AI Pullback Bites Apple’s Supply Chain, Week in Review

2 Min. Read Time

Week in Review

- Asian equities were mostly lower for the week, though Mainland China's STAR (Science & Technology) Board and Vietnam managed gains, while Hong Kong and Korea underperformed.

- The "Tale of Two Chinas" was on display all week, as Mainland-listed hardware technology stocks continued to outperform Hong Kong by a wide margin.

- The US and China agreed to hold consultations to eliminate $30 billion in reciprocal tariffs, with officials noting airplanes and farm goods as a "mutually beneficial" area, pointing to continued trade progress.

- Alibaba executed significant share buybacks this week, repurchasing more than 2 million US-listed shares.

Key News

Asia was largely lower as AI "picks and shovels" recent winners were hit hard following Apple’s price hike announcement and Microsoft’s Xbox price hike. Japan, Korea, and Taiwan were hit, along with Hong Kong, Mainland China, Thailand, and Indonesia. Meanwhile, Pakistan and India were closed for Ashura and Muharram, respectively.

The AI winners pullback combined with the Apple news weighed on its supply chain, hitting Mainland China-listed technology hardware, semiconductors, electronic equipment, communications equipment, and electrical equipment. It is worth noting that Mainland semiconductor materials and equipment managed to buck the trend, which limited the decline in Mainland China's Science and Technology (STAR) innovation Board. They were the anomaly, as the market suffered a wide sell-off, as non-ferrous metals, insurance, brokers, auto, machinery, chemicals and machinery were all hit hard.

It was a very similar story in Hong Kong, as AI winners, including semiconductors, electrical equipment, and technology hardware were all hit hard, along with internet, auto, insurance, and brokers. Breadth was awful, as decliners significantly outnumbered advancers was, and the Hang Seng Index closed below the 24,000 level and the Hang Seng Tech Index closed below 4,400.

Alibaba fell -5.70%, as Anthropic's compliant to Congress is concerning. Their argument, however, does not appear to be very data or evidence-driven. UBS’ report on companies gravitating to lower-cost Chinese AI large language models (LLMs) from expensive US AI LLMs could be the real motivation. Alibaba faced selling pressure overnight, as Mainland investors sold a net $289 million worth of shares (HKD 2.27 billion) via Southbound Stock Connect. However, the company reported they bought 1million US-listed shares this morning, which is a positive sign.

NetEase gained +3.14% after announcing it will convert its Hong Kong listing from a secondary listing to a primary listing on June 30th, which would allow it to be added to Stock Connect.

Six companies went public today in Hong Kong, raising HKD 20 billion, bringing the year-to-date (YTD) total to 78 IPOs, raising HKD 200 billion. Does anybody in Hong Kong remember that increasing supply without increasing demand leads to lower prices? There were also reports of Hong Kong IPO lock-ups expiring, which would put additional selling pressure on the market.

The State Administration for Market Regulation (SAMR) held the second 2026 Symposium on Fair Competition for Enterprises, which included emphasizing “anti-competitive practices in digital platforms”. There were reports that the restaurant delivery war subsidies being removed would be a benefit for shareholders in JD and Meituan.

It was disappointing to see internet names off, though it was a broad sell off so little place to hide.

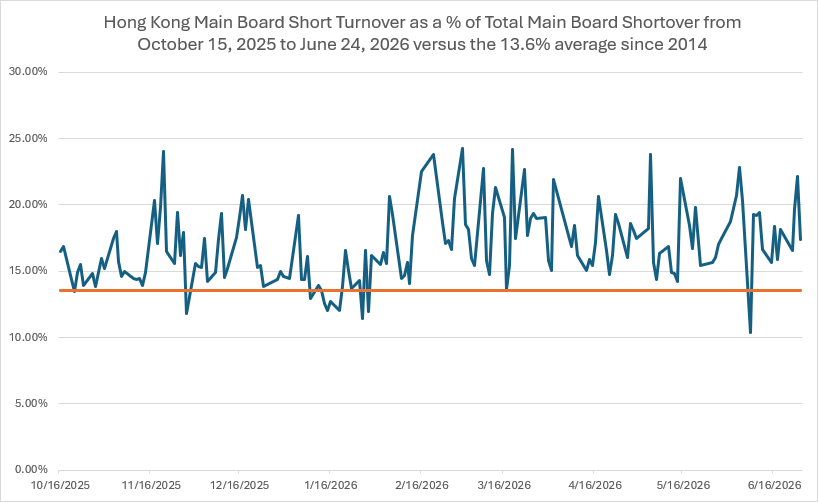

Below is a chart of HK short selling volume as a percentage of total Main Board volume.

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.80 versus 6.80 yesterday

- CNY per EUR 7.77 versus 7.73 yesterday

- Yield on 10-Year Government Bond 1.73% versus 1.74% yesterday

- Yield on 10-Year China Development Bank Bond 1.82% versus 1.82% yesterday

- Copper Price +0.46%

- Steel Price -0.45%