The Nattering Nabobs of Negativity Weigh on Markets

4 Min. Read Time

Key News

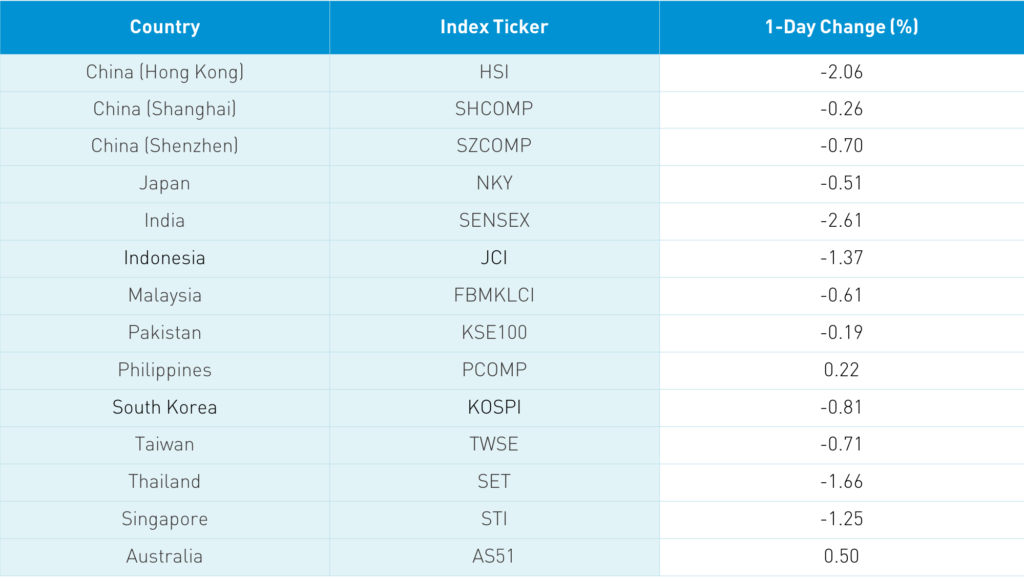

Asian equities were weaker today as US stimulus hopes fade, Europe tightens social distancing measures on coronavirus flare ups, and Reuters reports that Ant Group could be added to the US’ Entity List. Markets didn’t check my political rhetoric gauge as China currency appreciated $0.02 versus the US dollar yesterday. Being added to the Entity List would be of little consequence to Ant Group as the company has no business in the United States. It is worth highlighting that Taiwan Semiconductor (2330 TT) reported strong earnings after the market’s close. TSMC is a significant constituent of many broad Emerging Markets indexes and is therefore widely held and tends to serve as a bellwether for the sector.

Hong Kong’s selloff was led by the same growth stocks that performed so well yesterday. Volume leaders were Tencent, which fell -3.75%, Alibaba HK, which fell -4.3%, Meituan Dianping, which fell -4.81%, Xiaomi, which fell -3.44%, Ping An Insurance, which was unchanged, and BYD, which fell -0.15%. One bright spot was windmill manufacturer Xinjiang Goldwind (2208 HK), which gained +11% as clean energy names are garnering more attention due to the sector being highlighted in the next Five Year Plan crafted at month end.

The Mainland market was off, but by less than half as much as Hong Kong. Remember that Hong Kong is foreign investors’ traditional definition of China while the Mainland market is predominantly held by Chinese investors. The PBOC injected RMB 500 billion into the financial system today and left the medium-term lending facility (MLF) rate unchanged at 2.95%, as expected. Markets thrive on liquidity, so the injection helped contain losses. Mainland financials gained +0.88% on the policy move. Shanghai and Shenzhen are consolidating as they been in their current range since July. I suspect 2nd half earnings may serve as the catalyst to get them to punch through resistance. Only time will tell.

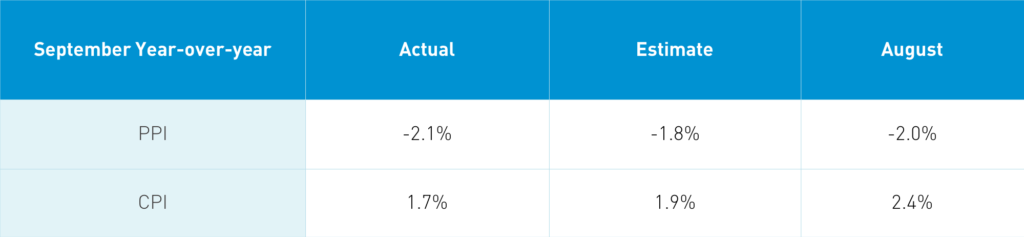

China reported inflation data for September overnight:

Takeaway: The inflation data came in weaker than expected, which didn’t drive the market today though it didn’t help as yesterday’s strong credit data was quickly forgotten. PPI’s decline is an indication that demand is weak, once again highlighting that China is not immune to the economic consequences of global quarantines. Consumer prices were driven by falling food prices, which rose +7.9% in September versus 11.2% in August. Pork prices skyrocketed after China wiped out its hogs due to the African swine flu last year. While transportation and communication prices were down -3.6%, prices for medicine and healthcare gained +1.5%.

A Mainland financial news source had an interesting article on declining ATM usage in China post-quarantine. Ant Group’s IPO highlights the incredible level of mobile payment usage in China today: $49 trillion annually with Ant’s Alipay controlling 55% of market share and Tencent’s WeChat Pay controlling 38%. The article noted that 40,000 ATMs were taken offline in the first six months of the year as consumers prefer mobile payments over cash for safety reasons. The article noted that a publicly traded Chinese ATM manufacturer reported losses this year. It might also be worth one’s time to figure out who the big ATM manufacturers are globally.

I caught up with a research contact yesterday who noted that Ant Group’s IPO has overshadowed JD Health’s coming Hong Kong listing. I would agree as the company hasn’t garnered much attention. However, the Hong Kong shares of competitors Ali Health and Ping An Health & Technology have been investor favorites this year. I will track down the filing and provide further clarity.

$6 billion worth of Chinese Treasury bonds were sold to foreign investors attracted by China’s strong comparative yields and good sovereign credit rating. A 10-Year Chinese Treasury bond yields 3.2% versus 0.7% for the current 10-year US Treasury bond. Bloomberg Research had a great piece on how Hong Kong real estate firms with Mainland revenue exposure are poised to benefit from the renminbi’s appreciation versus the US dollar. I believe the Chinese bonds are attractive as China’s V-shaped recovery should allow bond issuers to make coupon and principal payments. Combine that with the reward-free risk of US bonds and I would think that interest will continue. Allocating a small percentage of FI to China makes sense to me.

H-Share Update

The Hang Seng opened lower and stayed there to close -2.06%/-508 index points at 24,158. Volume was off 15% from yesterday though above the 1-year average. Breadth was awful with 1 advancer and 48 decliners. The broader Hang Seng Composite was off -2.06% wit 88 advancers and 370 decliners. The 204 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -2.2%, led lower by communication -3.5%, discretionary -3.07%, tech -3.01%, health care -2.35, utilities -1.67%, and real estate -1.4%. Southbound Connect volumes were light as Mainland investors bought $488 million worth of Hong Kong stocks today. Southbound Connect trading accounted for 10.2% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen were off -0.26% and -0.7% to close at 3,332 and 2,274, respectively. Volume was off -8% from yesterday, which is back below the 1-year average while breadth was off with 1,199 advancers and 2,482 decliners. The 517 Mainland stocks within the MSCI China All Shares Index were off -0.24% with financials +0.88%, and energy +0.85%. Meanwhile, communication -1.07%, health care -0.96%, staples -0.56%, and materials -0.51%. Northbound Stock Connect volumes were moderate as foreign investors sold -$49 million worth of Mainland stocks as Northbound Connect accounted for 5.4% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.73 versus 6.72 yesterday

- CNY/EUR 7.87 versus 7.90 yesterday

- Yield on 10-Year Government Bond 3.23% versus 3.22% yesterday

- Yield on 10-Year China Development Bank Bond 3.78% versus 3.77% yesterday