May Economic Data Show Online Retail Is Here To Stay

5 Min. Read Time

This week we will be hosting three webinars, please join us.

- The World's Second Largest Bond Market Is Now Open: A Discussion With KraneShares Europe and Sanjay Rao of Bloomberg

June 16th at 2 pm GMT - One Year Review: A Conversation with Nancy Davis of Quadratic Capital and Jonathan Krane, CEO of Krane Funds Advisors

June 16th at 11 am EST - A Larger Piece of the Pie: A Discussion With MSCI on Choosing the Right Mainland China Exposure,

June 18th at 10 am EST

Key News

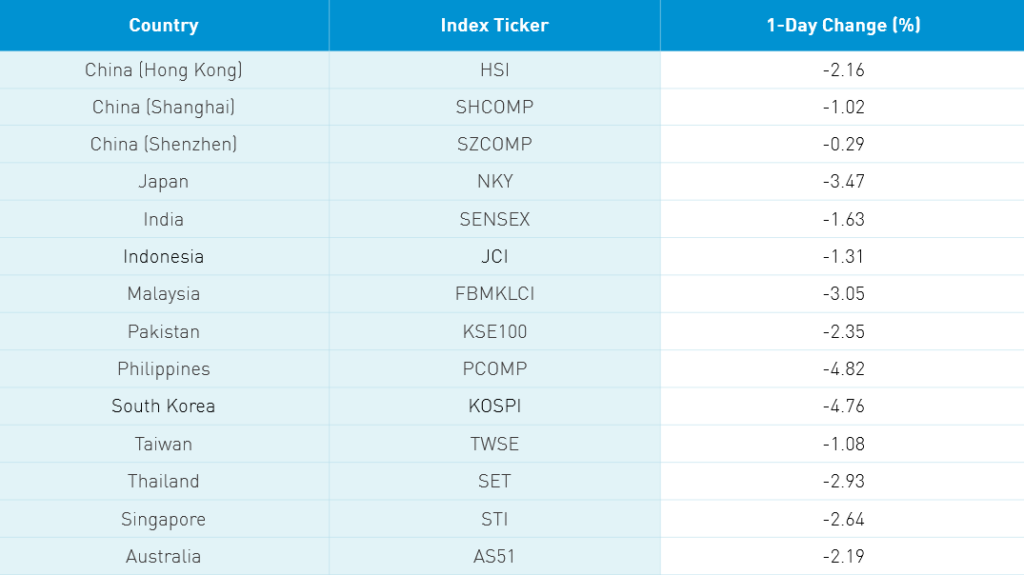

Asian equities mirrored the US equity market’s weakness from Friday on Monday as new coronavirus cases flared in the US, Beijing, and Japan. There were 39 new cases in Beijing that were traced to a food market and led to a tightening in social distancing measures. However, I do not believe a full quarantine will be implemented due to the potential economic consequence.

There was a positive development in US-China political tussle as Secretary of State Pompeo announced he will meet with his Chinese counterpart in Hawaii. China became the number one destination for US exports based on Friday trade data ahead of Canada and Mexico as farm purchases picked up. Chinese economic data discussed below came in below consensus but showed an improvement month over month and the resiliency of online sales is worth pointing out. Hong Kong had a rough day with the “ATM” stocks, volume leaders Tencent -1.68%, Alibaba HK -2.45% and Meituan Dianping -3.6%, all lower on the day. NetEase’s Hong Kong listing was off -2.65% though it was a fairly uniform selloff. Mainland China had a better day though an afternoon selloff pushed both Shanghai and Shenzhen into the red. It is worth noting that the Shenzhen (growth) held up better.

NetEase’s Hong Kong listing (9999 HK) will be added to the Hang Seng Composite Index on June 26th. The Composite Index is a broad measure of over just over 400 stocks versus the more well-known Hang Seng Index, which is comprised of 50 large cap stocks. More important than the Composite Index inclusion was the addition to the Large Cap Index, which is the basis for inclusion in Southbound Stock Connect. Like Alibaba’s Hong Kong listing, there is no indication as to when the stock will become eligible for Southbound Connect.

We spoke with the custodian responsible for the conversion of Alibaba US to Alibaba HK. It is very simple: a book entry conversion done overnight with a cost of $5 per 100 shares or $0.05 a share. We also spoke with a lobbyist on Friday though it remains unclear whether the House will send the Senate bill to committee. The timing of the vote is completely up in the air though a vote is expected before August. The House may amend the Senate version, which would be critical. The Senate bill does prohibit the stocks from trading either on exchange or over the counter, which negates an earlier idea that the stocks would trade on the pink sheets. If the House passes the Senate version, i.e. the nuclear option, it would be an unprecedented move though it is clear from the conversion custodian that institutional investors are exploring and, in some cases, already making the conversion. It is important to remember, however, that there is a three-year window for a solution to be found. That being said, there is no precedent for what is being proposed. None. The slight thawing in the US-China political dialogue could pave the way such a solution. Let’s hope cooler heads prevail!

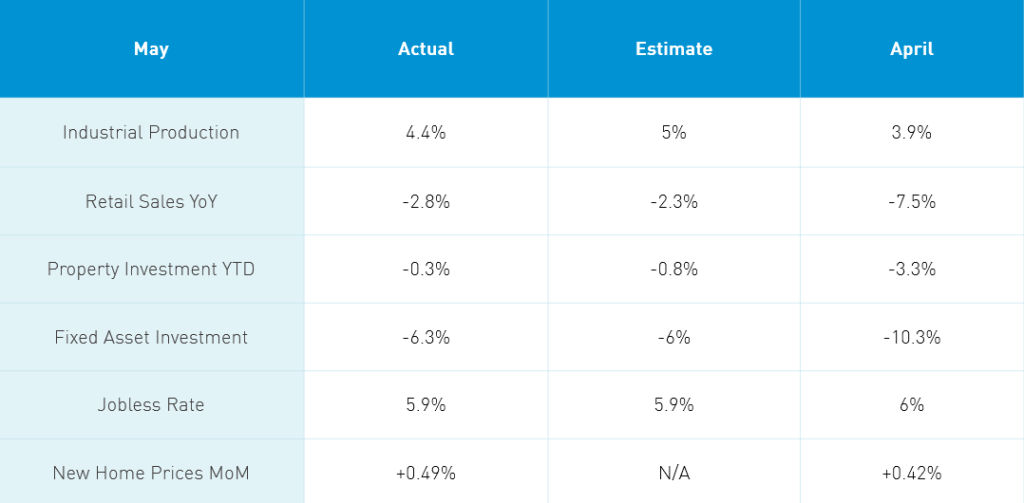

Takeaway: It is important to remember that Retail Sales is Year over Year. If we look at the data, month over month the value of retail sales increased robustly from April’s RMB 2.818 trillion to RMB 3.197 trillion in May. The big culprit in the release was weakness in “catering” i.e. restaurants, which was down -18.9% while retail sales of goods was only down by -0.8%. Meanwhile, online retail sales grew +4.5%! Yes, life is returning to normal, but there is still no cure and no vaccine, so people are still being cautious! The resiliency of online retail post quarantine is a very important for observation for global investors.

Industrial Production came in below economists’ expectations though was similar to retail sales. If we look at the output by industry, we see that food production and agricultural food processing weighed on the broad release. Many industries showed robust pickup. In particular, auto manufacturing jumped from April’s +5.8% to +12.1% YoY. This may explain Tencent’s offer to buy online auto dealer BITA US. As we’ve repeatedly mentioned, China auto sales may have troughed.

Pharmaceutical output did surprisingly drop to +2% from April’s +4.8%, which bears might be watching.

Fixed Asset Investment (FAI)’s weakness is surprising as infrastructure investment has been touted recently as a focus of stimulus. The new home prices hold more significance to me than the market as the vast majority of Chinese household wealth is in property (66%) compared to stocks (2%) and mutual funds (2%). Here in the US, the breakdown is 26% property, 23% stocks and 6% mutual funds.

H-Share Update

The Hang Seng opened lower but turned south in the afternoon session closing -2.16%/-524 index points at 23,776. Volume popped nearly 11% from Friday while breadth was awful with only 1 advancer and 48 decliners. The index was led lower by heavyweights AIA -3.08%/-74 index points, HSBC -2.14%/-48 index points and Tencent -1.68%/-40 index points. CK Infrastructure was the only positive performer +0.24%/+0.2 index point while Techtronic Industries was the day’s worst -4.87%/-15 index points. Chinese domiciled companies were off -1.8% versus -2.61% using the HS China Enterprise and HK 35 Indexes as proxies. The Chinese companies listed in HK within the MSCI China All Shares were down -1.93% with staples -1.02%, utilities -1.17%, financials -1.37%, communication -1.75%, healthcare -1.86%, tech -1.93%, industrials -1.94%, energy -2.25%, materials -2.34%, real estate -2.63%, and discretionary -3.55%.

Southbound Connect volumes were moderate/light as Mainland investors were net buyers of Hong Kong stocks. Volume leader Meituan Dianping was sold 3 to 2, Tencent was bought 2 to 1, and Semiconductor Manufacturing was bought 3 to 1. Mainland investors bought $290mm worth of Hong Kong stocks today as Southbound Connect accounted for 6.6% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen hung in there until an end of day bout of selling caused both indexes to close -1.02% and -0.29%, respectively, at 2,890 and 1,865, respectively. Volume picked up +8.7% from Friday while breadth tilted negative with 1,486 advancers and 2,168 decliners. Large caps underperformed mid and small caps by 50bps. The Mainland stocks within the MSCI China All Shares Index -1.28% with healthcare +0.37%, communication -0.03%, real estate -0.97%, industrials -1.4%, staples -1.41%, financials -1.42%, materials -1.59%, utilities -1.67%, energy -1.75%, discretionary -1.86%, and tech -1.9%.

Northbound Connect volumes were moderate as Shanghai had foreign selling while Shenzhen had foreign buying. Liquor stocks were the volume leaders and were weaker as both Kweichow Moutai and Wuliangye Yibin saw selling as foreign investors sour on China’s favorite drink. Foreign investors sold $573mm worth of Mainland stocks today. Northbound Connect accounted for 5.5% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.10 versus 7.09 Friday

- CNY/EUR 7.98 versus 7.07 Friday

- Yield on 1-Day Government Bond 1.15% versus 1.20% Friday

- Yield on 10-Year Government Bond 2.79% versus 2.75% Friday

- Yield on 10-Year China Development Bank Bond 3.12% versus 3.09% Friday