Hong Kong and Shenzhen Trip Recap, November Export Data Beats

3 Min. Read Time

Key News

Asian equities were a sea of red, though Japan's Yen strengthened to 145 versus the US dollar from its low of 151. Hopefully, the Bank of Japan doesn’t move too quickly before I can book a cheap vacation there.

Hong Kong and Mainland China fell early as Moody’s doubled down on yesterday’s downgrades by adjusting the outlook from stable to negative on a slew of Chinese banks, policy banks, and, shockingly, Tencent and Alibaba, despite their extraordinary cash flows. Hopefully, the press Moody’s receives for the downgrades is worth it, as I would value their business prospects in Mainland China going forward at zero.

November's exports and trade balance in US dollars beat expectations, as the former increased +0.5% versus October’s year-over-year decline of -6.4% as autos and mobile phones were key drivers. Imports missed expectations of +3.9% with a release of -0.6%. It is worth noting that in Renminbi terms exports increased +1.7% and imports increased +0.6%. Also, commodity prices have an effect on the value of exports/imports and oil prices have fallen.

Instead of focusing on the dollar value of exports/imports, we should look at the export/import volume in tons. That data tells us that oil imports fell, though soybean imports increased significantly, which is a good sign for US farmers.

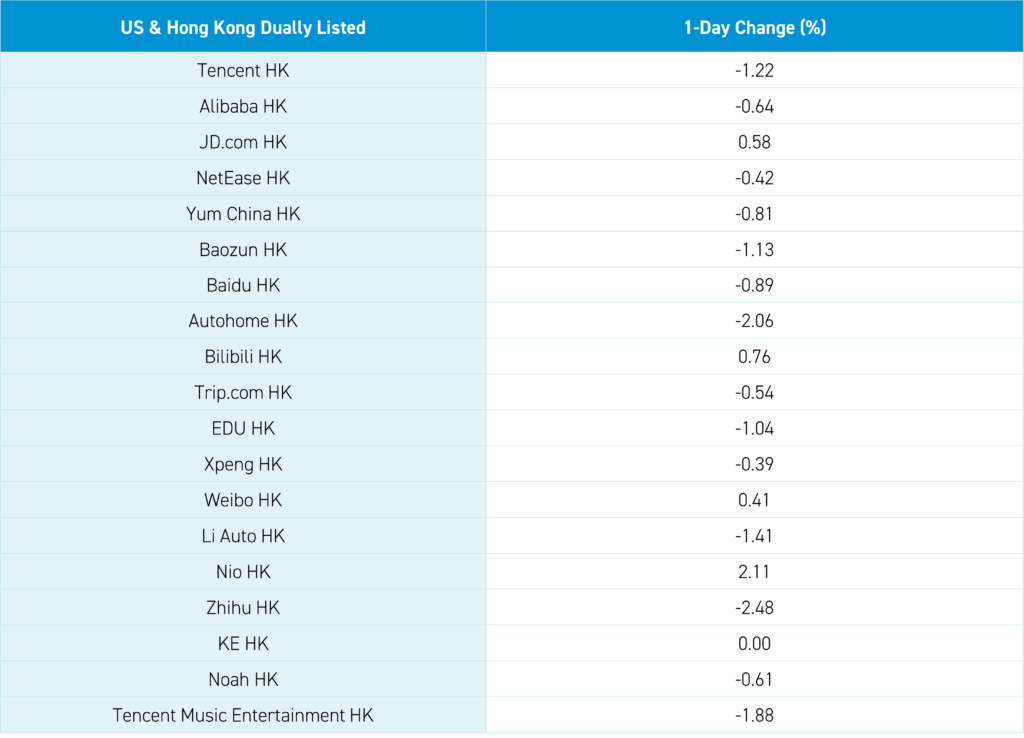

Hong Kong and Mainland China rallied off mid-morning lows to close down, but not nearly as bad as earlier in the session. Hong Kong’s most heavily traded stocks were Tencent, which fell -1.22%, Meituan, which fell -0.35%, and Alibaba, which fell -0.64% versus the US listing, which fell -1.23%. Healthcare was off again, as WuXi Biologics declined -2.44% to HKD 3.83 after falling -23.82% on Monday to 4.24 despite its buyback announcement.

Mainland China posted small losses and likewise rose off of mid-morning lows. EU leaders are currently visiting Beijing. President Xi will hold meetings with EU Commission President Ursula von der Leyen and EU Council President Charles Michel.

A quick note on my Hong Kong and Shenzhen trip. Both cities appeared busy, with malls and restaurants full, streets busy, traffic bad, and trains crowded. Visually, things seemed fine. In contrast, in my meeting with Hong Kong investors, the mood was low as the Hong Kong market is on track to fall for the fourth year. It is worth noting that Mainland China is “only” headed to its second annual loss. Many Hong Kong discussions revolved around Japan and US stocks as local investors pivot to what has been working, which is no different from similar conversations that I’ve had with institutional investors globally. Several trading desks were equally bummed out as trading volumes have been light. Could this mean peak pessimism in Hong Kong? It certainly felt like it, candidly. Ultimately, many Hong Kong companies are buying back stock and paying dividends. Meanwhile, China’s economy is coming back, albeit slowly, while valuations are very low on both an historical and a relative basis. We are supposed to buy low, right?

The mood in Shenzhen was more positive as one local manager saw the Mainland market’s weakness as a strong entry point. When asked personally how they were doing in a meeting with Hong Kong investors, they were fine, as many are planning the December and Chinese New Year holidays—another interesting discrepancy. I’ll share some Hong Kong and Shenzhen photos via Twitter (@ahern_brendan).

The Hang Seng and Hang Seng Tech indexes fell -0.71% and -0.73%, respectively, on volume that decreased -10% from yesterday, which is 83% of the 1-year average. 129 stocks advanced, while 344 declined. Main Board short turnover decreased -15.73% from yesterday, which is 90% of the 1-year average as 18% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and large caps “outperformed”/fell less than the value factor and small caps. Staples was the only positive sector +0.1%, while healthcare -1.74%, materials -1.6%, and tech -1.57%. Healthcare was the only positive sub-sector, while semis, pharmaceuticals, and energy were the worst. Southbound Stock Connect volumes were moderate/light as Mainland investors sold -$209mm of Hong Kong stocks and ETFs with energy giant CNOOC, Meituan, and Meitun were small net buys while the Hong Kong Tracker ETF and HS H Share ETF moderate/large net sells.

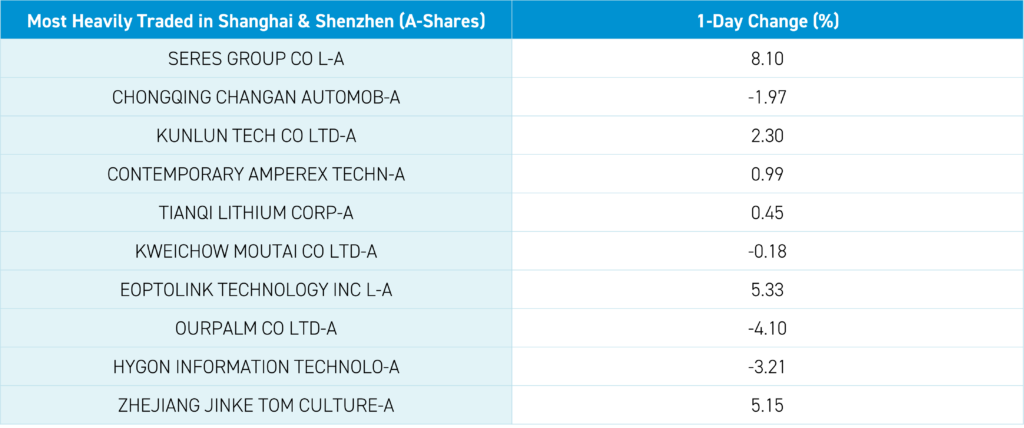

Shanghai, Shenzhen, and the STAR Board fell -0.0.9%, -0.27%, and -0.15%, respectively, on volume that was flat from yesterday, which is 94% of the 1-year average. 1,698 advanced, while 3,117 declined. The value factor and large caps “outperformed”/fell less than the growth factor and small caps. The top sectors were communication +1.51%, utilities +0.6%, and financials +0.44%, while healthcare -1.09%, energy -0.96% and materials -0.64%. The top sub-sectors were software, cultural media, and internet, while power generation equipment, office supplies, and pharmaceuticals were the worst. Northbound Stock Connect volumes were light/moderate as foreign investors bought $52mm of Mainland stocks with CATL and Kweichow Moutai moderate net buys, Tianqi Lithium a small net net buy, while United Imaging and Longi were small net sells. CNY and Asia dollar were flat. Treasury bonds rallied while copper fell and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.15 versus 7.15 yesterday

- CNY per EUR 7.70 versus 7.72 yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.67% yesterday

- Yield on 10-Year China Development Bank Bond 2.78% versus 2.78% yesterday

- Copper Price -0.21%

- Steel Price +1.99%