CATL Charges Up While Investors Should Ask If It’s Not Always Sunny Optical in Apple

4 Min. Read Time

Key News

Asian equities were largely higher, less Mainland China, Hong Kong, and South Korea.

While Mainland China and Hong Kong equities had a tough January, it is interesting that South Korea has really rolled over while Taiwan’s performance was negative and India is flat/down. Professional investors are careful about their top holdings at the end of the month/quarter due to investor disclosure leading to “window dressing,” i.e., selling what’s done poorly and buying what’s done well. We did not anticipate buying today, nor did it materialize as buyers stayed sidelined despite several positives.

January's Manufacturing PMI met expectations of 49.2, which is not a big deal, nor are you going to read about how the Manufacturing PMI increased from December’s 49. While output increased, export orders were tepid indicating the global economy is slowing. Small and medium-sized companies continue to struggle versus larger companies, which is problematic, as the former have far more employees than large companies.

The Non-manufacturing PMI actually increased and beat expectations with a reading of 50.7 versus estimates of 50.6 and December’s 50.4. There were several positives, including speculation that Presidents Biden and Xi will have a call soon. Meanwhile, Shanghai loosened some more home purchase restrictions while Suzhou removed all restrictions. The IMF raised China’s 2024 GDP forecast to 4.6% (2X the US’ 2.1%). President Xi attended a Central Committee on the 14th Five Year Plan.

Buyers have yet to step into the market in a significant way, as Mainland investors are buying bonds, knowing that a rate cut will occur, as the 10-year Treasury price hit a 52-week high and the yield hit a 52-week low of 2.43%, which is also the lowest level since data goes back to 2006. The bond buying is coming at the expense of Mainland-listed active China equity funds being sold and putting pressure on stocks, including Hong Kong-listed stocks.

Preliminary results continue to roll in, with CATL gaining +7.7% after yesterday’s strong release though Tianqi Lithium fell -7.72% as net income is expected to fall from -62% to -72%. Sunny Optical fell -11.66% as profit dropped about 50% to 55% as the cell phone (iPhone) lens maker, which could be a canary in the coal mine for those who own the Fruit (i.e. Apple).

Hong Kong-listed electric vehicle (EV) stocks were lower as Commerce Secretary Gina Raimondo called China-made EVs “scary,” due to the potential data transfer. Chinese EVs are scary to US auto manufacturers who are incapable of building EVs (or even hybrids) at the scale and affordable prices China does. This is why the companies should partner with US automakers to make them here in the US.

WuXi AppTec was off another -4.09% which brings the loss of US investors (based on SEC filed 13Fs) to $1.437 billion after members of Congress recommended restricting federally-funded medical providers from using WuXi. Why doesn’t the company publicly state that they will sue as the accusations are baseless is beyond me. Remember, TikTok won in US Court as acquisitions not backed by fact are libel, in my opinion. Remarkable to think a company that wants to cure cancer and employs thousands of US employees across a dozen US facilities is the target of Congress. Interesting that Northbound Stock Connect again had a positive net inflow, a sign the stabilization fund might exist, though a fund with several hundred billion can’t stop the market’s decline. Investors want to see definitive policies to support the economy. With that said, gosh darn, these stocks are cheap!

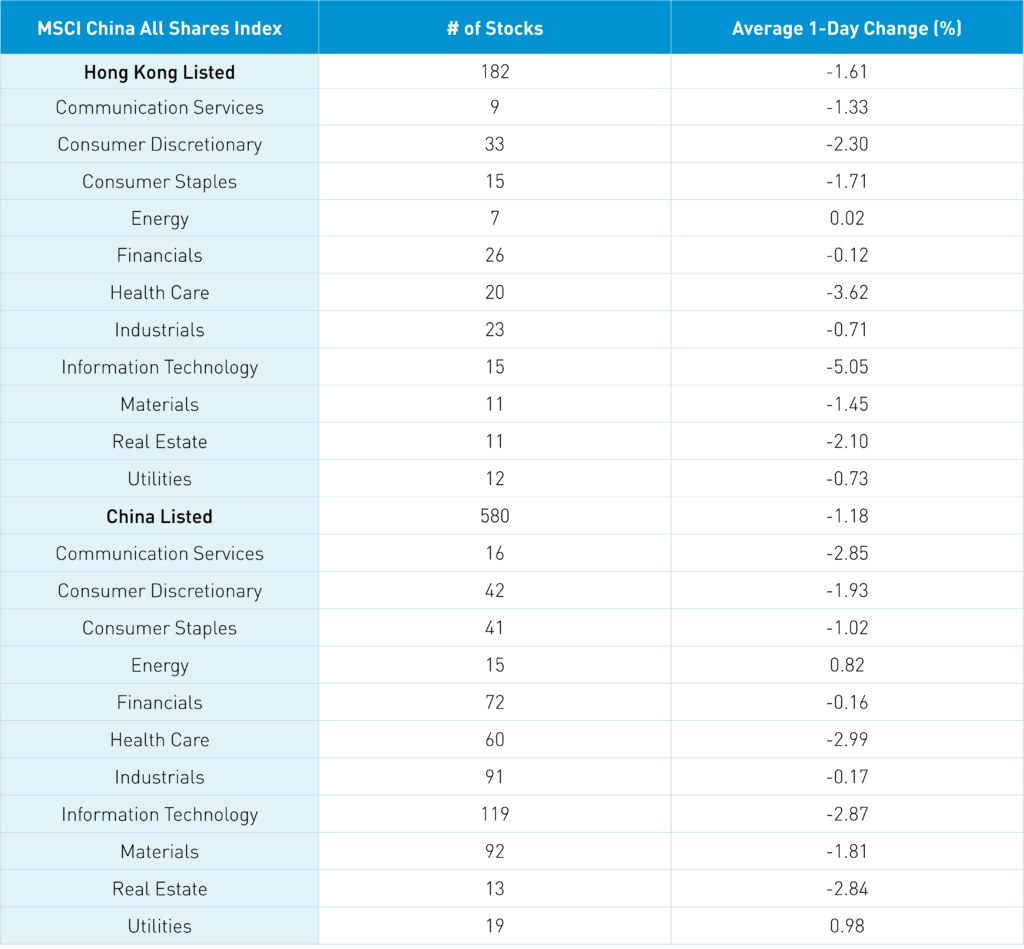

The Hang Seng and Hang Seng Tech fell -1.39% and -3% on volume +4.2% from yesterday, 98% of the 1-year average. 85 stocks advanced, while 396 declined. Main Board short turnover increased by +9.93% from yesterday, 96% of the 1-year average, as 17% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative, with the value factor and large caps “outperforming”/falling less than the growth factor and small caps. Energy was the only positive sector, gaining +0.02%, while tech -5.05%, healthcare -3.62% and discretionary -2.3%. The top sub-sectors were household/personal products, business/professional services, and media, while technical hardware, pharmaceutical, and semis were the worst. Southbound Stock Connect volumes were moderate/light as Mainland investors sold -$80 million of Hong Kong stocks and ETFs with CNOOC, Meituan and China Mobile small net buys while Tencent and Xiaomi small net sells.

Shanghai, Shenzhen, and STAR Board fell -1.48%, -3.03%, and -1.86% on volume +14.89% from yesterday, 88% of the 1-year average. 326 stocks advanced, while 4,679 declined. All factors were negative, with the value factor and large caps “outperforming”/falling less than the growth factor and small caps. Utilities and energy gained +0.98% and +0.82%, while healthcare fell -2.99%, tech -2.88%, and communication -2.85%. The top sub-sectors were motorcycle, insurance, and coal, while education, leisure products, and software were the worst. Northbound Stock Connect volumes were moderate as foreign investors bought $515 million of Mainland stocks with CATL's large net buy, Kweichow Moutai and Sokon's small net buys, while Wuxi AppTec, China Shenhua, and Gree were small net sells. CNY was flat versus the US dollar, while the Asia dollar index was off small. Treasury bonds rallied while copper rose and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.17 versus 7.17 yesterday

- CNY per EUR 7.77 versus 7.78 yesterday

- Yield on 10-Year Government Bond 2.43% versus 2.45% yesterday

- Yield on 10-Year China Development Bank Bond 2.59% versus 2.62% yesterday

- Copper Price +0.33% overnight

- Steel Price -1.29% overnight