Markets Reverse as Value Outperforms Growth

3 Min. Read Time

Key News

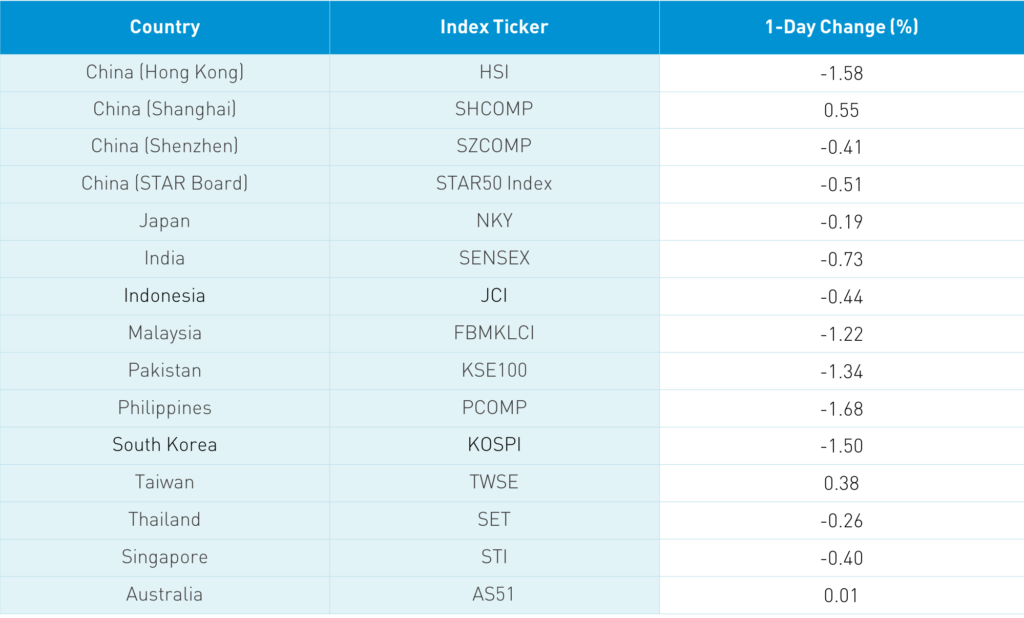

Asian equities were a sea of red following the US equity market lower overnight as only Shanghai, Taiwan, and Australia managed to end in the green. As one of our brokers noted, the market did the exact opposite of what was expected as profit-taking hit outperforming stocks and sectors. There was no catalyst as laggard value sectors outperformed YTD winners in growth sectors. The Hang Seng opened higher but quickly started to descend, closing down -1.58% at 30,595 led by Hong Kong volume leaders Tencent, which fell -1.32%, Meituan, which dropped -5.18%, China Mobile, which was up +2.02%, Alibaba Hong Kong, which was off -2.47%, Xiaomi, which fell -2.37%, healthcare IPO New Horizon Health, which gained +215%, energy giant CNOOC, which rose +1.5%, Semiconductor Manufacturing, which was up +2.6%, Kuaishou Tech, which fell -5.16%, and Hong Kong Exchanges, which gained +0.35%.

Southbound Connect reopened and accounted for 18% of Hong Kong turnover. Mainland investors were significant buyers of Hong Kong-listed stocks. Tencent was a significant beneficiary of Southbound flows despite its weakness overnight. Meanwhile, Meituan saw a rare net sell day. Growth stocks took the brunt of profit-taking as favored sectors such as health care, electric vehicles, clean energy, and e-commerce all took a hit. E-commerce’s weakness is somewhat surprising since Reuters reported that the Ministry of Commerce stated that sales by “key retail and catering companies” over Chinese New Year increased by +28.7% year-over-year to $127B. Home appliances, clothes, and fitness equipment saw a significant uptick from consumers.

Shanghai was lifted by value sectors by +0.55%, while the growth selloff weighed on Shenzhen and the STAR board, which were off -0.41% and -0.51%, respectively. Stocks and sectors that have outperformed year-to-date were hit overnight. Mainland volume leaders included alcohol stock Kweichow Moutai, which fell -5% negating my theory that foreign buying would lift the stock, electric vehicle (EV) maker BYD, which was off -2.98%, EV battery maker CATL, which fell -3.79%, and several consumer plays such as appliance maker Midea, which fell -8.23% and Muyuan Food, which dropped -4.62%. Energy, financials, and lithium plays did well overnight.

Foreign investors purchased $784 million worth of Mainland stocks overnight in heavy Northbound Connect trading. Bonds were off a touch while CNY eased slightly versus the dollar. Copper played catch up to global markets, rallying +4.25%.

The Financial Times had an excellent piece reporting on Japanese companies operating in China. Early adopters have done well in China though they face increasing competition from local players. I posted the article on Twitter yesterday. I don’t post often but will try to share articles worth reading. Check me out: @ahern_brendan.

In a blow to conspiracy theorists, the Chinese Academy of Sciences’ Institute of High Energy Physics denied that it is working on a time machine.

A local Hong Kong media source noted that a survey of participants in Hong Kong’s Mandatory Provident Fund believe China A-Shares should be added as an investment. With nearly HKD 1 trillion ($129B), that would be a good inflow.

Baidu reported strong results beating analyst expectations after the NY close led by its core search business, which gained +6% year-over-year (YoY) to RMB 23.1B ($3.54B). The company continues to buy back stock in a strong sign of its confidence that its stock is undervalued. AI and its Apollo Self Driving were highlighted by the company. The company’s Q1 2021 forecast was quite strong.

- Revenue +5% YoY to RMB 30.263B ($4.638B) versus analyst estimate RMB 30.056B ($4.654B)

- Gross Margin versus 49% Operating Profit RMB 6.868B ($763mm) versus $979mm RMB 6.324B

- Adjusted EPS declined -18% to RMB 15.05 ($2.31) versus estimate RMB 17 ($2.63)

- Adjusted Net income declined -26% to RMB 6.868 ($1.053B) versus RMB 5.77 ($894mm) Q1 2021

- Revenue forecast expected to grow between 15% and 26%, which is $4B to $4.4B

H-Share Update

The Hang Seng opened higher but quickly started a descent, closing down -1.58% at 30,595. Turnover jumped up +35.9% from yesterday, which is 196% of the 1-year average while breadth had 14 advancers and 35 decliners. The 196 Chinese companies listed in Hong Kong within the MSCI China All Shares Index lost -2.31%, with real estate up +0.45%, but discretionary off -4.32%, health care -4.12%, tech -3.6%, staples -2%, financials -1.72%, industrials -1.62%, communication -1.38%, materials -1.16%, and utilities -0.86%. Southbound Stock Connect volumes were very high as Mainland investors bought $1.832B of Mainland stocks as Southbound Connect trading accounted for 18.4% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen diverged with the former up +0.55% and the latter off -0.41%, closing at 3,675 and 2,450 respectively. Volumes were 24% higher than last Wednesday, which is 124% above the 1-year average while breadth had 1,303 advancers and 211 decliners on the Shanghai as Shenzhen data was unavailable. The 511 Mainland stocks within the MSCI China All Shares Index were off -1.15%, as energy rose +5.54%, real estate +2.8%, materials +2.36%, and financials +1.13, while health care fell -4.62%, staples -4.3%, industrials -1.32%, discretionary -1.25%, and tech -0.25%. Northbound Stock Connect volumes were very high as foreign investors purchased $784mm of Mainland stocks as Northbound Connect trading accounted for 10.1% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.49 versus 6.46 last Wednesday

- CNY/EUR 7.83 versus 7.77 yesterday

- Yield on 1-Day Government Bond 1.90% versus 1.82% last Wednesday

- Yield on 10-Year Government Bond 3.28% versus 3.24% last Wednesday

- Yield on 10-Year China Development Bank Bond 3.77% versus 3.72% last Wednesday

- China's Copper Price +4.25% overnight