Mainland Marches On, Profit-Taking in Hong Kong

5 Min. Read Time

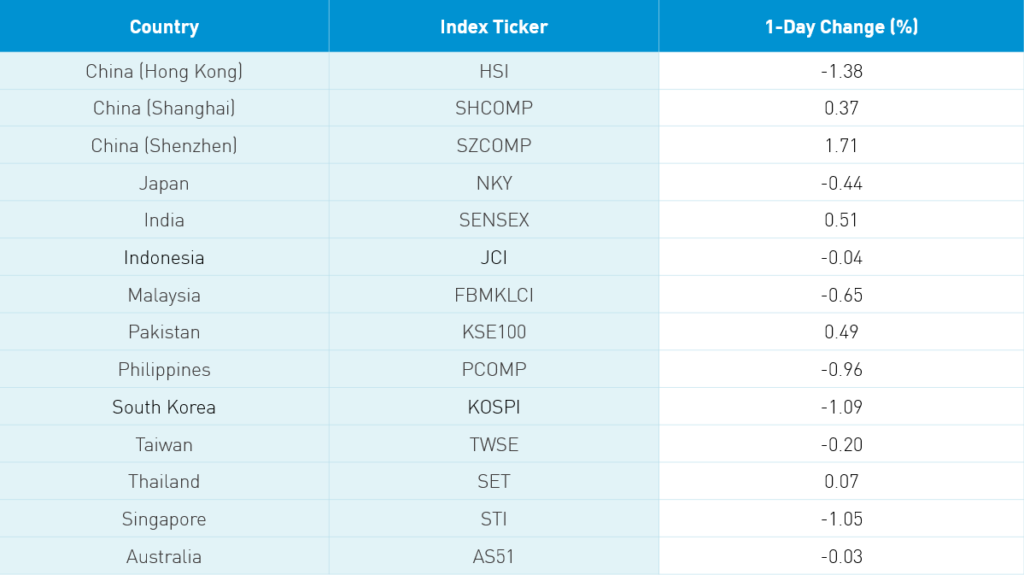

Key News

Asian investors took profits overnight after yesterday’s massive move. Hong Kong opened higher but retreated later in the session amid Hong Kong chief executive Carrie Lam’s speech defending the new security law and several new cases of coronavirus. Mainland investors were strong buyers of Hong Kong stocks on the weakness in the 17th consecutive day of net purchasing. Volume leader Semiconductor Manufacturing slipped -8.85% after surging 20% yesterday in advance of its STAR Board IPO tomorrow. Tencent was off -0.77% as CEO Pony Ma sold 500k shares, Alibaba HK popped +3.11%, Ping An Insurance +1.28%, and Meituan Dianping -3.14%.

Mainland China gained though investors favored growth companies. Shenzhen rose +1.17% while Shanghai gave up some gains and slid from the morning’s high to close +0.37% on very strong volumes that were +10% higher than yesterday. DnD, drugs and drinks, had a strong day with Kweichow Moutai +5.5%. Financials were led lower by brokerages after the widely followed Security Times said investors should be “rational”. Real estate also succumbed to profit taking after yesterday’s monster move on reports that one province would curtail home purchases. We’ll see whether value rebound over the last several days will resume. Northbound Connect volumes were the strongest in recent memory as foreign investors bought $1.402B worth of Mainland stocks, bringing the four-day total to $7.636B.

One stat from yesterday’s note was that, according to CICC, only 2% of China’s household wealth is invested in stocks. Expanding on this though, only 2% of household wealth is invested in mutual funds versus 66% in real estate. For comparative purposes, 26% of US household wealth is in real estate, 6% in mutual funds, and 23% in stocks.

Already, the nattering nabobs of negativity are comparing China’s 2014/2015 equity rise and collapse to today. As one broker noted, overnight margin debt is now only 2% of market cap versus 4.5% in 2015 and the latter figure does not include significant amounts of off-balance sheet lending which stoked the rise. Regulators have tightened margin requirements since then, eliminating the off-balance sheet lenders. Shanghai’s P/E ratio is currently 19 versus a peak of 41. Shenzhen’s P/E ratio is higher at 52 as investors have begun to bid up growth companies versus value companies. It is clear that retail investors have become interested in the Mainland market based on the huge volumes we’ve seen of late. Several technical analysts have noted the strong breakout though we are apt to see pullback at some point, which is healthy.

E-commerce company Pinduoduo (PDD US) was a standout for its weakness yesterday in a sea of green. Chatter is the company is guiding sell side analysts’ Q2 estimates down. With that said the stock has performed incredibly well this year.

As I read this weekend’s Investors’ Business Daily, I could not help but notice the soybean and soybean meal futures charts. This follows last week’s observation on copper’s rise. I also noticed IBD’s highlight of YTD best performing International ETFs included among the top 10 three from an unnamed US-based China asset manager. Apologies for the ADD and now back to soybean’s price action. What could be driving the prices higher? Starts with a C and ends in A. No, not Canada despite my respect for our neighbor and home to the great city of Toronto (Vancouver too!). Maybe China is buying more soybeans than the constant barrage of negative China headlines would let on? The USDA provides a tremendous amount of data transparency though I’m a novice at navigating their website and understanding their terminology. I did find the following line concerning soybeans “For 2020/2021, net sales of 841,700 MT were primarily for China (594,000 MT)”. I assume MT stands for metric tons. June’s soybean purchases will be released on Thursday, giving me two days to get up to speed and speak to a friend who plies his wares in the commodity space. As I consider US exports, one issue for US soybean farmers has been Brazil’s weak currency, which makes their soybeans less expensive. A weak dollar would help US farmers.

My colleague Anthony reminded me that China’s Gaokao test is being held this week. According to a Mainland media source, 10.7mm students started China’s version of the SAT, the National College Entrance Examination, at 7,000 testing centers. The two-day test is grueling and pressure filled as high school students must name the colleges they want to apply to. Test scores are ranked with the top students going to the top schools and so on. If your test scores fail to match your desired schools, you can end up not going to college at all. However, there is always the option to retake the test the following year. Good luck!

H-Share Update

The Hang Seng opened higher, but gravity quickly took effect and the index closed -1.38%/-363 index points at 25,975. Volumes were off -4% from yesterday but still very high as they were 2.5X the 1-year average. Breadth swung south with only 8 advancers and 42 decliners led by today’s worst performer Bank of China -8.235/-57 index points, HSBC -1.65%/-39 index points, and China Mobile -2.67%/-28 index points. Today’s best performer was Geely Auto +3.29%/+9.9 index points. China-domiciled stocks were -1.19% versus -1.91% for Hong Kong-domiciled stocks using the HS China Enterprise and HK 35 indices as proxies. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index -1.16% with health care +0.12%, staples +0.11%, industrials -0.31%, utilities -0.35%, financials -0.77%, communication -1.06%, discretionary -1.18%, materials -1.31%, energy-2.52%, real estate -2.82%, and tech -3.42%.

Southbound Connect volumes were very high at 3X the 1-year average as Mainland investors were net buyers of Hong Kong stocks. Volume leader Semiconductor Manufacturing had the highest volume I can recall with sellers just outpacing buyers. Tencent was sold slightly while Xiaomi was bought. Mainland investors bought $531mm worth of Hong Kong stocks today as Southbound Connect trading accounted for more than 12% of HK turnover.

A-Share Update

Shanghai and Shenzhen opened higher and stayed there as Shenzhen managed to climb higher while Shanghai stayed flat. Shanghai and Shenzhen gained +0.37% and +1.71% to close at 3,345 and 2,157, respectively. Volume actually increased +10.8% from yesterday at more than 2.5X the 1-year average. Mid and small caps significantly outperformed large caps. The Mainland stocks within the MSCI China All Shares Index gained +1.24% with staples +3.31%, health care +2.62%, tech +2.31%, communication +2%, industrials +1.96%, materials +1.08%, discretionary +0.7%, energy +0.03%, utilities -0.16%, financials -1.03%, and real estate -1.4%.

Northbound Connect volumes were the highest I’ve ever with Shanghai Connect volumes at 3X the 1-year average and Shenzhen a little more than 2X. Foreign investors were net buyers of Mainland stocks with Shanghai seeing more pronounced buying than Shenzhen. Shanghai’s volume leader was Ping An Insurance, which was bought 4 to 1 and Kweichow Moutai, which had buyers just outpace sellers. Shenzhen volume leader was Gree Electric Appliances, which saw buyers outpace sellers by fair amount while liquor stock Wuliangye Yibin was sold slightly and BOE Technology was bought more than 2 to 1. Foreign investors bought $1.402 billion worth of Mainland stocks today as Northbound Connect turnover accounted for 6% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.01 versus 7.02 yesterday

- CNY/EUR 7.92 versus 7.94 yesterday

- Yield on 1-Day Government Bond 1.22% versus 1.00% yesterday

- Yield on 10-Year Government Bond 3.02% versus 3.00% yesterday

- Yield on 10-Year China Development Bank Bond 3.33% versus 3.29% yesterday