AI Haves Versus The AI Have-Nots

2 Min. Read Time

Key News

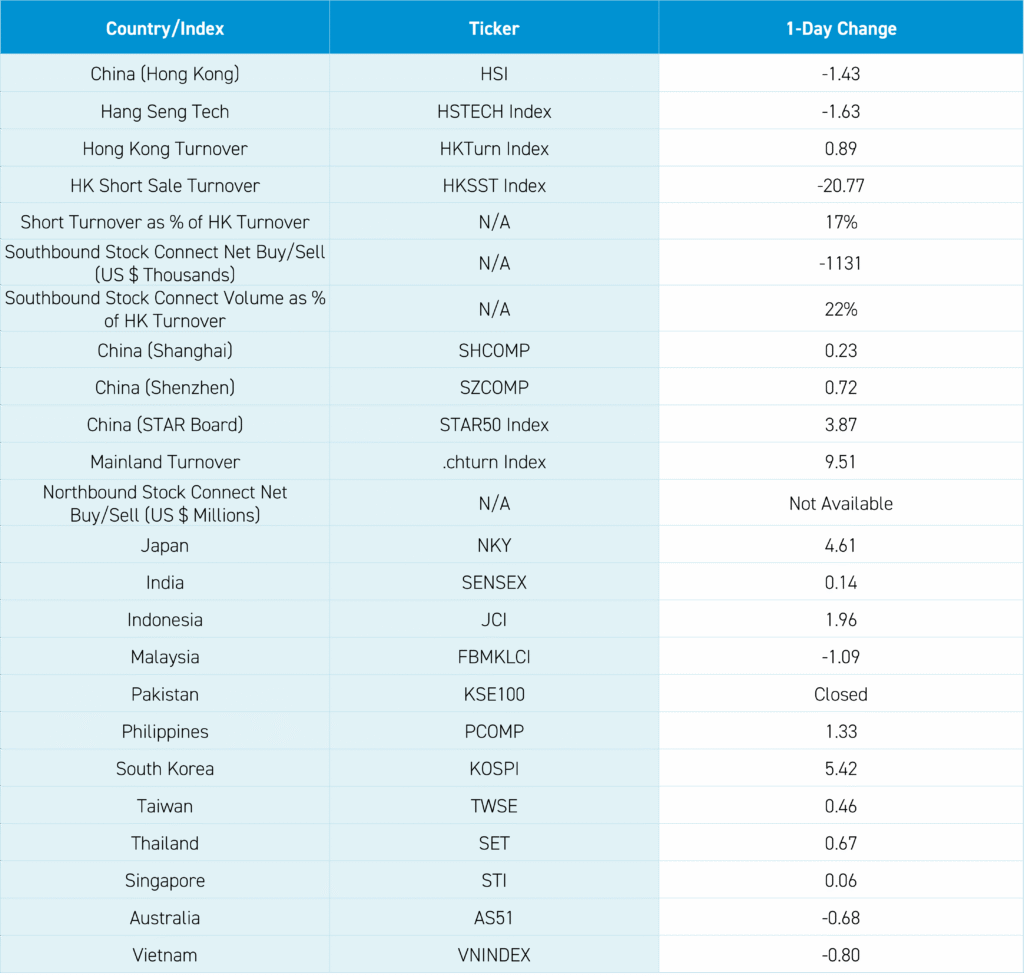

Asian AI plays cheered Micron's beat, which lifted China's Science and Technology (STAR) Board, Japan, and Korea, while the non-AI markets of Indonesia and the Philippines also rebounded, Hong Kong underperformed, and Pakistan was closed for Ashura.

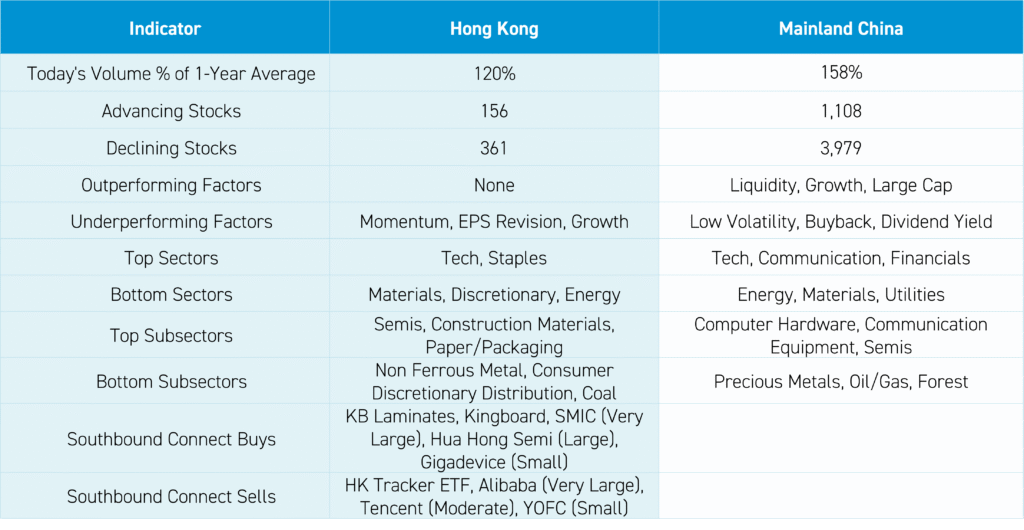

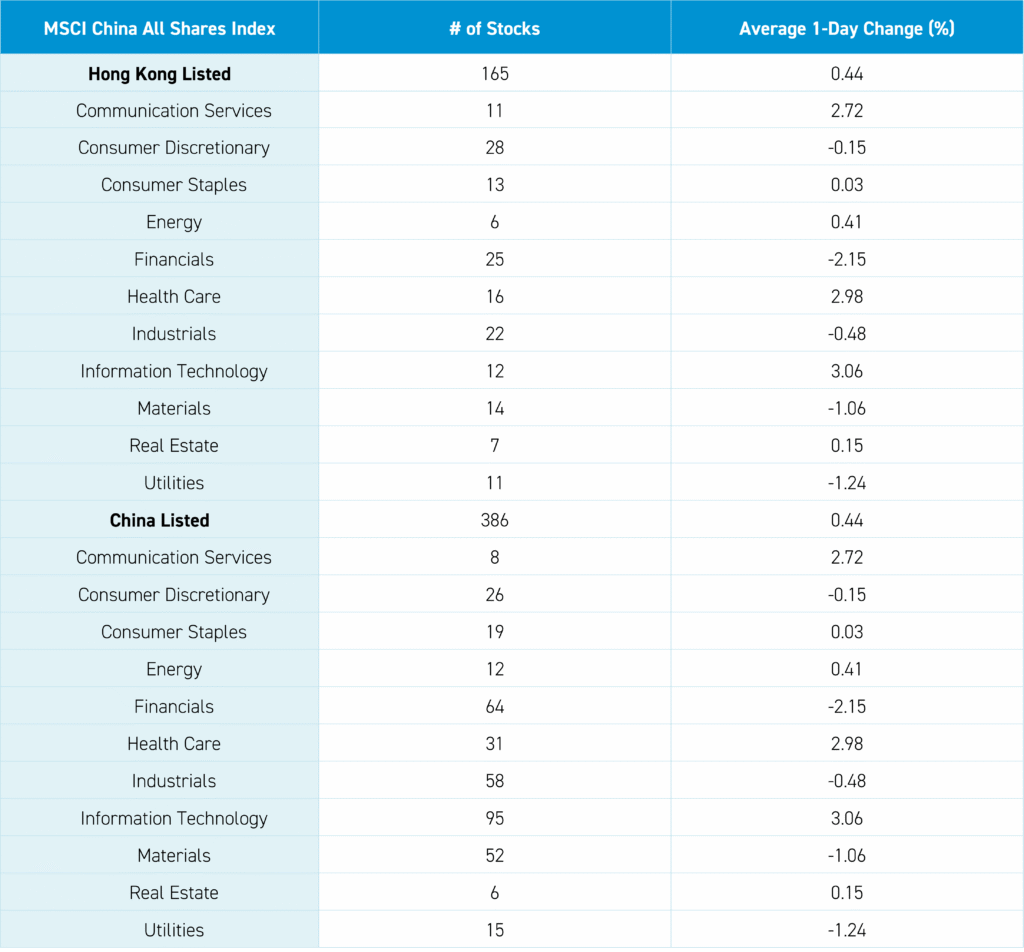

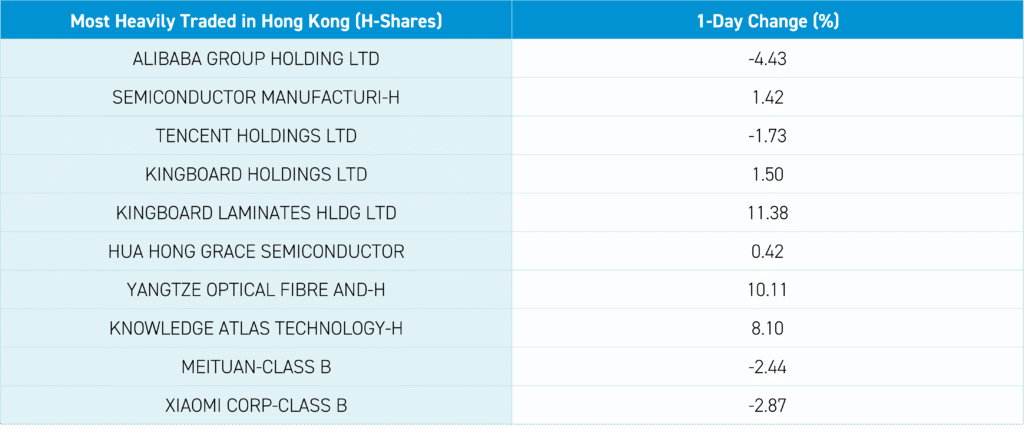

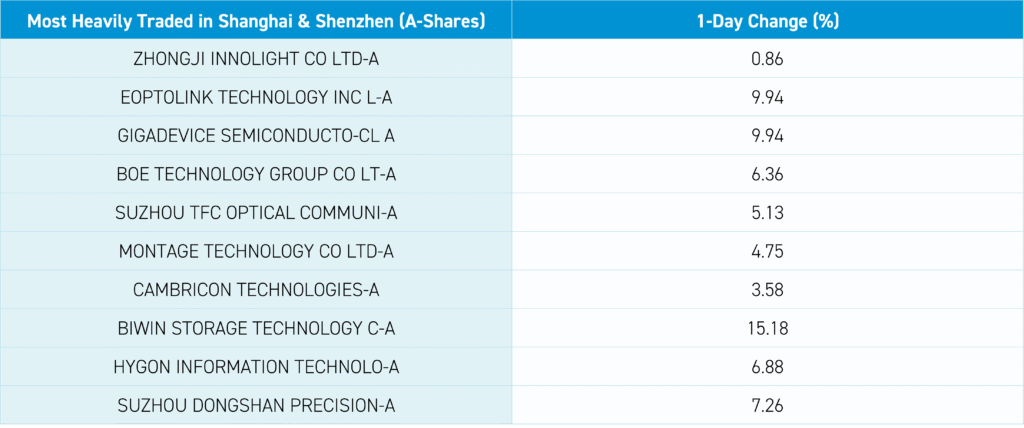

The disparity between the AI haves versus the AI have-nots was clear, as Korea's KOSPI gained +5.42%, and remains up +98% year-to-date (YTD), though it had 476 decliners versus 297 advancers, while Korea's KOSDAQ fell -2.36% and is down -10% YTD. The same was true again for Hong Kong, as technology hardware and semiconductors gained, while virtually everything else was down. Hong Kong had 156 advancers versus 361 decliners, except for pharmaceuticals' positive day. It was a similar story in Mainland China, which had 1,108 advancers versus 3,979 decliners, as technology hardware, electronic equipment, communication equipment, semiconductors, and electrical equipment all outperformed, while telecom, banks, oil & gas, and non-ferrous metals underperformed. Semiconductors powered the STAR Board higher by +3.87%, versus Shanghai, which only gained +0.21%, and Shenzhen, which only gained +0.72%.

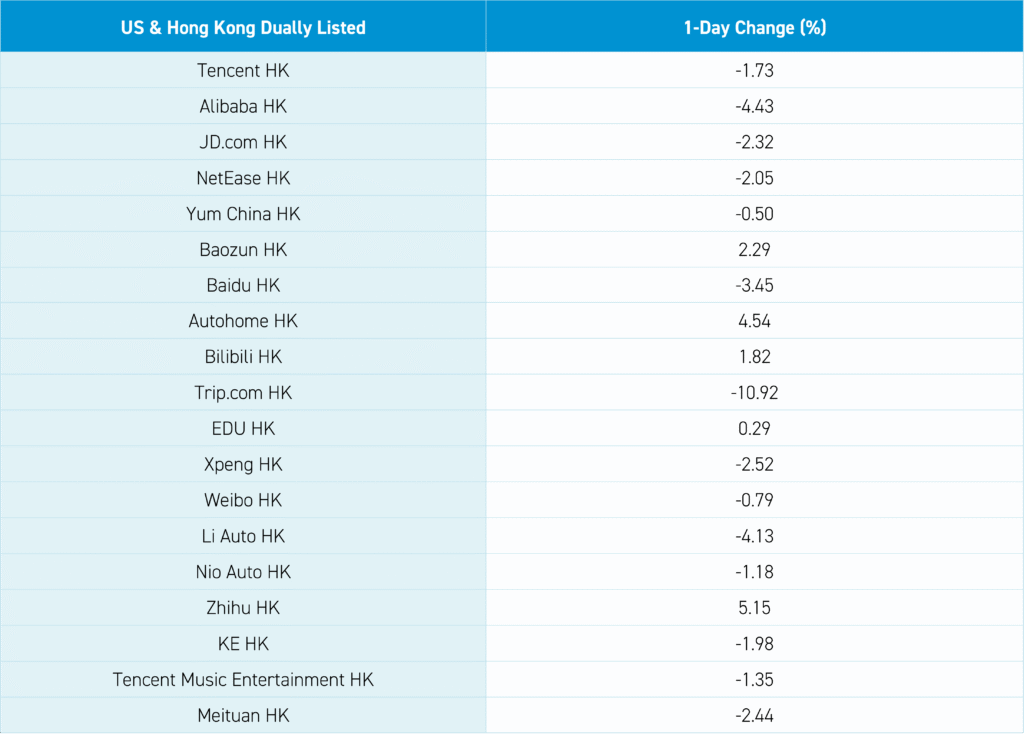

One factor in Hong Kong's weakness was Alibaba, which fell -4.43%, as Anthropic accused the company of accessing their Claude AI through fake accounts in a letter to several members of Congress. While US-China relations are improving under Trump, Congress remains outright hostile, which explains why the letter went to Congress rather than the White House. Mainland investors sold 287 million (HKD 2.25 billion) of Alibaba, along with a very big sell in the Hong Kong Tracker ETF. Alibaba repurchased 992,000 shares of its US-listed shares yesterday, according to today's Hong Kong filing.

It was a bit of a Groundhog Day in both Hong Kong and Mainland China, so we'll keep things brief and concise. The National Development and Reform Commission (NDRC) and the National Energy Administration issued a joint 15th Five-Year Plan for the Construction of a New Energy System. The 2030 goal is "the proportion of non-fossil energy generation reaching 50% as the main body of electricity consumption". CATL gained +1.65% in Mainland China and fell -0.69% in Hong Kong, as it plans 36 battery-swapping stations in Hong Kong by 2030, having already installed two. Ministry of Commerce (MoC) spokesman He Yadong stated that the US and China will hold "consultations" to eliminate $30 billion in reciprocal tariffs. He noted that airplanes and farm goods were a "mutually beneficial" area.

One interesting development was Hong Kong's SFC, its financial regulator, not allowing Hong Kong banks to provide new swaps to Mainland investors for foreign stock exposure. I wonder whether the growth in the Hong Kong-listed SK Hynix levered ETF is causing concern, as assets are approaching $12 billion. This could be part of the broader effort to enforce capital controls, as seen in actions against Chinese brokers and insurance companies. The timing is interesting, as the renminbi value against the US dollar has been quite resilient.

Trip.com fell -10.92% today in Hong Kong after reporting Q1 financial results after the US close yesterday. While revenue beat analyst expectations, adjusted net income and adjusted EPS both missed. Management'second-quarter forecast did not help, stating that "the slower pace of growth is expected to have a corresponding impact on margins and bottom-line results" due to "impacts from macreconomic headwinds such as elevated energy pricing and geopolitical volatility". Management noted their ongoing investigation, the January 2026 notice of investigation from the State Administration for Market Regulation (SAMR) that "it had commenced an investigation into whether the Company has abused or is abusing a dominant market position to engage in monopolistic conduct pursuant to the PRC's Anti-Monopoly Law." The regulatory overhang and uncertainty won't help. However, one assumes they'll receive a nominal fine.

- Revenue increased 17% to RMB 16.2B ($2.4B) from RMB 13.83B, versus expectations of RMB 15.86B

- Adjusted Net Income decreased to RMB 3.9B ($568mm) from RMB 4.19B, versus expectations of RMB 4.19B

- Adjusted EPS decreased to RMB 5.73 ($0.83) from RMB 5.96 versus expectations of RMB 6.09

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.79 versus 6.81 yesterday

- CNY per EUR 7.70 versus 7.72 yesterday

- Yield on 10-Year Government Bond 1.74% versus 1.75% yesterday

- Yield on 10-Year China Development Bank Bond 1.82% versus 1.82% yesterday

- Copper Price -1.84%

- Steel Price -0.22%