Minor Rules Make Major Impact, Week in Review

3 Min. Read Time

Week in Review

- Asian equities had a positive performance week until last night, when new gaming regulations for minors weighed on Hong Kong's stock market.

- We saw major flows to Hong Kong-listed ETFs from Mainland investors this week via Southbound Stock Connect.

- NIO announced a significant investment from an Abu Dhabi-based investor, which led to gains in its share price though the stock was volatile this week due to a Biden Administration plan for tariffs on EV imports.

- State-owned banks lowered deposit rates this week, the latest stimulus measure to support China's economic recovery.

Friday's Key News

Asian equities were largely higher, though Hong Kong underperformed, and the US dollar weakened overnight.

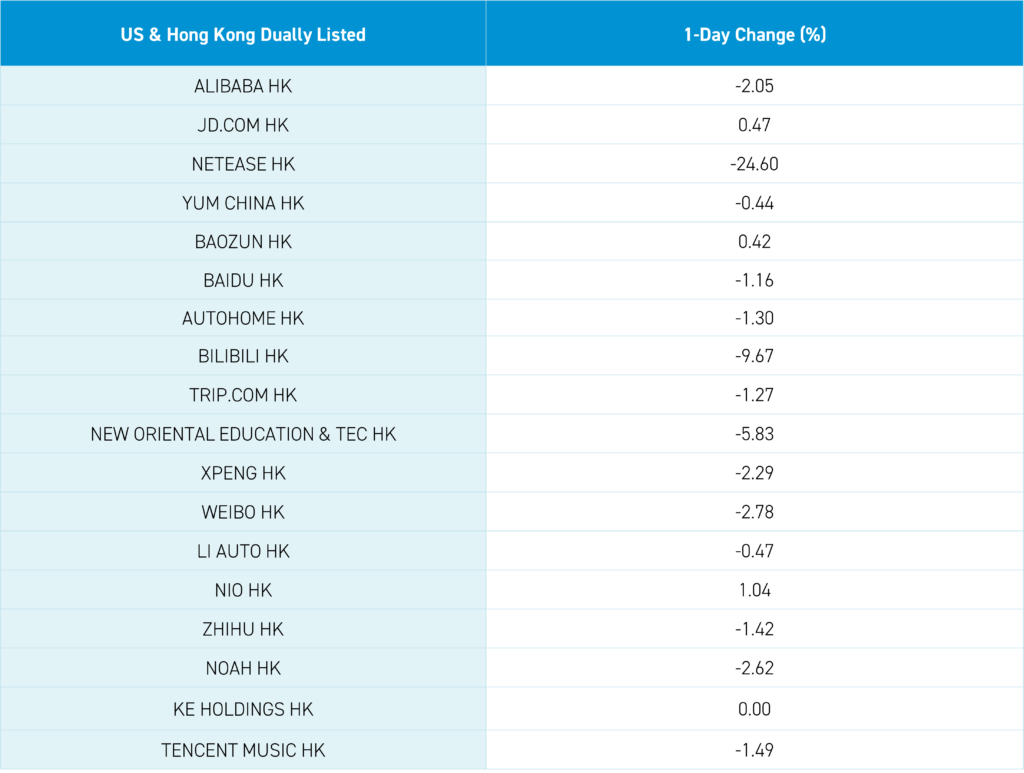

Both Hong Kong and Mainland China rose in morning trading until the late morning release of draft regulations regarding minors’ online gaming from the National Press and Publication Administration (NPPA) sent both markets lower as gaming companies Tencent, NetEase, and Bilibili fell by -1.35% and -24.6%, and -9.67%, respectively. The abysmal timing of the release greatly exacerbated the impact with many investors on holiday. Investors shot first and asked questions later as the move stoked fears of government interference. It is important to remember that the measures are only a draft, and previous regulations have considerably tightened rules governing minors’ gaming time and the companies’ small revenue exposure to minors. The draft rules include a prohibition on awarding users for logging on daily, to fight video game addiction, as well as potential limits on spending on online gaming platforms. Some of the heightened concern around this particular draft is that the scope could be broad and not just focused on minors.

The move undermines recent indications from President Xi that he would like to make China friendlier to foreign corporations and investors. China is often viewed as a singular entity. However, in reality, its government is constituted of a giant, complex bureaucracy that often does not know or even see what individual agencies are doing. Today’s move goes completely against efforts to rebuild investor confidence while hurting investors, including Mainland Chinese investors, and impacting a well-respected and widely owned company. Tencent’s volume increased by +1,346% from yesterday, NetEase's volume by +1,331%, and Bilibili’s by +440%.

The NPPA announcement also weighed on Alibaba, which fell -2.04%, Meituan, which fell -3.89%, and Kuaishou, which fell -7.22%. However, JD.com gained +0.47%. It also weighed on investor sentiment, with Hong Kong and Mainland China falling on the news. Again, the extent of the move seems greatly exaggerated and even if implemented will not meaningfully impact the companies. Tencent lost -$47 billion in market cap today, which makes no sense to me.

It is wholly disappointing to enter a holiday weekend and year-end with today’s market move. With that said, on behalf of KraneShares, we hope you and your loved ones have a wonderful holiday weekend and a happy New Year’s.

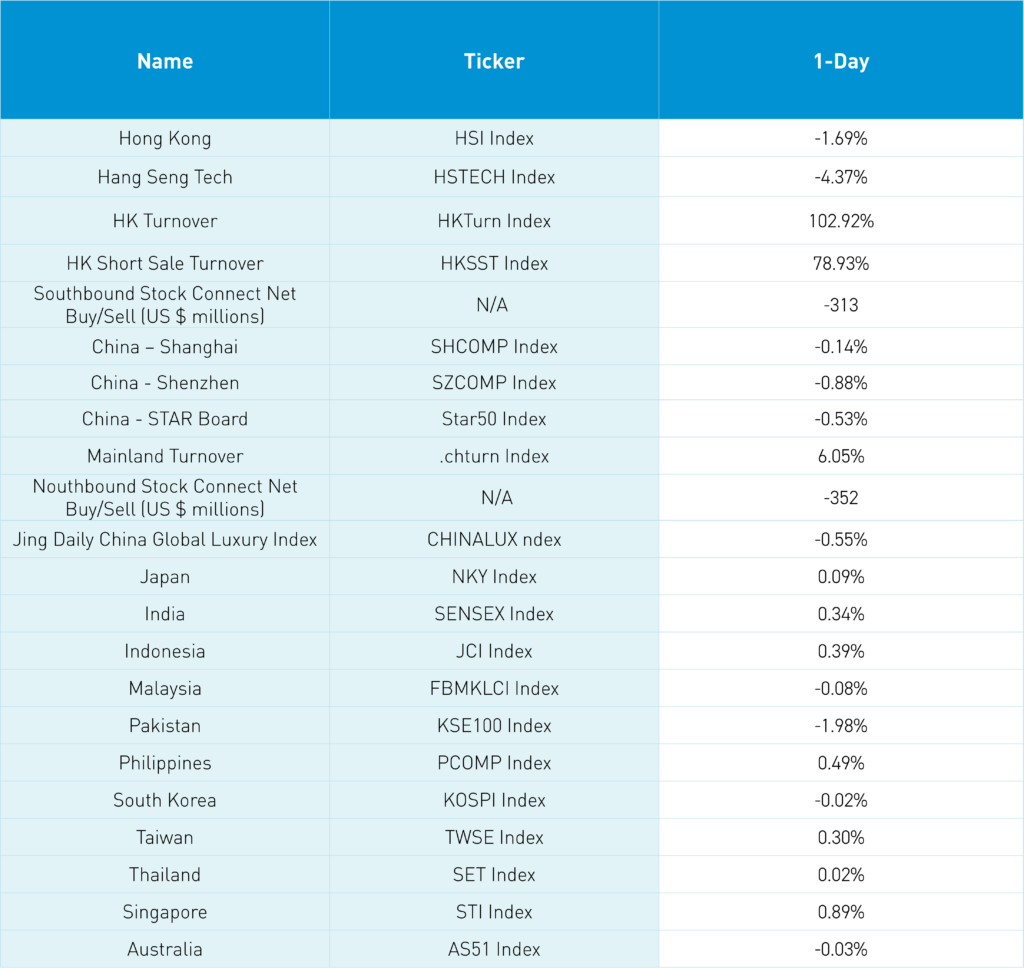

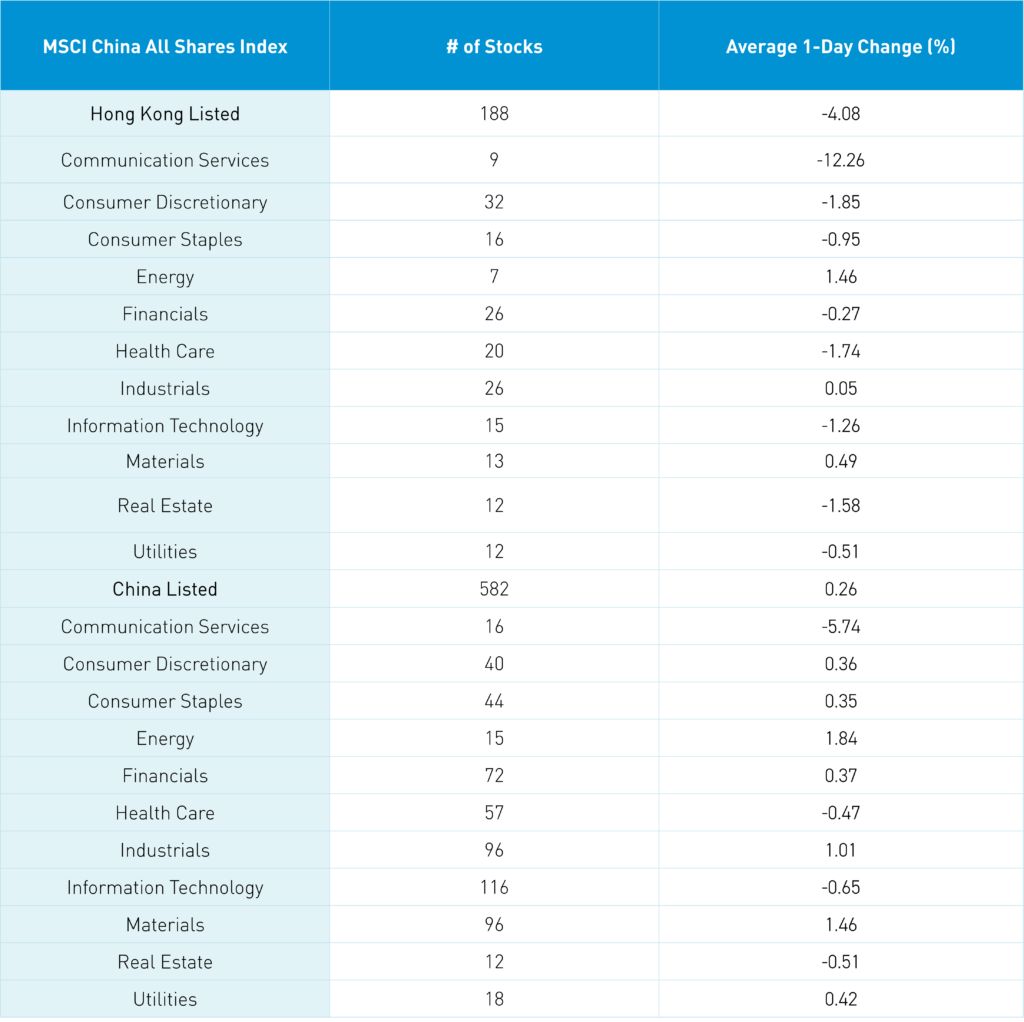

The Hang Seng and Hang Seng Tech indexes fell -1.69% and -4.37%, respectively, on volume that increased +102% from yesterday, which is 134% of the 1-year average. 131 stocks advanced, while 346 stocks declined. Main Board short turnover increased by +78.9% from yesterday, which is 104% of the 1-year average, as 13% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps “outperformed” (i.e. fell less than) the growth factor and small caps. The top-performing sectors were Energy, which gained +1.49%, Materials, which gained +0.52%, and Industrials, which gained +0.09%. Meanwhile, Communication Services fell -12.24%, Consumer Discretionary fell -1.82%, and Health Care fell-1.71%. The top-performing subsectors were energy, materials, and household products. Meanwhile, software, media, and retail were among the worst-performing. Southbound Stock Connect volumes were high as Mainland investors sold a net -$313 million worth of Hong Kong-listed stocks and ETFs. However, China Mobile, CNOOC, and Kingdee were small net buys. Tencent was a sizeable net sell along with the Hong Kong Tracker ETF and the Hang Seng Tech ETF.

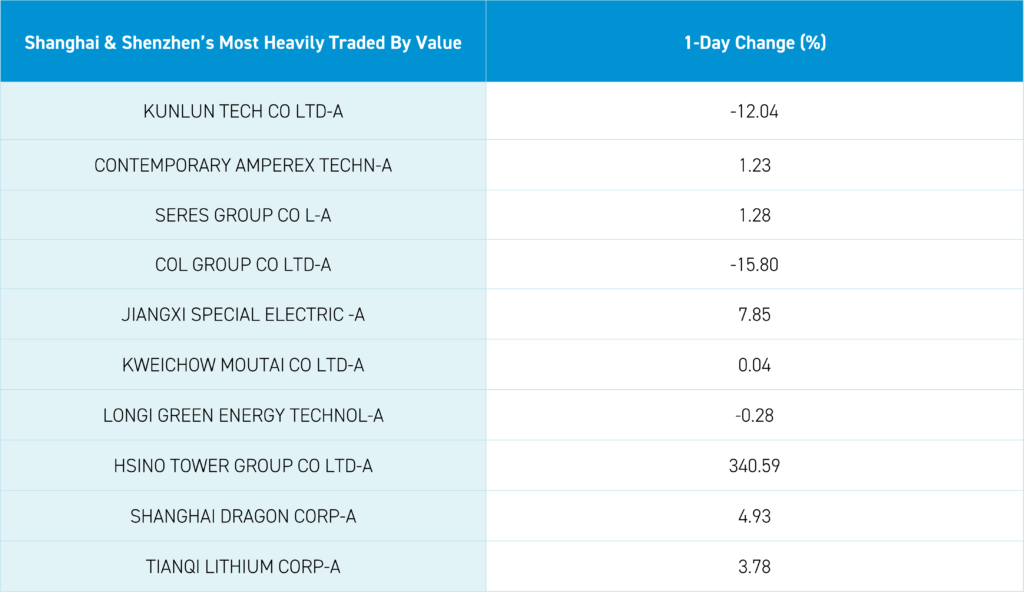

Shanghai, Shenzhen and the STAR Board fell -0.14%, -0.88%, and -0.53%, respectively, on volume that increased +6.05% from yesterday, which is 89% of the 1-year average. 943 stocks advanced while 3,953 stocks declined. The value factor and large caps “outperformed/fell less than the growth factor and small caps. The top-performing sectors were Energy, which gained +1.72%, Materials, which gained +1.34%, and Industrials, which gained +0.89%. Meanwhile, Communication Services fell -5.85%, Technology fell -0.77%, and Real Estate fell -0.63%. The top-performing subsectors were building materials, aerospace/military, and base metals. Meanwhile, the internet, media, and education were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$352 million worth of Mainland stocks. However, Gree, Changan Auto, and CATL were small net buys. Meanwhile, Bank of Ningbo, China Merchants Bank, and Midea were small net sells. CNY and the Asia Dollar Index both rallied versus the US dollar. Treasury bonds rallied along with copper and steel.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.13 versus 7.14 yesterday

- CNY per EUR 7.86 versus 7.84 yesterday

- Yield on 1-Day Government Bond 1.13% versus 1.22% yesterday

- Yield on 10-Year Government Bond 2.59% versus 2.59% yesterday

- Yield on 10-Year China Development Bank Bond 2.74% versus 2.75% yesterday

- Copper Price +0.35%

- Steel Price 1.21%