If Chinese Equities Rally In a Forest and No One Is Invested, Who Makes the Money? Week In Review

3 Min. Read Time

Week In Review

- Online retail sales in China grew +4.5% in May, according to data released Monday. We also learned that NetEase’s Hong Kong listing will be added to the Hang Seng Composite Index on Friday, June 26th. Passive managers may increases purchases of the stock before its inclusion in the index.

- There were rumors on Tuesday that Tencent is eyeing a purchase of Baidu’s stake in video streamer and Baidu spin-off iQiyi (IQ US).

- JD.com’s Hong Kong listing was 179x oversubscribed on Wednesday, demonstrating a significant demand for the company’s shares. Meanwhile, Asian markets showed resilience to risk sentiment surrounding the coronavirus flare-up in Beijing.

- JD.com listed for the first time in Hong Kong. The IPO was a great success as the company raised $3.9 billion and shares rose +3.52% in Thursday trading.

Friday’s Key News

Asia markets ended the week on a high note as Secretary of State Pompeo’s positive comments on China pledging to meet their Phase One obligations lifted equities. This outweighed President Trump’s WSJ interview and subsequent Tweet that the US could decouple from China. In finance, we are very data driven which makes such statements quite head scratching. Decoupling would mean losing our largest trade partner, $370B of revenues generated by US companies in China, and a key source of revenue for 46% of the top 3,000 US stocks, and so on and so forth.

Today was the FTSE index rebalance. Alibaba Health jumped +7.56% as it was added to FTSE indices. FTSE rebalance trades led to volumes jumping +24% from yesterday in Hong Kong while Northbound Connect saw very high volumes and inflows as foreign investors bought $2.879 billion worth of Mainland stocks today. Mainland stocks and Chinese companies listed in Hong Kong saw their percent weights increase in FTSE indices across the board.

Growth names were the volume leaders in Friday trading with Tencent +0.52%, Alibaba HK +0.55%, Hong Kong Exchanges +1.49%, and Meituan Dianping +0.87%. JD HK and NetEase HK diverged to close -0.17% and +1.66%, respectively. Mainland markets were led by D&D. Not Dunkin’ Donuts, but Drinking & Drugs i.e. Alcohol and healthcare stocks. Tip of the hat to SCMP for the acronym! All in all, China and Hong Kong had a very strong week on both a relative and an absolute basis.

MSCI updated JD.com’s market cap weight in their indices at yesterday’s close due to the company’s new Hong Kong listing. The US-listed JD received the share adjustment as it is the primary trading venue for the company. Passive managers of MSCI-benchmarked ETFs and index funds had to buy the stock as a result. At the close yesterday, there was a print of 8.6mm shares worth while the stock traded 40mm shares. On Wednesday, the stock traded 24mm shares while the 1-year average is 14mm shares. The power of passive was on full display!

H-Share Update

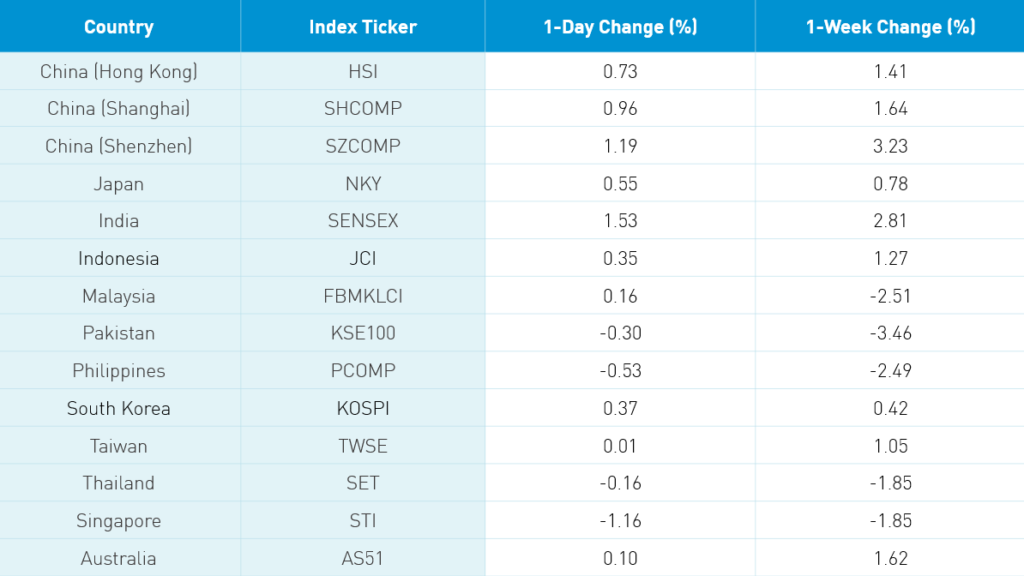

The Hang Seng traveled from lower left to upper right +0.73%/+178 index points to close at 24,643 as volumes surged +24% from yesterday, which is 50% higher than the 1-year average. Breadth was positive with 36 advancers and 10 decliners as index heavyweights led the way higher with China Construction Bank gaining +1.46%/+29 index points, Hong Kong Exchanges +1.49%/+16 index points and ICBC +1.37%/+15 index points. Today’s best performer was AAC +6.54%/+6 index points while Sunny Optical -1.135/-2 index points. Hong Kong-domiciled stocks outperformed China-domiciled stocks +1.02% versus +0.59% using the HS HK 35 and China Enterprise Indices as proxies. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.77% with Healthcare 1.65%, real estate +1.38%, staples +1.01%, discretionary +0.95%, financials +0.87%, tech +0.53%, communication +0.53%, energy +0.5%, industrials +0.43%, utilities +0.12%, and materials -0.47%.

Southbound Connect volumes were average/moderate as Mainland investors were net buyers of Hong Kong stocks. Volume leaders saw pronounced buying as Tencent, Seminconductor Manufacturing, ZTE and China Construction Bank all saw heavy buying relative to sellers. Mainland investors bought $273mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 6.6% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen had a strong day +0.96% and +1.19% to close at 2,967 and 1,931, respectively, as volume picked up 2%. Breadth was positive with 2,091 advancers and 1,457 decliners as small caps outperformed large and mid caps. The Mainland stocks within the MSCI China All Shares Index gained +1.56% with healthcare +2.93%, staples +2.56%, discretionary +1.63%, financials +1.49%, tech +1.19%, industrials +1.14%, communication +0.69%, real estate +0.67%, materials +0.48%, energy +0.24%, and utilities +0.09%.

Northbound Connect inflows were very strong on high volumes. Volume leaders Kweichow Moutai, Ping An Insurance, and Wuliangye Yibin all had buyers outpace sellers. Foreign investors bought $2.578 billion worth of Mainland stocks today, bringing the weekly total to $2.879B.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.07 versus 7.09 yesterday

- CNY/EUR 7.90 versus 7.96 yesterday

- Yield on 1-Day Government Bond 1.43% versus 1.42% yesterday

- Yield on 10-Year Government Bond 2.88% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.16% versus 3.15% yesterday