Lufax Holdings Looks to Capitalize on Ant Group’s Fintech Interest with an NYSE listing

3 Min. Read Time

Key News

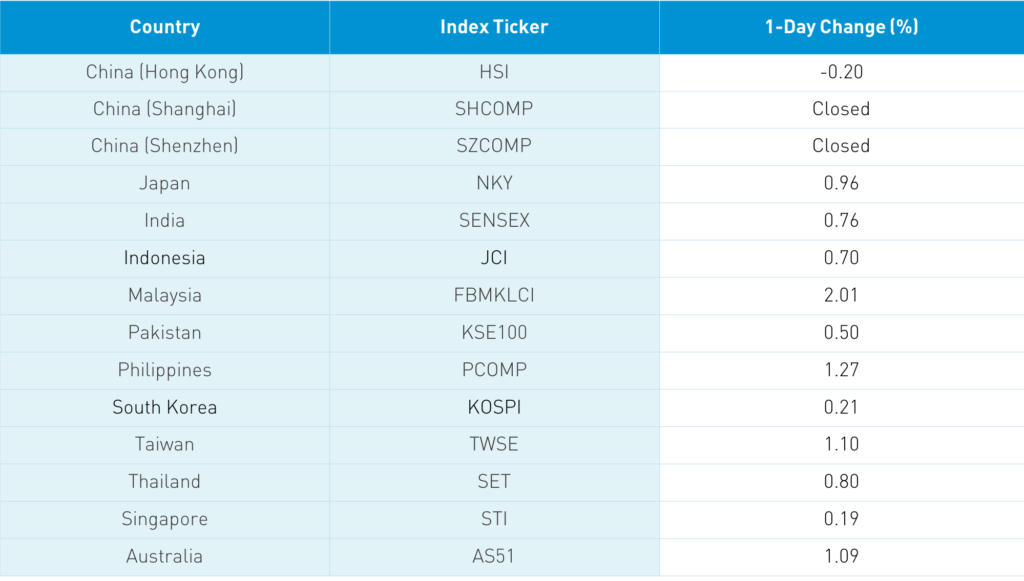

Asian equities were largely higher on light volumes, though the 50 stock Hang Seng Index was off a touch/-0.2% after rising off its intra-day low of -0.9%. The broader Hang Seng Composite gained +0.3% and the 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.35%. Volumes have been anemic during the Chinese holiday, though things should pick up tomorrow as Shanghai & Shenzhen come back online. US-listed Chinese A-share ETFs are anticipating a healthy +3% open for the Mainland market tonight.

There was another quiet night in Hong Kong as the US focuses on the election and stimulus. Hong Kong volume leaders were Alibaba Hong Kong, which gained +0.49%, Tencent, which was unchanged, Xiaomi, which fell -3.92%, Meituan Dianping, which fell -0.37%, BYD, which rose +5.94%, Sunny Optical, which rose +2.87% on the coming Apple release, Ping An Insurance, which gained +0.38% after Lufax Holdings, backed by Ping An Insurance, filed for a US listing, and JD.com Hong Kong, which was off a James Bond -0.07%. Macau gaming stocks were off as the Golden Week was less than Golden, based on weak visitor data due to coronavirus travel restrictions. Things should pick up tonight with Stock Connect, Shanghai, and Shenzhen reopening, though I predict volumes will really pick up next week.

Mid-day yesterday, we had the announcement that the US would target Chinese mobile payment providers Ant Group and Tencent’s WePay, despite the reality that neither company has any users in the US. In order to use the apps, one needs a Chinese bank account. Though an absolutely meaningless announcement, US-listed Chinese companies dropped on the “news”. Remember when we get US political rhetoric that we need to check on CNH, China’s currency price during US trading hours. CNH did initially spike up and depreciate $0.01, though it quickly recovered. US Chinese equities also recovered. The key takeaway is not to panic on such headlines. Checking on CNH’s price action is a great indicator of whether the bark has any bite. As one of the institutional brokers put it “USDCNH no care, so neither should you”.

Headlines always provide a good reason not to invest in China. Today it’s the US-China political rhetoric, and a few years ago, it was shadow banking. Banks were reluctant to lend to private companies, and thus peer to peer lending filled the void. Investors earned a lending yield by having their assets pooled and lent to firms and individuals. The industry took off until 2016 when regulators recognized the potential risks associated with the practice. As regulators put the screws to the space, public companies in the space such as tickers QD and YRD fell dramatically. Lufax Holdings is a peer to peer lender that evolved out of necessity into a “technology-empowered personal financial services platform”. The Ping An Insurance-backed company filed for a New York Stock Exchange listing under the ticker LU. In scanning their SEC filing, the company has two main businesses: Retail Credit Facilitation, which lends 13.4mm to small business owners with RMB 519 billion in loans currently, and Wealth Management, which has 12.8mm investors with RMB 375B in investable assets. The company reported Net Profit of RMB 13.3B ($1.9B) in 2019 and RMB 7.3B ($1B) in the first half of 2020. The filing didn’t disclose the size of the offering, though chatter is that at least $2B will be raised.

An institutional broker noted a large out-of-the-money Alibaba US call option trade yesterday. Of course, we immediately thought of Softbank, which put on monster tech option trades earlier this year. We’ll never know who bought Alibaba June calls at $440, but they are confident about Alibaba rising…a lot.

Caixin PMI Services to be released tonight.

H-Share Update

The Hang Seng Index eased in the morning to reach an intra-day low of -0.9% before rallying back to close -0.2%/49 index points at 24,193. Volumes off by -4% with 19 advancers and 28 decliners. The broader Hang Seng Composite gained +0.3% with 303 advancers and 148 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.35%, led by industrials +1.49%, materials +1.01%, and discretionary +0.76%, while energy -0.78%, staples -0.08%. Southbound Connect was closed.

A-Share Update

Shanghai and Shenzhen are closed until Friday for the Golden Week holiday.