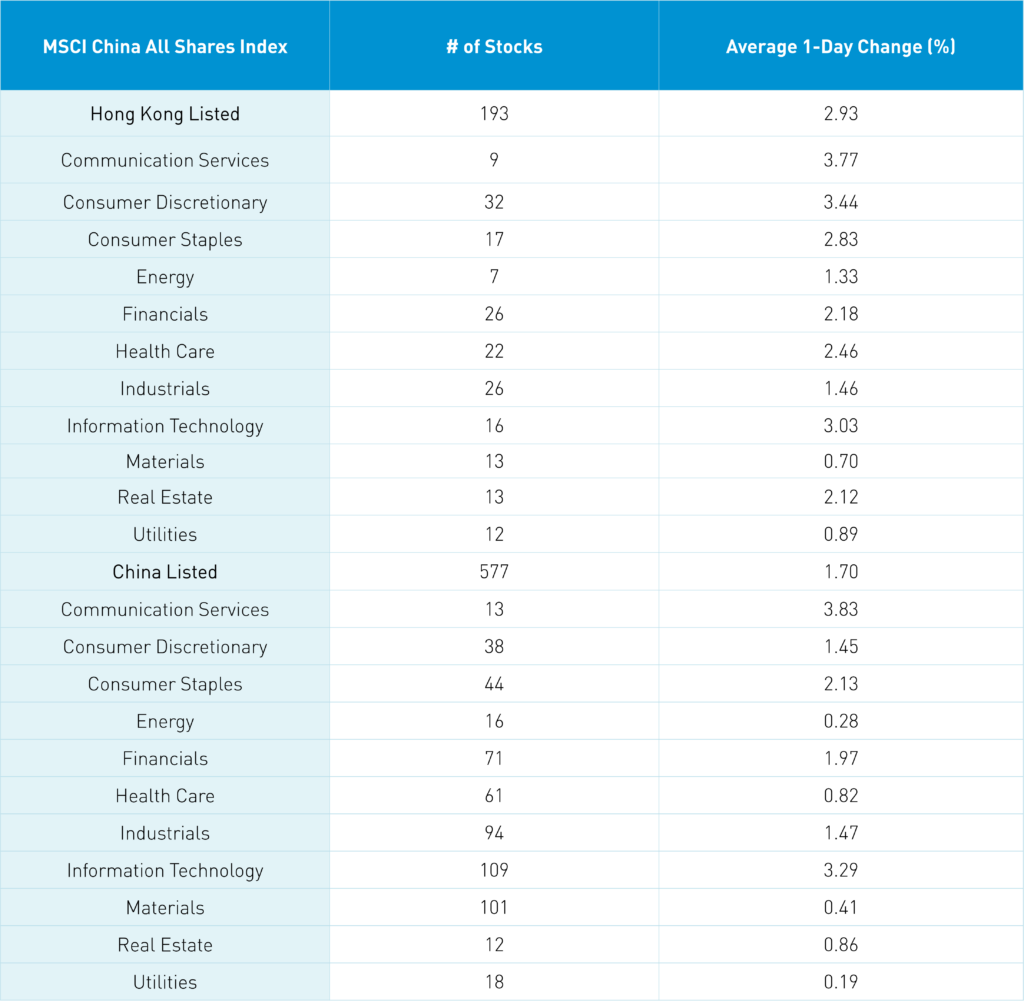

All sectors in both Hong Kong and Mainland China were up today, led by growth stocks and sectors, as breadth was decent as advancers outpaced decliners handily, which was a complete reversal of yesterday’s moves. As I noted yesterday, the Shanghai, Shenzhen and Hang Seng Index have all breached big, round numbers and are hovering around 3,100, 1,900, and 18,000, respectively. This puts the market’s declines on policymakers’ radars. Investors, on the other hand, may also note the undervaluation of China equities, especially in light of higher US interest rates, which still have the potential to weigh on US stocks.

Yesterday, we speculated on the potential unraveling of the most crowded trade ever, namely the overweight of US stocks amongst global investors. When might this trade, which has been supported by the US dollar’s strength over the last decade, come to an end? As the US government nears a shutdown, this US equity overweight could become slightly uncomfortable against the backdrop of high valuations.

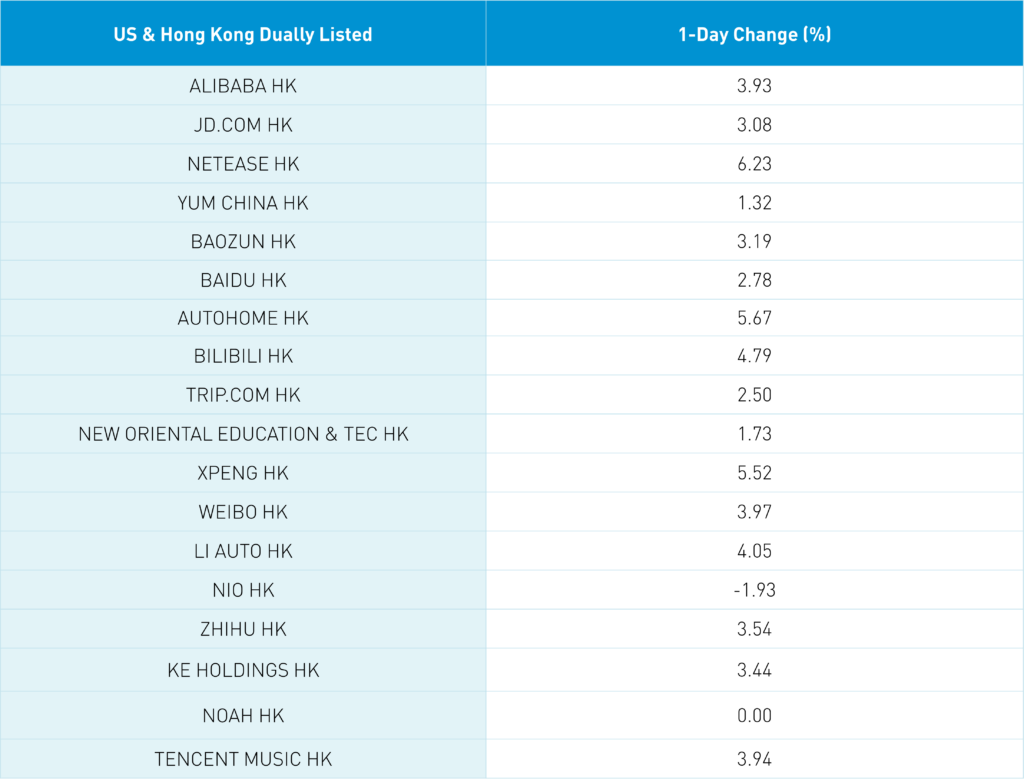

Nonetheless, there were catalysts behind today’s move apart from the macroeconomic narrative. Alibaba jumped +3.93% overnight, as its logistics unit Cainiao is rumored to be filing for its IPO next week. Through its restructuring and subsequent spinoffs, Alibaba is forcing investors to perform a sum-of-the-parts (SOTP) analysis by separating its six core businesses from each other and analyzing their fundamentals individually. This has led not only to individual stock upgrades. Another catalyst was several global research strategists warming up to China’s market.

Foreign ownership limits on individual stocks will increase from the current levels of 30% for total foreign ownership and 10% for any individual foreign owner. Meanwhile, Beijing and Shanghai will ease limitations on foreigners' ability to move money in and out of the country.

The fact is that Hong Kong was severely oversold and overdue for the bounce we saw overnight, as China’s economy incrementally rebounds. As we near China’s big week-long holiday, pre-bookings of hotel, train, and domestic travel numbers look very strong. We are also seeing very strong sales numbers for both Apple’s and Huawei’s new phones.

Southbound Stock Connect saw a net outflow though the Hong Kong Tracker ETF, which tracks the Hang Seng Index, saw a big outflow while individual stocks largely saw net purchasing. Shanghai and Shenzhen also grinded higher all day, driven by the tech subsectors that ripped. As mentioned yesterday, foreign sales of Mainland growth stocks have weighed on Kweichow Moutai, CATL, and BYD. Meanwhile, new names became more prominent. In keeping with the opposite day narrative, foreign investors bought a net $1.025 billion worth of Mainland stocks as these three stocks gained +2.81%, +2.03%, and +2.24%, respectively.

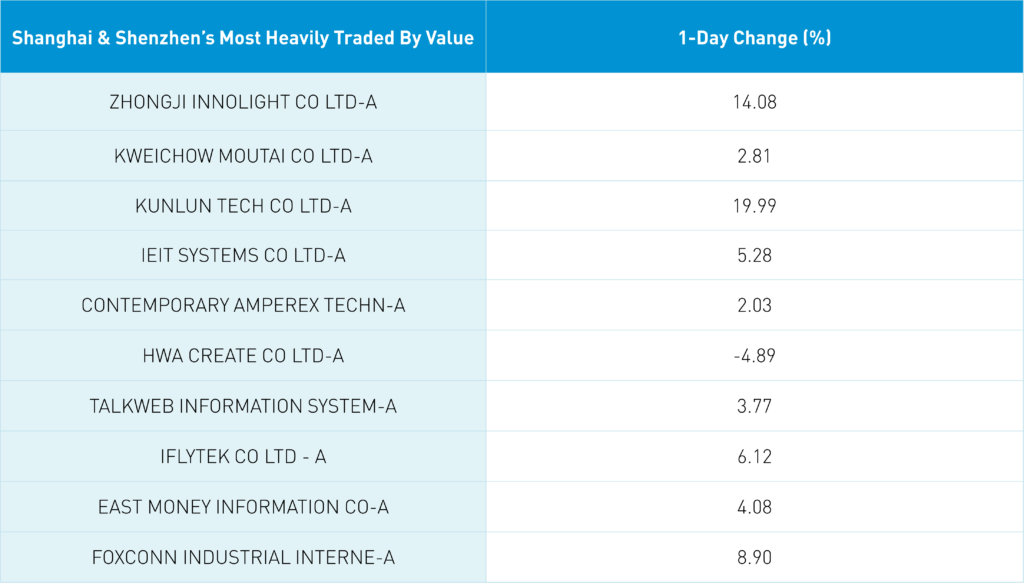

Today’s most heavily traded stock by value in Mainland China was Zhongji Innnolight, which gained +14.08%, the third most heavily traded stock was Kunlun Tech, which gained +19.99%, the 14th most traded was Eoptolink Tech, which gained +12.16%, and the 18th most traded was Suzhou TFC Optical, which gained +20%. In summary, AI, mobile phone component, communication, and ChatGPT-like stocks and internet stocks saw the most significant rips higher.

The People’s Bank of China (PBOC) identified 20 banks as systemically important, which requires the banks adhere to capital and leverage.

In China, it was noted that the US-China economic working group, established during Janet Yellen’s China visit with He Lifeng, will start to meet. This is yet another green shoot in US-China diplomatic relations!

We have highlighted Southbound Stock Connect flows and Hong Kong Main Board short turnover. As noted today, Southbound Stock Connect data now includes ETF flows, which have been very volatile. In examining Hong Kong’s rising short volume, we found out that short turnover now includes ETF volume. This has distorted short turnover as market makers need short ETFs in advance of selling shares to an investor without having any ETF shares in their inventory. ETF short turnover is potentially nearly 50% of short turnover. We are working with a data provider to strip out the ETF volume in Stock Connect and short turnover. Just an FYI, but Hong Kong’s short turnover might not be as bad as we initially thought.

The Hang Seng and Hang Seng Tech indexes gained +2.28% and +3.69%, respectively, on volume that increased +32% from yesterday, which is 89% of the 1-year average. 425 stocks advanced while 68 stocks declined. Main Board short turnover increased +32% from yesterday, which is 112% of the 1-year average as 21% of turnover was short turnover. The growth factor outperformed the value factor while small caps outpaced large caps. All sectors were up as the top-performing sectors were communication services, which gained +3.77%, consumer discretionary, which gained +3.40%, and technology, which gained +3.03%. The top-performing subsectors were short video and live broadcasting. Meanwhile, internet credit and microfinance were the among worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors sold a net -$540 million worth of Hong Kong-listed ETFs and stocks as Tencent, Meituan, Ping An Insurance, and Kuaishou were moderate net buys while the Hong Kong Tracker ETF was a very large net sell.

Shanghai, Shenzhen, and the STAR Board gained +1.55%, +1.91%, and +2.61%, respectively, on volume that increased +32%, which is 87% of the 1-year average. 4,293 stocks advanced while 582 stocks declined. The growth factor outperformed the value factor as large caps outperformed small caps. All sectors were higher as the top-performing sectors were communication services, which gained +3.82%, technology, which gained +3.28%, and consumer staples, which gained +2.12%. The top-performing subsectors were optical modules, optical communication, and software. Meanwhile gold, mining, and coal were among the worst. Northbound Stock Connect volumes were moderate as foreign investors bought a net $1 billion worth of Mainland stocks as BYD was a large net buy, Foxconn was a moderate net buy, Sokon and Kweichow Moutai were small net buys. Meanwhile, CATL, Sungrow, and Zijin Mining were moderate and moderate/high net sells. Treasury bonds sold off while CNY and the Asia Dollar Index, which gained versus the US dollar. Copper and steel were both down.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.30 versus 7.31 yesterday

- CNY per EUR 7.77 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.34% versus 1.50% yesterday

- Yield on 10-Year Government Bond 2.68% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 2.76% versus 2.73% yesterday

- Copper Price -1.06% overnight

- Steel Price -0.66% overnight