Bilibili Higher As Mainland Investors Buy Alibaba In Size (Again)

6 Min. Read Time

| Upcoming Live Webinar |

| Join us tomorrow at 10:30 am EDT for: China, Land of Breakthroughs? A Conversation With Gavekal’s Louis-Vincent Gave Please click here to register |

Key News

Asian equities had a strong session overnight, led by Hong Kong, Taiwan, South Korea, and Singapore.

The Hang Seng Index and Hang Seng Tech Index both closed above recent resistance levels at 26,000 and 5,900, respectively. The Hang Seng Index reached a 52-week high and the highest level since October 2021, while the Hang Seng Tech Index did not surpass its September 2024 stimulus high, suggesting additional upside potential remains.

Mainland China’s August inflation data missed expectations, with the Consumer Price Index (CPI) falling -0.4% versus July’s 0% and the consensus forecast of -0.2%. The Producer Price Index (PPI) declined -2.9%, matching expectations, and improved from July’s -3.6%. Core CPI, which excludes food and energy, grew +0.9% for the fourth consecutive month, an encouraging trend not widely reported in headlines.

It has been speculated that a fully implemented anti-involution campaign could end Mainland China’s deflationary spiral, affecting both domestic and global markets. J.P. Morgan recently suggested that anti-involution could be a major market theme over the next two years.

Hong Kong saw strong volumes and broad market participation, with banks, insurance, and internet sectors outperforming. Notably, Hong Kong-listed heavyweights Contemporary Amperex Technology Co. Limited (CATL) declined -1.16% despite a lithium mine reopening, Xiaomi fell -2.22%, and BYD fell -0.28% despite news that executives bought 488,200 shares in September, costing Renminbi (RMB) 52.327 million. This weakness may be linked to a Ministry of Industry and Information Technology (MIIT) regulatory examination into online auto sales, as some dealers are suspected of selling new cars as used to qualify for subsidies.

Bilibili surged +7.57% after releasing a video about its upcoming game, San Guo: N Card, with player testing to begin in October. Alibaba Group added +0.63% following a strong day of net buying via Southbound Stock Connect, while Tencent rose +1.04% and Meituan climbed +2.06%.

Alibaba announced the launch of its “Amap Street Stars” feature, enabling 170 million daily users of its map app to find everything from local restaurants and hotels to tourist attractions based on navigation patterns and genuine user reviews. The company will spend RMB 1 billion in subsidies on “consumer transportation and offline spending” to enhance connectivity between online and offline commerce, with optics positive for regulators as in-person dining has suffered amid a delivery price war that keeps consumers home.

NIO dropped -2.26% to Hong Kong $46.72 after announcing plans to raise nearly $1 billion by selling 181 million shares at Hong Kong $42.86 to $44.46 to fund further electric vehicle (EV) growth, with dilution weighing on shares. The China Federation of Logistics and Purchasing’s E-Commerce Logistics Index rose for the sixth consecutive month, hitting an all-time high based on August data. This is a newer data point to watch and will be examined further in an upcoming note.

Mainland sector performance flipped, with semiconductors and technology hardware stocks, such as electronic and communication equipment, leading today’s gains after being the worst performers yesterday. The most heavily traded names in the Mainland session included Victory Giant Technology (+12.01%), Eoptolink Technology (+6.23%), Zhongji Innolight (+7.16%), and Foxconn Industrial (+10%). Despite today’s move, the three sub-sectors remained down over the last five trading days. Luxshare Precision gained +0.8% for an 11.27% increase over five days. Green tech stocks were off, with CATL -1.24%, Tongwei -6%, and Sungrow -1.22%. Both Shanghai and Shenzhen remained off recent highs, which may be healthy after the recent strong rally.

The 17th meeting of the 14th National People’s Congress (NPC) Standing Committee convened in Beijing, featuring agency updates. Zheng Gangjie, Director of the National Development and Reform Commission, highlighted the need to “release the potential of domestic demand” and “promote the deep integration of scientific and technological innovation with industrial innovation” in the second half of the year. Ministry of Finance Minister Lan Fo’an focused on “more active fiscal policies,” while Ministry of Culture and Tourism Minister Sun Yeli emphasized tourism initiatives linked to domestic consumption. There has been no visible market reaction so far, but these developments appear positive.

The 16th Five-Year Plan will launch next year, with preparations already underway. Early indications point to a continued focus on artificial intelligence, technology, science, and private enterprise.

NBC News reported that U.S. lawmakers will visit China this month, marking the first visit by a U.S. House of Representatives delegation since 2019, according to Reuters.

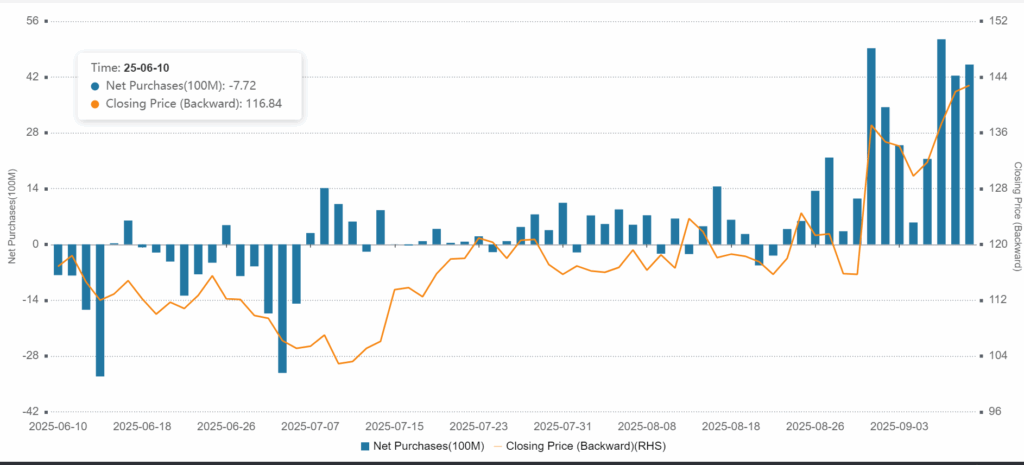

Alibaba’s Hong Kong Stock Price and Net Flow From Southbound Stock Connect:

Last Night's Performance

| Country / Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 1% |

| Hang Seng Tech | HSTECH Index | 1.3% |

| Hong Kong Turnover | HKTurn Index | -2% |

| Hong Kong Short Sale Turnover | HKSST Index | -15.5% |

| Short Turnover as a % of Hong Kong Turnover | N/A | 13.7% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 966.30 |

| China (Shanghai) | SHCOMP Index | 0.1% |

| China (Shenzhen) | SZCOMP Index | 0.3% |

| China (STAR Board) | Star50 Index | 1.1% |

| Mainland Turnover | .chturn Index | -6.6% |

| Northbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0.1% |

| Japan | NKY Index | 0.9% |

| India | SENSEX Index | 0.4% |

| Indonesia | JCI Index | 0.9% |

| Malaysia | FBMKLCI Index | 0.2% |

| Pakistan | KSE100 Index | 0.2% |

| Philippines | PCOMP Index | 0% |

| South Korea | KOSPI Index | 1.7% |

| Taiwan | TWSE Index | 1.4% |

| Thailand | SET Index | 0.2% |

| Singapore | STI Index | 1.1% |

| Australia | AS51 Index | 0.3% |

| Vietnam | VNINDEX Index | 0.4% |

| Indicator | Hong Kong | Mainland |

|---|---|---|

| Today's Volume % of 1-Year Average | 124% | 124% |

| Advancing Stocks | 294 | 2434 |

| Declining Stocks | 190 | 2497 |

| Outperforming Factors | Dividend Yield, Value, Liquidity | Momentum, Large Cap, Growth |

| Underperforming Factors | Value, Dividend Yield, Low Volatility | |

| Top Sectors | Financials, Real Estate, Communication | Communication, Tech, Staples |

| Bottom Sectors | Healthcare, Tech | Materials, Healthcare, Industrials |

| Top Subsectors | Semis, Banks, Household/Personal Products | Communication Equipment, Electronic Components, Catering/Tourism |

| Bottom Subsectors | Consumer Durables/Apparel, National Defense, Steel | Fertilizer/Pesticides, Chemical Raw Material, Comprehensize |

| Southbound Connect Buys | Alibaba (Very Large), SMIC (Small) | |

| Southbound Connect Sells | Akeso, Pop Mart (Large), Xiaomi (Moderate), Kingsoft Cloud (Small), Meituan, Tencent (Tiny) |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | 0.8 |

| Communication Services | 9 | 1.29 |

| Consumer Discretionary | 28 | 0.5 |

| Consumer Staples | 13 | 0.95 |

| Energy | 6 | 0.8 |

| Financials | 24 | 2.14 |

| Health Care | 12 | -1.68 |

| Industrials | 21 | 0.86 |

| Information Technology | 10 | -1.09 |

| Materials | 10 | 0.22 |

| Real Estate | 7 | 1.82 |

| Utilities | 12 | 0.45 |

| Mainland China Listed | 395 | 0.29 |

| Communication Services | 7 | 3.54 |

| Consumer Discretionary | 29 | -0.42 |

| Consumer Staples | 24 | 0.31 |

| Energy | 13 | -0.67 |

| Financials | 64 | 0.01 |

| Health Care | 32 | -0.94 |

| Industrials | 61 | -0.73 |

| Information Technology | 90 | 2.74 |

| Materials | 54 | -1.36 |

| Real Estate | 6 | -0.17 |

| Utilities | 15 | 0.01 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 1 |

| Alibaba HK | 9988 HK Equity | 0.6 |

| JD.com HK | 9618 HK Equity | 3.6 |

| NetEase HK | 9999 HK Equity | 2.6 |

| Yum China HK | 9987 HK Equity | 0.8 |

| Baozun HK | 9991 HK Equity | -0.5 |

| Baidu HK | 9888 HK Equity | 2.8 |

| Autohome HK | 2518 HK Equity | 2.1 |

| Bilibili HK | 9626 HK Equity | 7.6 |

| Trip.com HK | 9961 HK Equity | 1.7 |

| EDU HK | 9901 HK Equity | 2.2 |

| Xpeng HK | 9868 HK Equity | -0.6 |

| Weibo HK | 9898 HK Equity | 6 |

| Li Auto HK | 2015 HK Equity | 0 |

| Nio Auto HK | 9866 HK Equity | -2.3 |

| Zhihu HK | 2390 HK Equity | -1.4 |

| KE HK | 2423 HK Equity | 3.1 |

| Tencent Music Entertainment HK | 1698 HK Equity | 3.4 |

| Meituan HK | 3690 HK Equity | 2.1 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| ALIBABA GROUP HOLDING LTD | 0.6 |

| TENCENT HOLDINGS LTD | 1 |

| MEITUAN-CLASS B | 2.1 |

| POP MART INTERNATIONAL GROUP | -4.5 |

| XIAOMI CORP-CLASS B | -2.2 |

| SEMICONDUCTOR MANUFACTURI-H | 3.6 |

| JD.COM INC-CLASS A | 3.6 |

| BAIDU INC-CLASS A | 2.8 |

| BYD CO LTD-H | -0.3 |

| AKESO INC | -4.7 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| VISUAL CHINA GROUP CO LTD-A | 0.1 |

| SHANTUI CONSTRUCTION MACHI-A | -1.7 |

| VICTORY GIANT TECHNOLOGY -A | 12 |

| EOPTOLINK TECHNOLOGY INC L-A | 6.2 |

| ZHONGJI INNOLIGHT CO LTD-A | 7.2 |

| FOXCONN INDUSTRIAL INTERNE-A | 10 |

| CAMBRICON TECHNOLOGIES-A | 3.7 |

| SUNGROW POWER SUPPLY CO LT-A | -1.2 |

| WUXI LEAD INTELLIGENT EQUI-A | 4.5 |

| CONTEMPORARY AMPEREX TECHN-A | -1.2 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.12 versus 7.12 yesterday

- CNY per EUR 8.33 versus 8.37 yesterday

- Yield on 10-Year Government Bond 1.90% versus 1.86% yesterday

- Yield on 10-Year China Development Bank Bond 2.04% versus 1.91% yesterday

- Copper Price -0.04%

- Steel Price -0.77%