Mainland Investors Buy The Dip In Hong Kong, Week in Review

3 Min. Read Time

Week in Review

- Asian equities were mixed but mostly higher this week though the Renminbi and other Asian currencies gained significant ground versus the US dollar.

- Real estate developers benefited from the release of a list of 50 developers on Tuesday that are to receive special financing in a bid to reinvigorate the industry after tightening.

- In its Q3 earnings release, Baidu reported that US semiconductor restrictions are likely to have a muted impact on its cloud/AI and autonomous vehicle businesses, while chipmaker Nvidia warned that the restrictions may begin to impact their sales.

- Trip.com increased its profits 5X in Q3 from a year earlier, according to a Tuesday release, though the travel booking platform’s top line revenue was in line with analyst expectations.

Friday’s Key News

Asian equities were mixed today on a quiet night though managed to trade higher for the week.

There was a significant difference today from yesterday for Hong Kong as the Hang Seng and Hang Seng Tech indexes gained +0.99% and +2.17%, respectively, on Thursday, only to fall -1.96% and -2.24%, respectively, today.

Mainland investors reversed their sale of -$737 million worth of Hong Kong-listed stocks and ETFs from yesterday, buying a healthy +$1.12 billion worth of predominantly ETFs today. The Hong Kong Tracker ETF had its largest inflow since September 5th’s HKD 5.8 billion worth of net inflow while the Hang Seng H Share ETF and Hang Seng Tech ETF had strong inflows as well.

Reuters is reporting that Nvidia is delaying a chip designed for use in China for a few months. Although the report was not cited as factor in today’s trading, technology, specifically semiconductor, stocks were weak in both Hong Kong and Mainland China.

Financials were weak as the “white list” of real estate developers to receive special financing is viewed as weighing on the banks who will be on the hook for financing.

Hong Kong’s most heavily traded stocks were Tencent, which fell -2.43% versus +1.48% yesterday, BYD, which fell -5.54% versus yesterday's gain of +0.75%, Alibaba, which fell -1.36% versus yesterday's +0.52%, Meituan, which fell -2.76% versus yesterday's gain of +0.72%, and Xiaomi, which fell -2.85% versus yesterday's gain of +2.12%.

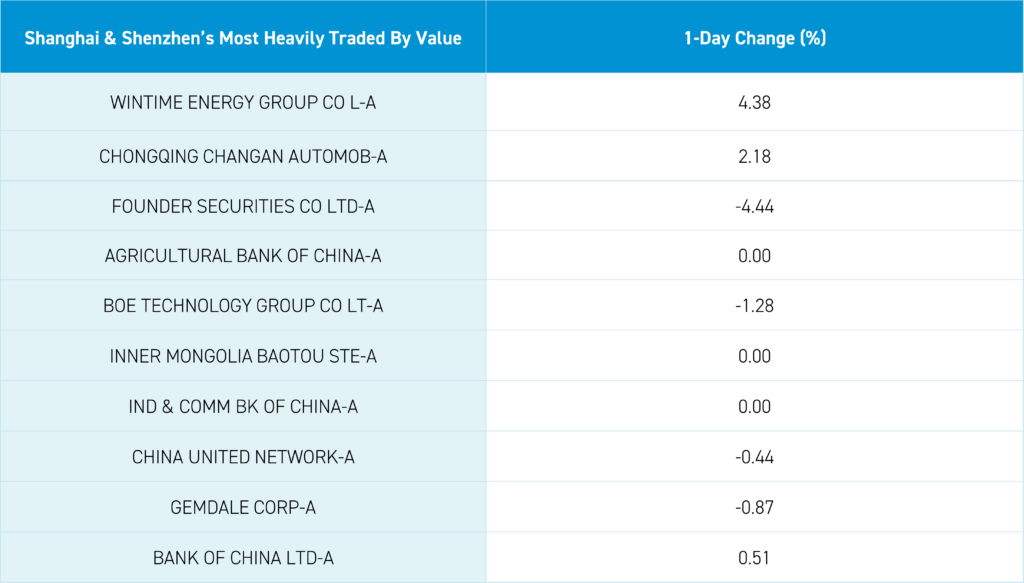

Mainland China's market continues to consolidate after falling for the last two days. The Mainland’s most heavily traded stocks over the last two days were Changan Auto, which gained +2.18% today versus +6.75% yesterday after announcing a partnership with NIO. Foreign investors sold a net -$866 million worth of Mainland stocks today after buying 707 million worth yesterday. CNY’s strong rally versus the US dollar has slowed as the exchange rate closed today at 7.15 versus Monday’s close of 7.16 from 7.31 at the end of October.

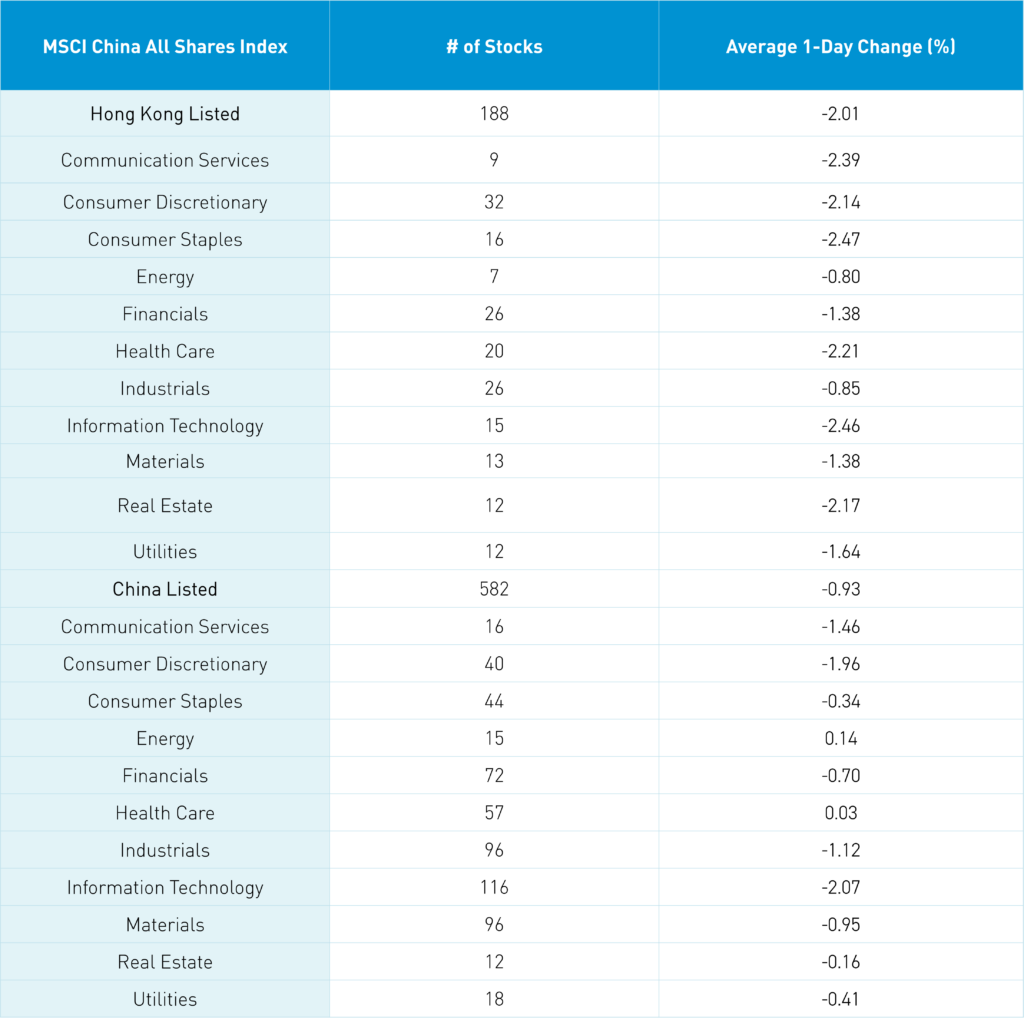

The Hang Seng and Hang Seng Tech indexes fell -1.96% and -2.24%, respectively, on volume that decreased -9.81% from yesterday, which is 81% of the 1-year average. 74 stocks advanced while 415 declined. Main Board short sale turnover increased +28.38% from yesterday, which is 144% of the 1-year average turnover (remember Hong Kong short sale turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps “outperformed” (i.e. fell less than) the growth factor and small caps. All sectors were down as consumer staples fell -2.47%, technology fell -2.46%, and communication services fell -2.39%. All subsectors were lower as autos, software, and technical hardware were off the most. Southbound Stock Connect volumes were moderate as Mainland investors bought a healthy net $1.12 billion worth of Hong Kong-listed stocks and ETFs.

Shanghai, Shenzhen, and the STAR Board fell -0.68%, -1.08%, and -1.48%, respectively, on volume that decreased -1.29% from yesterday, which is 93% of the 1-year average. 918 stocks advanced while 3,953 declined. The value factor and large caps “outperformed” (i.e. fell less than) the growth factor and small caps. Energy and healthcare were the only positive sectors, gaining +0.14% and +0.04%, respectively, while technology fell -2.07%, consumer discretionary fell -1.95%, and communication services fell -1.45%. The top-performing subsectors were coal, agriculture, and pharmaceuticals. Meanwhile, computer hardware, software, and internet were among the worst-performing subsectors. Northbound Stock Connect volumes were moderate/light as foreign investors sold a net -$866 million worth of Mainland stocks. CNY and the Asia Dollar Index both fell versus the US dollar. Treasury bonds, copper, and steel fell.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.15 versus 7.15 yesterday

- CNY per EUR 7.81 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.56% versus 1.56% yesterday

- Yield on 10-Year Government Bond 2.71% versus 2.70% yesterday

- Yield on 10-Year China Development Bank Bond 2.77% versus 2.77% yesterday