China’s Securities Regulator Addresses Audit Issue, Consumer Data Protection Law Set, Week in Review

4 Min. Read Time

Upcoming Webinar:

Join us on August 26, 2021 at 11:00 am EDT for

Hockey Stick Growth: Opportunities From The Electric Vehicle and New Transportation Technology Ecosystem

Click here to register.

Week in Review

- According to an economic release Monday, retail sales, industrial production, and other economic indicators missed estimates in July as massive flooding and lockdowns weighed on China’s economic output compared to a year earlier when the nation had just emerged from quarantine.

- We began to see the light at the end of the tunnel when it comes to internet regulations on Tuesday as it was reported that China’s new anti-monopoly and consumer data protection laws will be finalized next month. While we may see further enforcement actions later this year, the new policies are likely to be fully implemented well before the National People’s Congress (NPC) in March 2022.

- Tencent reported strong Q2 results on Wednesday. The company’s revenues grew by +20%, which was just above the consensus estimate. However, gross margins were slightly off for the quarter, coming in at 45% versus last year’s 46%.

- The internet space saw more selling pressure Thursday despite Tencent’s positive earnings release. However, the Mainland market held its own as growth names outperformed including electric vehicles, clean technology, and semiconductors.

Friday’s Key News

“China CSRC to Create Conditions for Audit Cooperation With U.S.” was a Bloomberg headline today. Wow! This would put to bed the long-running issue of US-listed Chinese companies not being allowed to provide their audit papers to the PCAOB due to Chinese law. This issue led to the passing of the Holding Foreign Companies Accountable Act (HFCA) in both the House and the Senate, which stipulated that after three years of non-compliance the companies would be delisted. 100% of the companies should comply with this global standard. Changing the goalposts and hurting US investors does not make any sense. Anyway, let’s hope this leads to the issue being resolved.

There is talk that China’s Personal Information Protection Law will become effective in November. Regulation surrounding how internet companies protect user data and user privacy has been weighing on the China internet space. Remember that companies have been adjusting themselves in advance of the law becoming effective. This is a good thing! It means we have a finish line on this issue. Internet regulation is multi-faceted, but we know the fintech rules appear in place so we can check those off the list. The anti-monopoly law is out there, but the MIIT said it will conclude its review in four months. Nonetheless, the bureau recently announced that 68 companies have already complied with its rules. These are indications we are closer to the end. Yes, Didi will be fined significantly, but that is company-specific. Green shoots are appearing.

I could not imagine this week ending any different than it started. Asian equities did not let me down as we hit a red light, referencing Matthew McConaughey’s book Greenlights, which I recommend. My mood was similar to that of a Hong Kong broker, who noted sourly that Hang Seng’s announcements on new stock inclusions did not move the stocks being added, but neither have good earnings.

The shoot-first mentality spread to the Mainland market as a rumor that healthcare might fall under regulation led to a wholesale collapse in the space. Hengrui Medicine (600276 CH) missed earnings, but a literal rumor sent the entire market down. We also heard another rumor that liquor stocks might see prices capped, which sent the sector down significantly. Analysts and brokerage firms are coming to the defense of both sectors as they do not see either issue materializing.

Today’s market action must be noticed by policymakers as the media frenzy and lack of transparency on regulation is now spilling over into the Mainland market, which, I imagine, is quite disconcerting for policymakers. Again, these were rumors, but the reaction highlights the sentiment. Hong Kong’s downdraft was significant, though there was a silver lining. Mainland investors bought Tencent today, which has been a rare event in the last few months. One day is not a trend, but, rather, a positive sign.

H-Share Update

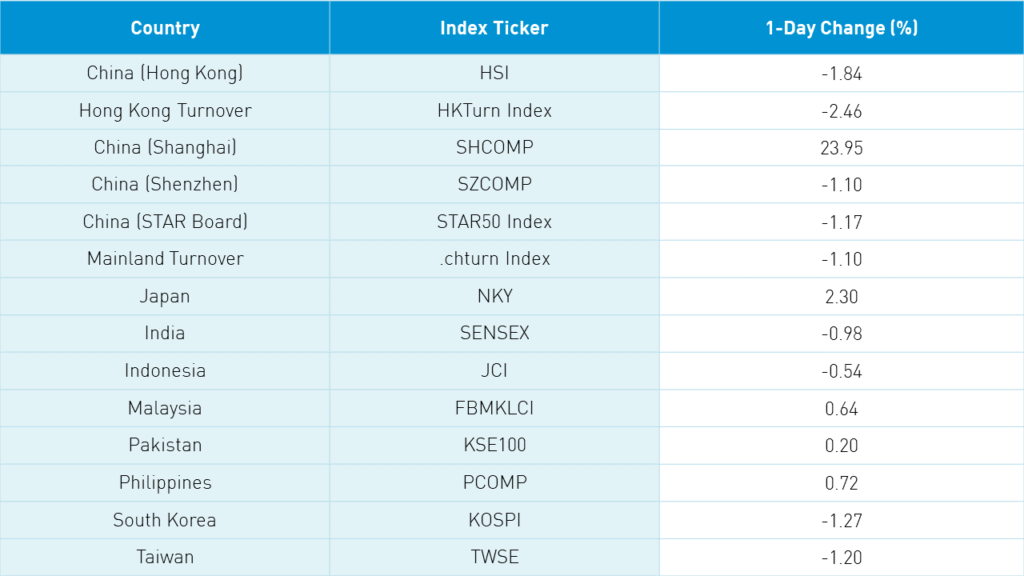

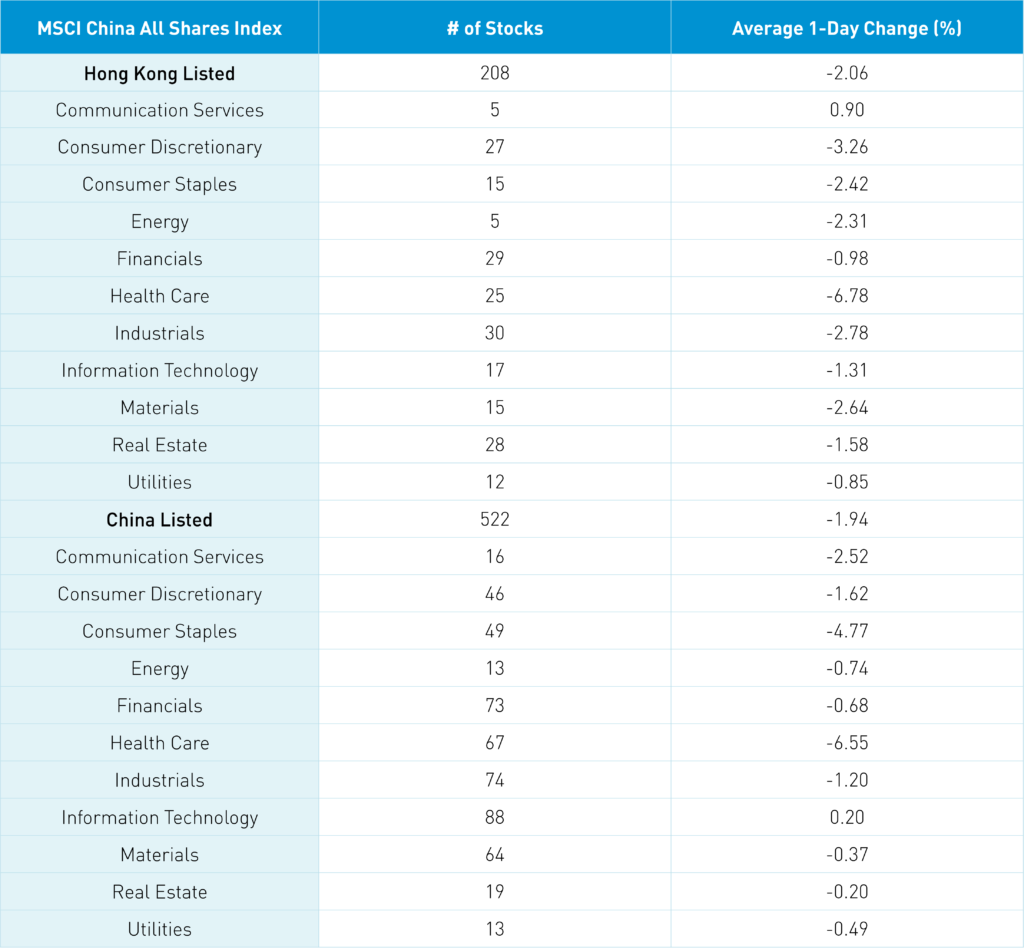

The Hang Seng opened lower and kept that trajectory, closing -1.84% as volume increased +23.92% from yesterday, which is 122% of the 1-year average. The 208 Chinese companies listed in Hong Kong within the MSCI China All shares Index lost -2.06% with communication +0.91% while healthcare -6.77%, discretionary -3.26%, industrials -2.78%, materials -2.64%, staples -2.41%, energy -2.3%, real estate -1.58%, tech -1.3%, financials -0.98% and utilities -0.84%. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +1%, Meituan, which fell -4.54%, Alibaba HK, which fell -2.59%, Wuxi Biologics, which fell -7.47%, Hong Kong Exchanges, which fell -1.99%, BYD, which fell -3.1%, Kuaishou, which gained +3.5%, Xiaomi, which fell -2.29%, China Mobile, which fell -1.65%, and Geely Auto, which fell -3.92%. Southbound Stock Connect volumes were moderate/high as Mainland investors sold -$382 million worth of Hong Kong stocks as Southbound trading accounted for 13.1% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were off -1.1%, -1.17%, and -1.1%, respectively, as volume increased +2.3%, which is 134% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares Index were off -1.95% with tech +0.18%. Meanwhile, healthcare -6.56%, staples -4.78%, communication -2.53%, discretionary -1.64%, industrials -1.21%, energy -0.76%, financials -0.69%, utilities -0.5%, materials -0.39% and real estate -0.21%. The Mainland’s most heavily traded stocks by value were China Telecom, which surged +35.78%, Kweichow Moutai, which fell -4.44%, Tianqi Lithium, which gained +6.06%, Wuliangye Yibin, which fell -7.31%, Qinghai Salt Lake, which gained +9.99%, Shenzhen Mindray, which fell -17.05%, China Northern Rare Earth, which gained +3.92%, Zhejiang Huayou Cobalt, which fell -6.17%, broker East Money, which fell -2.09%, and BYD, which fell -2.94%. Northbound Stock Connect volumes were elevated as foreign investors sold -$1.664 billion worth of Mainland stocks.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.50 versus 6.49 yesterday

- CNY/EUR 7.59 versus 7.59 yesterday

- Yield on 1-Day Government Bond 1.55% versus 1.55% yesterday

- Yield on 10-Year Government Bond 2.85% versus 2.84% yesterday

- Yield on 10-Year China Development Bank Bond 3.25% versus 3.24% yesterday

- Copper Price -0.47% overnight