Renminbi Rises Too Much Too Soon, China Moves to Three Child Policy

3 Min. Read Time

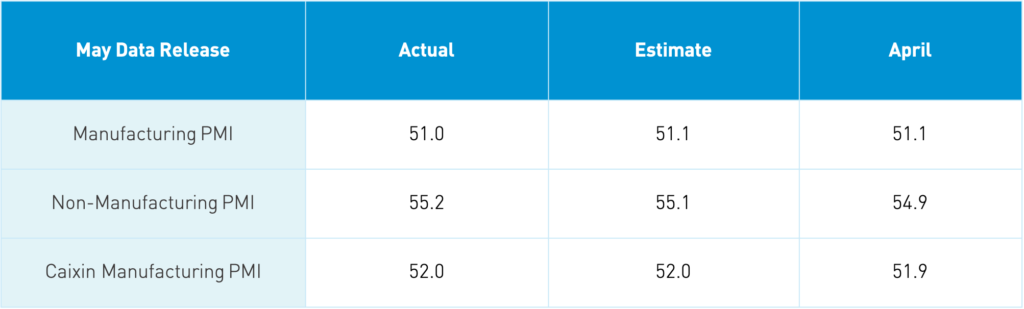

May Data Release

Takeaway: Today’s release was in line with economist expectations. The “official” PMI’s survey is conducted by the National Bureau of Statistics versus the Caixin survey, which is conducted by IHS Markit. PMIs are a diffusion index with readings over 50 indicating growth month-over-month. Within the “official” Manufacturing PMI, it is worth noting that both input and output prices were very high at 72.8 and 60.6. The disparity between input and output prices indicates that manufacturers are eating some element of the price difference, though price increases are being passed along. Business activity expectations for both “official” PMIs were strong, indicating that China and the global economy’s rebound is apt to continue.

Key News

Asian equities were largely higher overnight in a quiet night with China-driven headlines. First, we had yesterday’s news that the PBOC will raise the foreign exchange reserve ratio on June 15th for Chinese banks to 7% from 5% – the first adjustment in fourteen years. The renminbi’s strong appreciation versus the US dollar appears to have been too much too soon for policymakers. Second, China will allow couples to have up to three kids in an effort to mitigate demographic trends. The key will be policies that support families who choose to have more kids as the little buggers are expensive, especially in cities. Lastly, we also had more talk of curtailing rising commodity prices by raising margin requirements in commodity futures.

Ultimately, it is hard to slap the invisible hand of the market as the currency and commodity prices are reflective of global interest rate differentials and supply/demand dynamics. Investors have cheered Meituan’s results and the CEO’s comments on regulations not negatively impacting business following the release of Q1 2021 financials after Friday’s Hong Kong close. Yesterday, Meituan rose +10.86%, and today it rose +6.46% as growth stocks performed well both today and yesterday.

Inflation has become the topic du jour. Thankfully, we have a relationship with Nancy Davis who runs Quadratic Capital who has previously worked in senior fixed income investment roles prior to starting the firm. I recommend reading Nancy’s latest thoughts on the topic!

Reading Liars Poker in high school got me hooked on finance and Michael Lewis’ books ever since. I was very saddened to hear that Mr. Lewis’s daughter was killed in a car accident. My condolences to the Lewis family.

H-Share Update

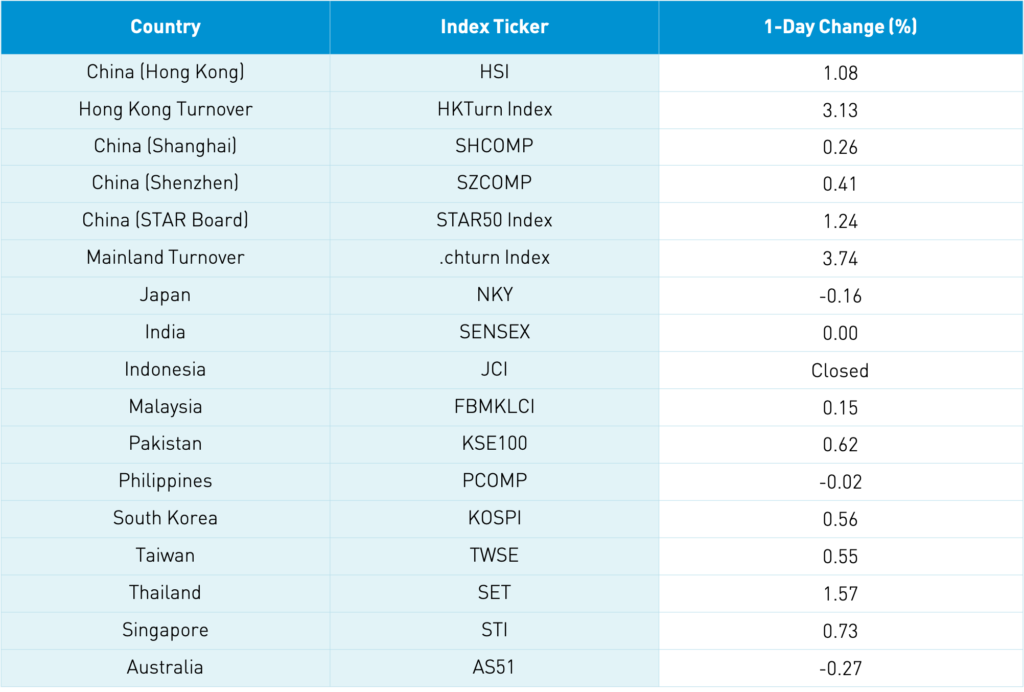

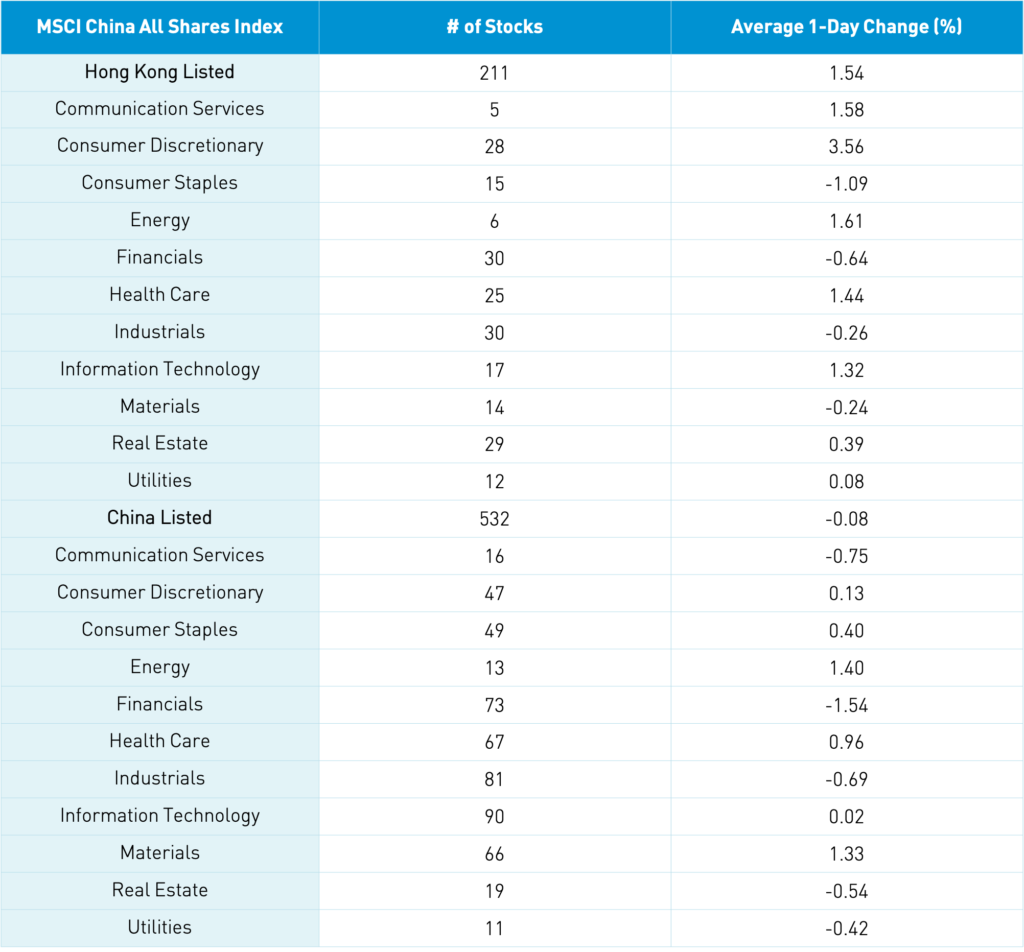

The Hang Seng opened lower but grinded higher to close up +1.08% at 29,468 as volume increased 3.16% from yesterday, which is just below the 1-year average. The 211 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +1.54% led by discretionary +3.56%, energy +1.61%, communication +1.59%, healthcare +1.44% and tech +1.32% while staples -1.09% and financials -0.63%. Hong Kong’s most heavily traded by value were Metiaun, which rose +6.46%, Tencent, which rose +1.45%, Alibaba HK, which rose +3.41%, Xiaomi, which fell -0.17%,, Kuaishou Technology, which rose +9.21%, BYD, which rose +6.06%, AIA, which rose +1.21%, Wuxi Biologics, which rose +2.8%, JD Logistics, which rose +10.23% on news that it will join the Hang Seng Index on June 11th, and JD.com HK, which rose +2.27%. Southbound Stock Connect volumes were moderate as Mainland investors bought $682mm of Hong Kong stocks as Southbound trading accounted for 14.2% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board gained +0.21%, +0.41%, and +1.24% respectively as volume increased +3.74%, which is 114% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares Index were off -0.09% as energy gained +1.4%, materials +1.33%, and healthcare +0.95% while financials -1.55%, communication -0.76%, and industrials -0.7%. The Mainland’s most heavily traded by value were BYD, which rose +6.02%, Sany Heavy Industry, which rose +4.39%, Kweichow Moutai, which rose +1.03%, CATL -2.02%, broker East Money, which fell -1.38%, COSCO Shipping, which rose +4.59%, Wuliangye Yibin, which rose +0.18%, Changan Auto, which rose +0.17%, Changchun High & New Technology, which rose +5.21%, and Longi Green Energy, which fell -0.98%. Northbound Stock Connect volumes were moderate/high as foreign investors bought $172mm of Mainland stocks following yesterday’s purchase of $818mm as Northbound Connect trading accounted for 5.7% of Mainland turnover. CNY depreciated slightly overnight, bonds were flat, and copper posted a small gain.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.38 versus 6.37 yesterday

- CNY/EUR 7.80 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.71% versus 1.76% yesterday

- Yield on 10-Day Government Bond 3.04% versus 3.04% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- China’s Copper Price +0.34% overnight