ATMX Hit on Global Tech Rout

3 Min. Read Time

We have two webinars coming up in September. You can find the descriptions below.

EM Consumer Technology: Tuesday, September 15th, 11 am EST

COVID-19: An Inflection Point For Emerging Markets Consumer Technology

China Macro: Thursday, September 17th, 9 am EST

China Macro Economic Outlook: Digital Transformation and Structural Reforms Provide Catalysts for Post COVID-19 Growth

Key News

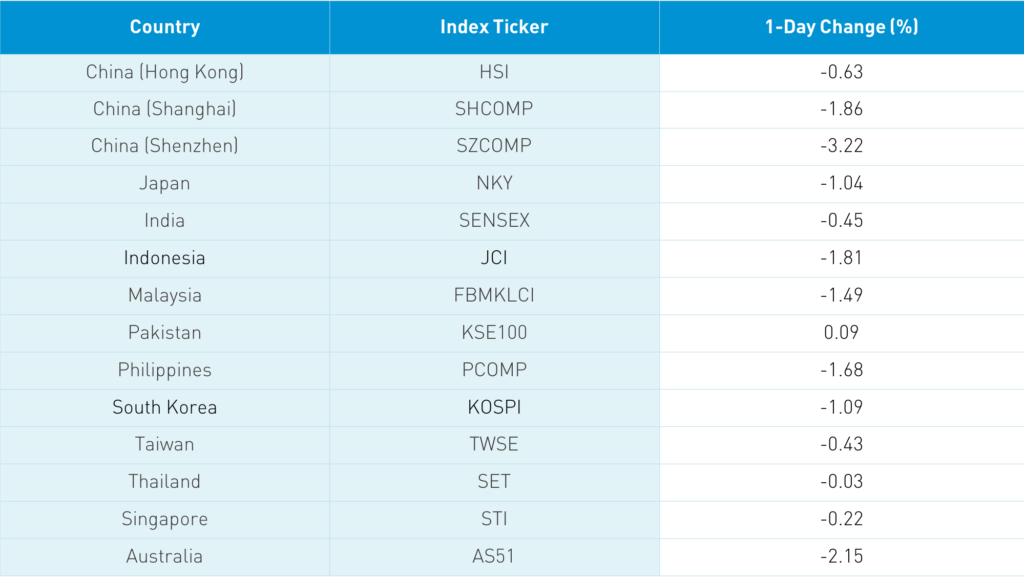

Asian equities followed the US equity market south as the three-day tech rout goes global and Astra Zenca’s vaccine issue hit healthcare. Hong Kong growth stocks were hit as ATMX led the volume list with Alibaba Hong Kong off -2.37%, Tencent off -0.88%, Meituan Dianping off -2.52%, Xiaomi off -1.34%, and Semiconductor Manufacturing off -2.02%. Mainland China was off for the same reasons while tech was especially weak after three small-cap companies were halted due to enormous percentage gains.

The markets did overlook strong August auto sales, which were up +8.8% year-over-year. Shanghai and Shenzhen have fallen to the bottom of their recent price ranges. Considering the strength of the economic data, we should hopefully see investors buy the dip at this level. The Hang Seng Index is also at the low end of its July/August price range. Remember that the index added Alibaba Hong Kong, Meituan Dianping, and Xiaomi on Monday, which lowered financials to 45% of the index.

Chinese bonds rallied overnight while the US dollar had a rally that I expect to be short-lived. What could put a floor under growth stocks? Apple is expected to announce its new iPhone next Tuesday, which would have a big effect on its Asian suppliers. With ample liquidity and low-interest rates globally, where else are investors going to put cash to work?

Tencent will no longer distribute the popular video game PlayerUnknown’s Battlegrounds (PUBG) in India. Instead, the South Korean gaming company that developed PUBG will distribute it, potentially a workaround on the recent Chinese app ban in India.

58.com (WUBA US) announced on Monday that it's being taken private by management and private equity firms Warburg Pincus and General Atlantic. The company is often referred to as the Craiglist of China. The company increased revenue by 50% from 2017 to 2019, while EPS doubled. However, WUBA’s stock price was down approximately -11% over the same time period since 12/31/2017. I doubt this is the last we hear of 58.com, as a relisting in Hong Kong and/or Mainland China is highly likely in the future.

Most overlooked headline from yesterday: China pre-orders 400,000 tons of US soybeans for next season. The American Chamber of Commerce in Shanghai surveyed 346 US companies with operations in China. According to the Financial Times, less than 4% of the companies plan on relocating production back to the US. Why would you shut yourself out of a market with 1.4 billion potential consumers? China is also a gateway to Asia with 4 billion potential customers.

Yum China’s Hong Kong listing is tomorrow, after being oversubscribed 50X according to brokers.

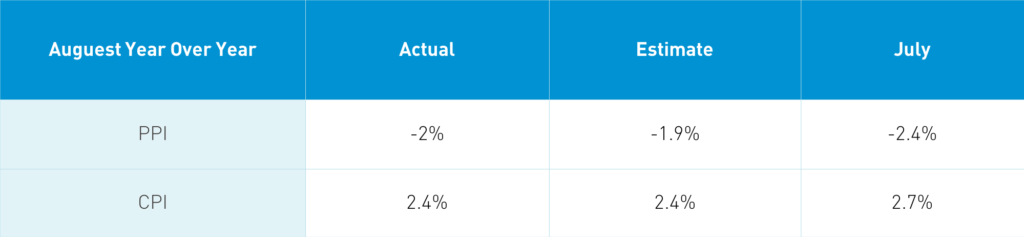

The morning release of inflation measures had little impact on the market.

PPI’s weakness was driven by lower commodity prices, while CPI, less food and energy, was flat. Food prices were up +11.2% year-over-year driven by high pork prices, though down month-over-month. Central banks worry about inflation (at least they are supposed to!) as it erodes wealth. With little signs of inflation, the PBOC has ample room to cut interest rates.

H-Share Update

The Hang Seng Index was off -0.63%/-155 index points to close at 24,468 as volume declined -14%, which is just above the 1-year average. Breadth was off with 15 advancers and 33 decliners. The broader Hang Seng Composite was off -0.88% with 118 advancers and 336 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index declined by -1.07%, led by industrials -0.36%, utilities -0.47%, and communication -0.68%, and underperformers materials -3.15%, discretionary -1.94%, and staples -1.93%. Southbound Stock Connect volumes were light with Mainland investors buyers of Hong Kong stocks. Mainland investors bought $223mm of Hong Kong stocks as Southbound Connect trading accounted for nearly 10% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen were down -1.86% and -3.22% to close at 3,254 and 2,175 respectively, as volume increased +12%, which is 42% above the 1-year average. Breadth was well off with 1,058 advancers and 2,637 decliners as mid and small caps underperformed. The 517 Mainland stocks within the MSCI China All Shares Index were off -2.68%, led by utilities -0.47%, energy -1.04%, and financials -1.44%, and underperformers health care -4.93%, communication -3.7%, and tech -3.59%. Foreign investors were sellers of Mainland stocks

Last Night’s Exchange Rates & Yields

- CNY/USD 6.83 versus 6.85 yesterday

- CNY/EUR 8.08 versus 8.07 yesterday

- Yield on 1-Day Government Bond 1.00% versus 0.95% yesterday

- Yield on 10-Year Government Bond 3.08% versus 3.12% yesterday

- Yield on 10-Year China Development Bank Bond 3.67% versus 3.63% yesterday