Investors Get Their Cheese As Year of The Rat Ends

4 Min. Read Time

Key News

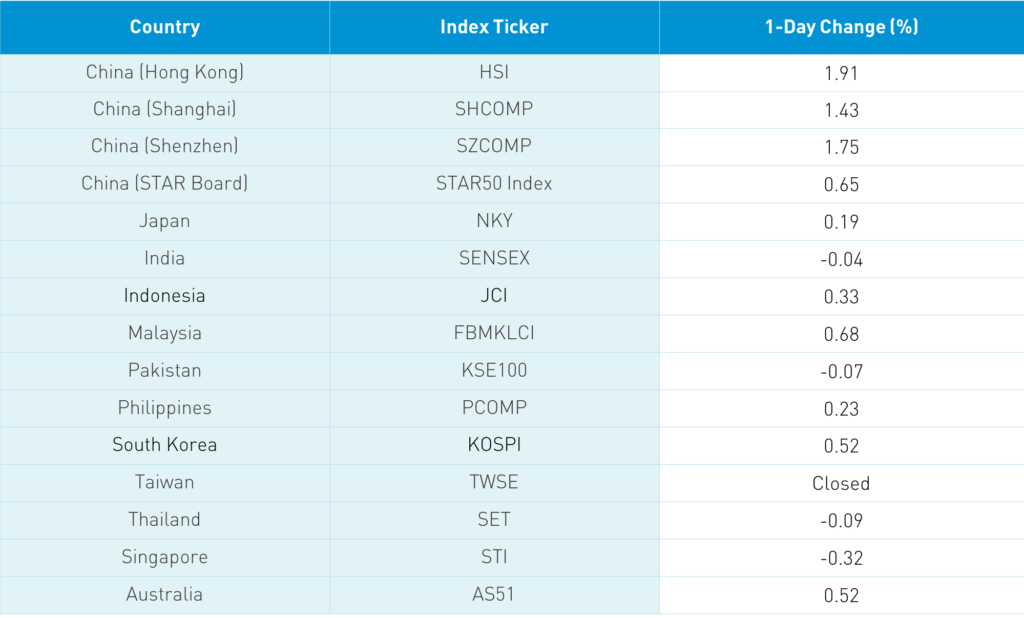

Asian equities were largely higher as Hong Kong and Mainland China outperformed on the last day of Mainland trading before the Chinese New Year holiday. Yesterday’s strong new loan and aggregate financing data release was cited as a catalyst. There has been so much hardship and pain in the last year globally that it is hard to rectify how well global equities have done. This holds true for Chinese equity investors as well as the year of the rat ends.

The Hang Seng Index closed +1.91% higher at 30,038 led by galloping growth stocks. It was a broad rally as the Chinese stocks listed in Hong Kong and within the MSCI China All Shares Index gained +2.13%. Hong Kong volume leaders were Tencent, which gained +2.77% as investors cheered new game approvals, Kuaishou Technology, which surged +13.23% as the company will be added MSCI indexes at month end, Meituan, which gained +5.23%, Alibaba HK, which gained +2.58%, Xiaomi, which gained +0.55%, HK Exchanges, which gained +3.79%, Ping An, which gained +0.39%, BYD, which gained +2.69%, JD.com HK, which gained +2.69%, and China Construction Bank, which gained +2.5%. Tomorrow is a half day for Hong Kong.

Healthcare did well in Hong Kong and Mainland China as CanSino Biologics (6185 HK) ripped +14.53% on news of the efficacy rate of its vaccine and Mainland reports of policy supporting traditional Chinese medicine. Shanghai, Shenzhen, and the STAR Board gained +1.43%, +1.75% and +0.65%, respectively. Consumption plays also gained as limited travel during Chinese New Year should benefit certain companies. Mainland volume leaders included alcohol stocks Kweichow Moutai, which gained +5.89% and Wuliangye Yibin, which gained +3.99%. Real estate was off as a Mainland media source noted Beijing’s local government reiterated that housing is for living and not speculating. Foreign investors sold $276 million worth of Mainland equities as Kweichow Moutai had a large net sale. Other than Kweichou Moutai, it would have been a net inflow day. Foreign investors have bought $1.36 billion worth of mainland stocks so far this week, which raises the year-to-date net inflow to $11.15 billion. CNY was off a touch while bonds eased and copper rallied.

This morning, Bloomberg is reporting that Jack Ma was spotted playing golf on China’s Hawaii: Hainan Island. I had previously joked that Mr. Ma was likely simply on vacation on Hainan Island and laying low. I was always dismissive of the “missing” Jack Ma media narrative.

The Wall Street Journal is reporting that ByteDance’s “sale” of TikTok to Oracle and Walmart driven by the previous administration is on hold. Many US pension funds, endowments, and foundations are likely exhaling as two of ByteDance’s biggest owners are US private equity firms General Atlantic and Sequoia. The article mentions Tiktok’s synergies with Walmart, with which I agree. While Walmart sells goods on TikTok today in the US, there might be a great opportunity to collaborate in China. However, Walmart has an investment in JD.com, which could complicate things. Nonetheless, ByteDance is a real tour de force in China.

Last night MSCI released the pro forma for the March 1st Quarterly Index Review. China’s weight in EM will increase to 39% from 38.7% with 14 new additions and three deletions. Numerically, China now represents 711 of the Emerging Markets Index’s 1,395 holdings. China’s weight of 39% is 2X larger than MSCI EM Europe, Middle East, Africa, and MSCI EM Latin America combined! I write daily about the MSCI China All Shares Index, which holds the full set of A-Shares, Hong Kong, and US stocks. While STAR Board stocks were not added to MSCI EM or China, I noticed Shenzhen Transsion Holding (688036 CH) was added to the MSCI China All Shares Index, which is a total China index including the full weight of Chinese A-shares. All Shares is what the MSCI China Index will look like once A-Shares are fully added, though we do not have to wait to know what the future will look like. Yesterday’s announcement also highlights why an EM ex-China strategy is so relevant today and in the future.

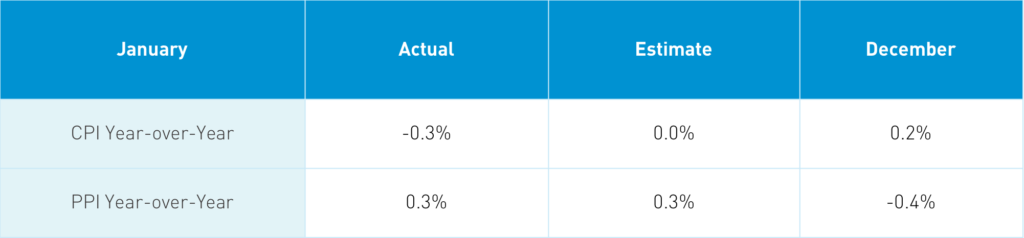

Takeaway: The release, which came at the market’s open, was not cited as a market mover. The CPI saw food prices increase by 1.4% while transportation prices plunged by -4.6%. The key is to recognize that this is a year over year comparison of pre-quarantine China embarking on travel a travel bonanza for Chinese New Year versus this year with a limited amount of travel due to coronavirus restrictions. The clickbait headlines were all about an “uneven recovery” though it is just simply the year-over-year comparison that skews this. Amazing. PPI was driven by mining prices, which gained +1%, manufacturing, which gained +1%, and food +1.6% with the former not surprising considering the tear commodities have been on.

H-Share Update

The Hang Seng grinded higher to close +1.91% higher at 30,038. Volumes increased +17% from yesterday, which is 23% above the 1-year average while breadth was fantastic with 44 advancers and 3 decliners. The 196 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +2.13% led by discretionary +3.85%, communication +2.75%, health care +2.22%, materials +1.76%, financials +1.53% and tech +1.03%. Meanwhile, industrials and energy were off -0.95% and -0.73%, respectively. Southbound Stock Connect was closed overnight.

A-Share Update

Shanghai and Shenzhen rose higher by +1.43% and +1.75% to close at 3,655 and 2,460, respectively. Volume increased +4.6% from yesterday, which is just below the 1-year average while breadth had 2,410 advancers and 1,346 decliners. The 511 Mainland Chinese companies within the MSCI China All Shares Index gained +1.91% led by staples +4.11%, health care +2.66%, discretionary +2.44%, materials +1.98%, tech +1.88%, industrials +1.41%, and utilities +1.26%. Meanwhile, real estate -0.23%. Northbound Stock Connect had moderate volumes as foreign investors sold $276 million worth of mainland stocks today and Northbound Stock Connect trading accounted for 7.6% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.45 versus 6.44 yesterday

- CNY/EUR 7.83 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.82% versus 1.67% yesterday

- Yield on 10-Year Government Bond 3.24% versus 3.23% yesterday

- Yield on 10-Year China Development Bank Bond 3.72% versus 3.70% yesterday