Ray Dalio Warns Against Imposing Capital Controls in The US

4 Min. Read Time

Key News

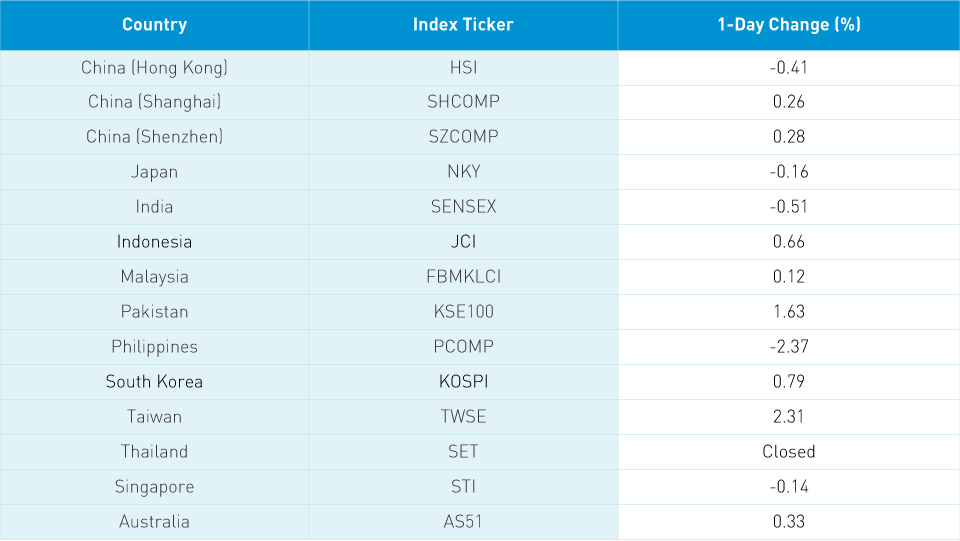

Asian equities had a mixed day as US-China political rhetoric continues to hang on sentiment while spikes in coronavirus cases gave investors additional pause. Hong Kong opened higher but slid over the course of the trading day on light volumes as stricter social distancing measures are implemented to snuff out the recent coronavirus flare up. Hong Kong volume leaders were the galloping growth names Tencent, which fell -1.52%, Alibaba HK 0.0%, Meituan Dianping -2.99%, and Semiconductor Manufacturing (SMIC) -3.12%. Meanwhile, JD.com HK rose +0.85% and NetEase HK fell -0.93%. Materials names were powered higher by gold stocks as the shiny metal reaches fresh highs.

HSBC was off -1.81% after a column in the People's Daily accused the company of framing Huawei CFO Meng Wangzhou. There is the space between a rock and hard place and then there is where HSBC appears to be.

Mainland Chinese stocks managed small gains on light volume as June Industrials Profits rose +11.5% year over year versus May's increase of 6%. The positive release, however, failed to excite investors.

Outperforming sectors included gold stocks and the DND trade (drugs/pharma and drinks/alcohol) while real estate was off as policy makers want to temper enthusiasm for speculation in the housing market. Foreign investors used the dip in growth sectors to buy via Shenzhen Northbound Stock Connect, the Hong Kong-based platform allowing access to Mainland-listed stocks, as Shanghai Connect saw net selling. The National Equities Exchange and Quotation (NEEQ), China's version of the pink sheets, carved out 32 larger companies for a new board that Mainland mutual funds are now allowed to invest in. These are tiny companies that are not included in MSCI's definition of Mainland stocks. However, the move is representative of continuing financial reforms.

Ray Dalio's Sunday interview on Fox News garnered a fair amount of interest from our brokers as well as local media. My takeaway was that Mr. Dalio was warning US politicians about implementing capital controls in the US as a form of retaliation against China. He was more concerned about US budget deficits and rising debt levels than China. It does amaze me how much attention China is receiving despite domestic issues. The US dollar's recent decline is driven by low US interest rates in addition to a deteriorating US balance sheet. It could lead to a capital flow adjustment as foreign investors' positions are losing value.

I was surprised he seems to accept there is US China rivalry as it ignores the economic reality of US and China business interests. Need I mention the billions of revenue generated in China by US multinationals? Reuters reported overnight that China imported the largest amount of US-manufactured copper concentrate in June since September 2018. Closing consulates diminishes communication between the US and China, which is the opposite of what we need. Last week, a group of US diplomats travelled to China, likely in advance of agreed upon six month US China Phase 1 deal catch ups. Fingers crossed that was the case.

Several Chinese A-Shares-focused levered and inverse ETFs listed in Hong Kong today for the first time. It is an interesting move and could pave the way for MSCI China A Index futures to list in Hong Kong. That would remove one of MSCI's outstanding issues for raising the weight of Chinese A-Shares in their indices.

H-Share Update

The Hang Seng opened higher but slid lower to close -0.41%/-102 index points at 24,603. Volumes collapsed -24%, which is just above the 1-year average while breadth was off with 19 advancers and 29 decliners. Index heavyweights led the way with Tencent -1.52%/-43 index points, HSBC -1.81%/-39 index points and HK Exchanges -1.83%/-23 index points. Sunny Optical was the day's best performer +2.61%/7.9 index points while New World Development was the worst -2.82%/-4 index points. China-domiciled companies outperformed Hong Kong-domiciled companies -0.05% versus -0.8% using the HS China Enterprise and HK 35 indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -0.67% with materials +3.41%, staples +0.97%, energy +0.23%, financials +0.15%, utilities +0.13%, industrials -0.23%, health care -0.61%, real estate -1.14%, communication -1.43%, discretionary -1.49%, and tech -1.53%.

Southbound Stock Connect flows were light as Mainland investors' pace of buying slowed markedly. The Shanghai Southbound Connect volume leaders SMIC and Tencent saw sellers outpace buyers by a small margin while Xiaomi was bought by a small amount. Meituan Dianping was sold 2 to 1 while over on the Shenzhen Southbound e-cigarette maker Smoore International had massive buying of 40 to 1. Mainland investors bought $238mm worth of Hong Kong stocks today as Southbound Stock Connect trading accounted for 10% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen traded in a narrow range gaining +0.26% and +0.28% to close at 3,205 and 2,144, respectively. Volumes collapsed -30% to just above the 1-year average while breadth was off with 1,601 advancers and 2,030 decliners. Mid and small caps outperformed large caps by a small amount. The 509 Mainland-listed companies within the MSCI China All Shares Index rose +0.65% with health care +2.04%, materials +1.87%, staples +1.54%, utilities +1.37%, tech +1.17%, communication +0.48%, energy +0.17%, financials -0.23%, discretionary -0.4%, industrials -0.51%, and real estate -1.55%.

Northbound Stock Connect volumes were elevated in what has become the new normal as foreign investors sold Shanghai stocks and bought Shenzhen stocks. Shanghai volume leader Ping An was bought by a small amount while China Tourism was sold by 2 to 1 and Kweichow Moutai was flat as trading was balanced between buyers and sellers. Foreign investors sold -$216mm worth of Mainland stocks today as Northbound Stock Connect trading accounted for 5% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 7.01 versus 7.02 Friday

- CNY/EUR 8.22 versus 8.17 Friday

- Yield on 1-Day Government Bond 1.33% versus 1.33% Friday

- Yield on 10-Year Government Bond 2.88% versus 2.86% Friday

- Yield on 10-Year China Development Bank Bond 3.35% versus 3.33% Friday