Hong Kong Internet Rebounds Overnight

7 Min. Read Time

At the bottom of today’s note is a review of what got us here and where we are going.

Key News

Asia was largely off as Hong Kong rebounded while mega-caps in China outperformed. Tuesday’s Hong Kong plunge was likely exacerbated by warrants hitting knock-out levels. Warrants are structured products built by investment banks using a stock’s options. Local investors want principal protection as they can earn high rates of return in bonds and money market funds. Banks build principal-protected structured products by buying calls on a stock while also buying puts. These products, therefore, have price levels that require the structured products to terminate when levels are hit to the downside. The banks hedge themselves using the underlying stock. So, Tuesday’s drop led the bank to sell stock in as the structured products hit the downside. Last night I hit my local Hong Kong expert Ken who agreed with my theory.

Mainland markets were led higher by mega-caps as healthcare was very strong overnight as cases in Japan and Indonesia have spiked and several flare-ups were seen in China. It is likely China’s “national team”, government-affiliated institutional investors such as pension plans, were buying overnight in the Mainland market. Known as the plunge protection team, these are long-term buyers that simply buy low when there is panic selling sticking to high-quality large/mega caps. There was a significant amount of Mainland financial media coverage going into today on the irrational move in Mainland equities Monday and Tuesday.

EV battery behemoth CATL spiked +6.07% after announcing the development of a sodium-ion battery. Semiconductors and the STAR Board were off overnight, nullifying, at least in the short term, my theory yesterday that policy wants to see capital committed to industries that will lead China’s economy in the decades to come.

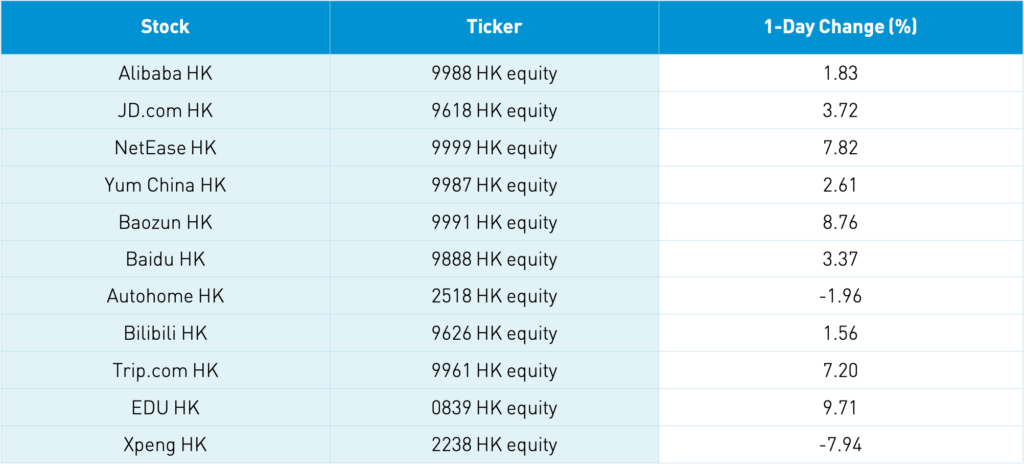

Hong Kong saw internet names rebound overnight as they are buys for value investors. Volumes in Tencent +0.27% and Meituan +7.53% were massive.

The Ministry of Industry and Information Technology (MIIT) announced that a six-month review period for internet companies commenced on July 23rd. This would provide a finish line to regulation, which investors should cheer. The announcement isn’t necessarily a bad thing as we continue to see companies adhere and adapt to regulation with Q4 2020 earnings reported in February and Q1 2021 earnings reported in May were strong.

Alibaba released a letter from Chairman and CEO Daniel Zhang in advance of their financial results next Tuesday. Interesting timing right? The letter speaks to the strength of their retail business, growth of cloud computing unit and SE Asia e-commerce unit, Lazada. It notes they paid their fine and will continue to adhere.

Apple’s net sales included a nice increase from China as revenue grew to $14.762B versus $9.329B year over year in Q2 and $53.803 versus $32.362B year to date year over year.

A Mainland media source is reporting that foreign ownership caps might be scrapped as Volvo wants to buy out parent Geely. The scrapping of foreign ownership caps (currently 30% for stocks) would check a box for MSCI’s inclusion of Chinese A Shares.

H-Share Update

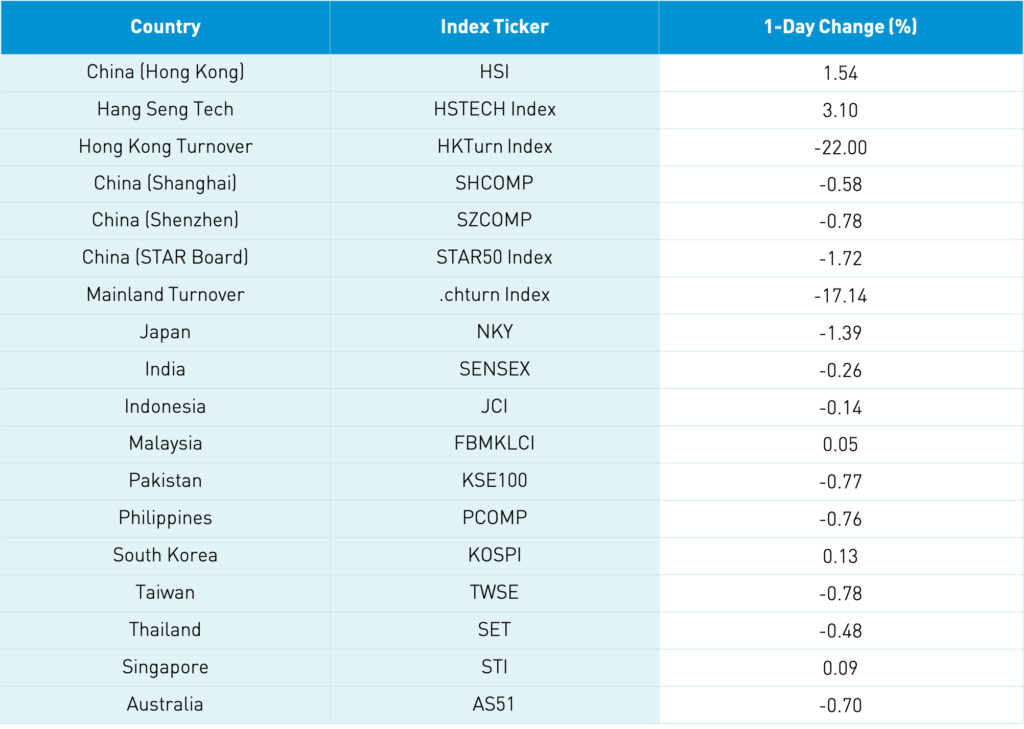

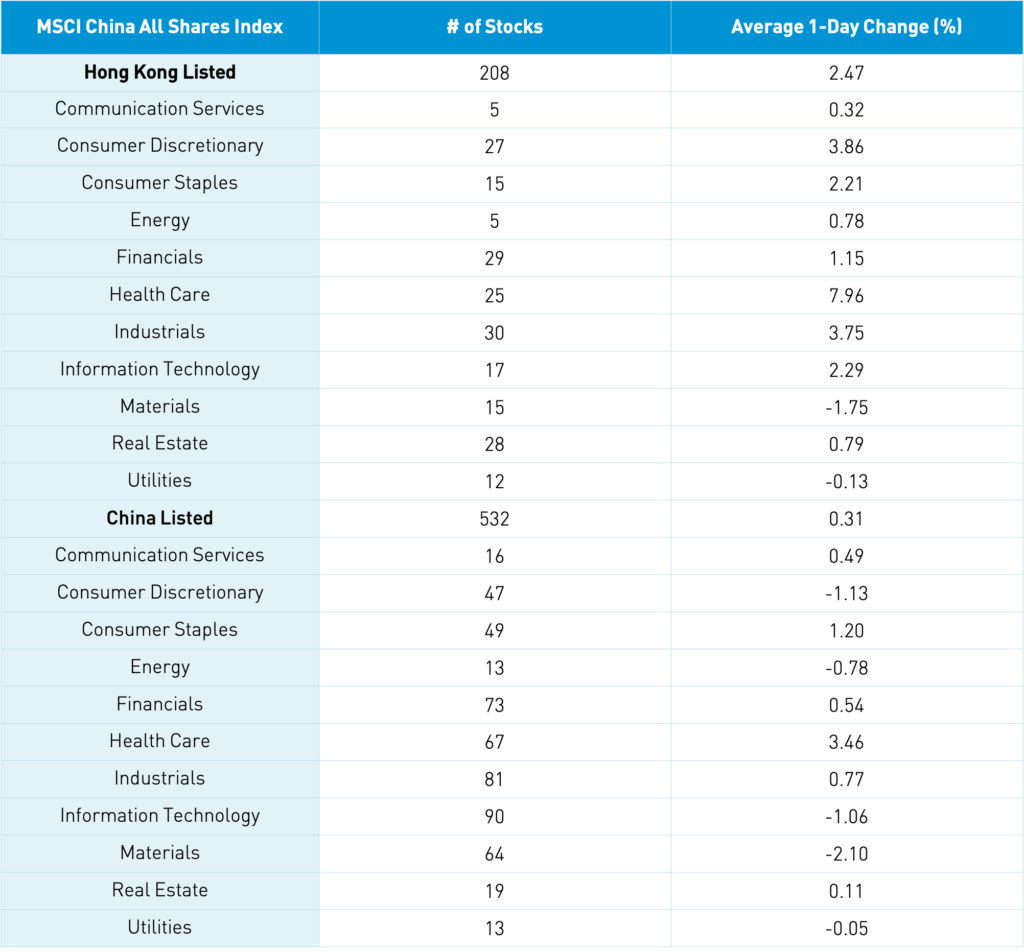

The Hang Seng Index bounced around the room swinging between gains and losses twice intra-day rallied into the close+1.54% while the Hang Seng TECH gained +3.1%. Volume was off -22% from yesterday though still 170% of the 1-year average. The 208 Chinese companies listed in Hong Kong gained 2.47% led by healthcare +7.96%, discretionary +3.85%, industrials +3.75%, tech +2.29%, staples +2.21%, financials +1.15%, real estate +0.79%, energy +0.77%, and energy +0.31% while materials -1.75% and utilities -0.13%. Hong Kong’s most heavily traded by value were Tencent +0.27%, Meituan +7.53%, Alibaba Hong Kong +1.83%, Hong Kong Exchanges +1.16%, Wuxi biologics +10.38%, AIA -0.73%, SMIC -1.57%, Xiaomi +3.08%, Ping An +1.54% and ANTA Sports +1.54%. Southbound Stock Connect volumes were high as Mainland investors sold a massive $1.714B of Hong Kong stocks as Southbound Connect trading accounted for 15.1% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board were off the lows closing -0.58%, -0.78% and -1.72% on volume down -17% from yesterday which is 140% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares gained +0.31% led by healthcare +3.46%, staples +1.2%, industrials +0.77%, financials +0.54%, communication +0.49% and real estate +0.11% while materials -2.1%, discretionary -1.13%, tech -1.06%, energy -0.78% and utilities -0.05%. The Mainland’s most heavily traded by value were Kweichow Moutai +3.2%, CATL +6.07%, SMIC -7.98%, Longi Green Energy +2.13%, East Money -1.58%, Wuliangye Yibin +2.39%, China Northern Rare Earth -2.33%, Tianqi Lithium-4.29%, Sanan Optoelectric +2.27% and BYD -0.93%. Northbound Stock volumes were high as foreign investors bought $1.239B of Mainland stocks as Northbound trading accounted for 5.8% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.50 versus 6.50 Yesterday

- CNY/EUR 7.67 versus 7.65 Yesterday

- Yield on 10-Year Government Bond 2.93% versus 2.91% Yesterday

- Yield on 10-Year China Development Bank Bond 3.31% versus 3.30% Yesterday

- Copper Price +0.13% overnight

How we got here:

Governments globally are beginning to deal with the mass and rapid adoption of technology. We saw this happen in 2018 with the European Union’s General Data Protection Regulation (GDPR). 30% of all retail sales in China flow through the country's internet platforms. Working in finance, we are highly regulated. But, who regulates Amazon or Facebook? China is responding to the importance of these companies to the economy.

Regulation is multi-faceted though the lack of a game plan is making it appear to have been done in an ad hoc/whack-a-mole manner. The market hates uncertainty so the apparent lack of a game plan is problematic. Regulation has hit fintech (if you act like a bank you need to be regulated like a bank), anti-trust (no banning your competitors), and data security/user privacy. Companies in these industries have adopted and adhered to the regulations despite the constant negative narrative. The proof of this is in Q4 2020 earnings, which were reported in February, and again in Q1 2021 earnings, which were reported in May. We have Alibaba reporting next Tuesday post-Hong Kong close, which hopefully will provide a catalyst.

The one area where the companies have been hurt is after-school tutoring (AST) (small exposure/~1% in our flagship China internet strategy). We knew AST was going to get hit, but it was worse than anticipated as for-profit companies were banned from engaging in K-12 AST. What’s the rationale? A China media source noted that upwards of 25% of urban family income is spent on AST. China’s census showed a few months ago that the birthrate is 1.3 children per woman. Policies will be implemented to reduce the financial costs of having children. We might not like it, but there is a rationale. Getting apartment prices down could be the next focus.

Hedge fund Archegos was liquidated in February including the firesale of its portfolio at significant discounts, which included five US-listed Chinese companies. This weighed on the space as a whole as the stocks hit were held by investors that held other names in the space in addition to re-valuation by comparing these companies to one another. If company A is worth X, similar company B will be valued near X. The rapid ascent of Chinese internet stocks in January and early February was likely Archegos putting those trades on. I have nothing to confirm this, but it would explain the parabolic move higher.

Didi is a separate issue (not in our flagship China internet strategy). They likely should not have gone public before being regulated, which is why Ant Group’s IPO was stopped in Hong Kong. Ant’s IPO prospectus had pre-regulatory financials, which would have led to the stock cratering following the regulation announcement as we have seen with Didi. Didi will get a BIG fine. Meanwhile, Didi's IPO prospectus had 60 pages of risk factors.

US regulation is an issue as the Holding Foreign Companies Accountable Act (HFCAA) was signed into law in December. It states if US-listed Chinese companies don’t provide their audit review papers to the PCAOB for three years, they may face delisting. We do not yet know when the SEC will opine on enforcing HFCAA nor when the 3-year clock will start. Institutional investors like ourselves will convert our US listings into the Hong Kong share classes. The SEC should provide retail investors the same opportunity, though I’m told most retail broker-dealers (Schwab, Fidelity, TD) do not allow for ADR conversion today.

US-China political rhetoric is another overhang. China’s June imports are interesting as they show how well business people appear to get along but how poorly politicians are at communicating. China’s June imports from the US went up +37.6% year-over-year, Taiwan +32.6%, EU +34.1% and Australia +53.5%. The US-China Business Council recently reported that Texas overtook California as the top exporting state to China (LNG, oil).

Credit default swaps (CDS) on Alibaba and Tencent debt serve as insurance for holders of the bonds just like car insurance. Based on the equity reaction, you would think the cost to insure their debt would skyrocket. That was not the case as CDS have barely moved when comparing prices from a year ago. What do fixed income investors know we don’t?

More importantly, what are the catalysts to get things going again?

- Earnings starting with BABA next Tuesday post-Hong Kong close. We could see buybacks announced during the results.

- Technical chart appears to show capitulation/panic selling.

- Privatization announcements marked the low in the summer of 2015. As companies’ market cap reach levels of their cash position, we could see companies buy back their public shares and go private. Likely in the smaller companies but “feels” we are at those levels.

- The regulator narrative could spill into the real economy as foreign companies operating in China are apt to pause or voice concern. At a minimum clarity on the regulatory end game would go a long way to soothing investor concern.

- A shares reacted to regulatory concern Monday and Tuesday for the first time. While Mainland investors have considerable capital in Hong Kong, the Mainland’s move should be disconcerting.

- Massive valuation gap between China internet and US internet is hard to ignore.