Media’s “China Lehman Moment” Doesn’t Happen Due to a $35mm Bond Payment

2 Min. Read Time

Key News

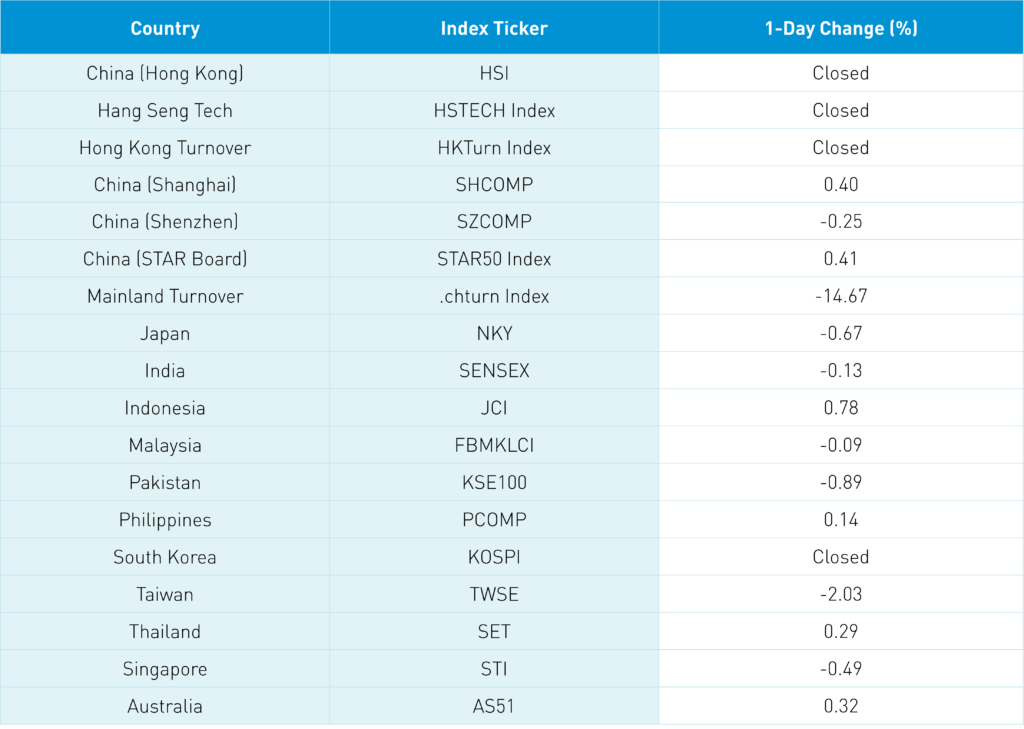

Asia was largely off, led by Japan and Taiwan which reopened post-holiday. South Korea and Hong Kong were closed on holiday.

As we suspected, the PBOC pumped nearly $19B of liquidity into the financial system overnight in a strong sign of policy support in light of Evergrande’s deteriorating financials. Shanghai and Shenzhen opened down -1.4% but grinded higher across the trading day.

Guess what one of the best performing sectors was in China today? Real estate! Why? According to our friend Kevin Liu, CICC’s equity strategist, it's because Evergrande grew too quickly taking on debt while many peers have not. Evergrande announced they negotiated with creditors on a $35.9mm bond payment due Thursday. How many billions were lost due to a $35.9mm payment! Talk about yelling fire in a crowded theater. Evergrande isn’t out of the woods as it owes $700mm through January. The company will have to negotiate similar deals to make these payments in order to stave off a default though I believe the government will push creditors to oblige. Financials were off today as banks are apt to take a haircut on their loans to Evergrande though it shouldn’t be meaningful for them.

Yesterday we met with Hong Kong Exchanges in advance of their rollout of MSCI China A 50 futures in October. It is anticipated that HKeX’s consultation on removing listing restrictions on allowing all US-listed Chinese companies to relist in HK should be done by year-end.

President Xi’s UN speech mentioned China will stop building coal-fired electric plants which sent mainland clean energy, hydro, nuclear, and ironically coal stocks higher. Consumer-related names such as wine/liquor were off as discretionary and staples lagged with delta restrictions likely crimping domestic travel during the four-day weekend.

I am in Chicago for Morningstar’s Investment Conference as I am on a panel Thursday. The hotel I am staying at is eerily empty as I feel like an extra in the Shining. Out of 1,100 rooms, only 30 are occupied as a nearby conference canceled dropping capacity from 50% to 3%. Not a good sign for cities if conferences don’t occur. Just an observation.

H-Share Update

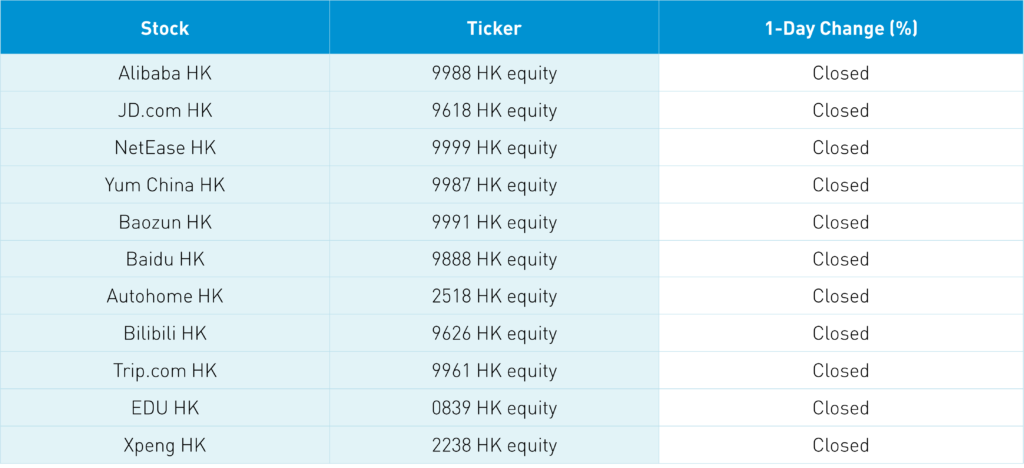

Hong Kong was closed today along with Southbound Stock Connect.

A-Share Update

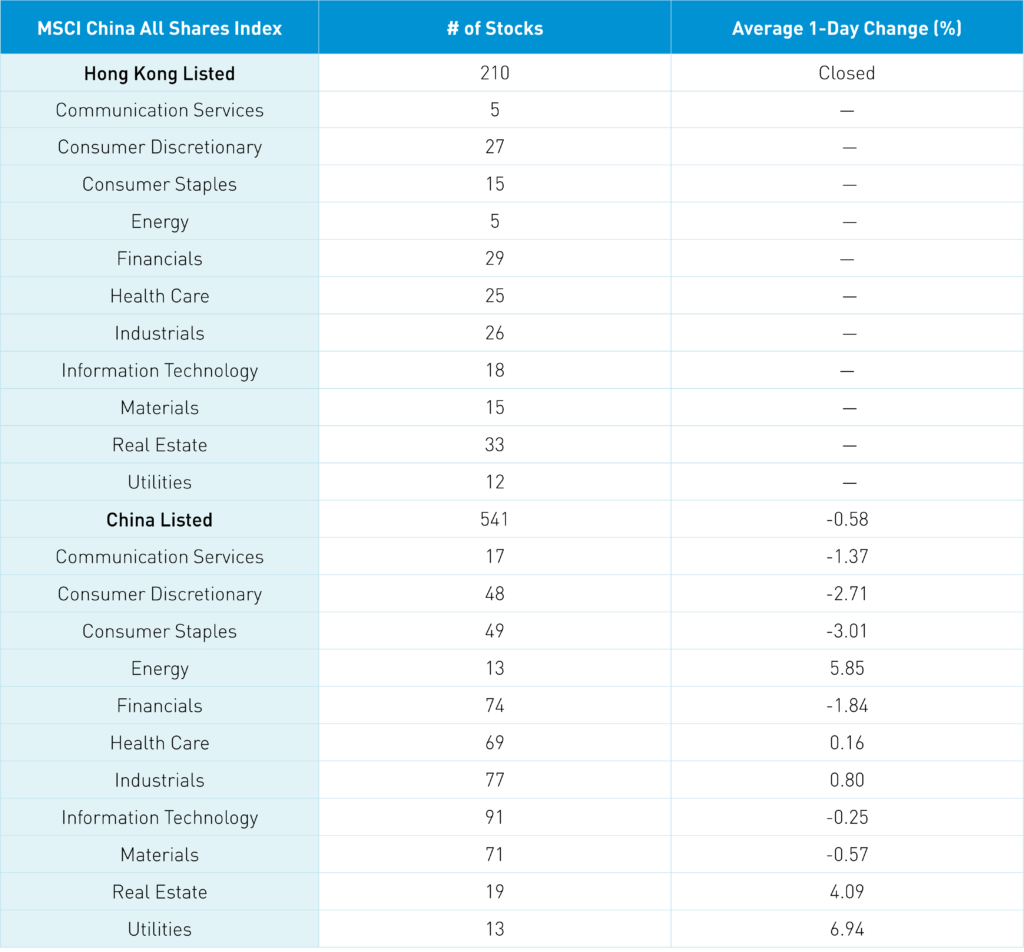

Shanghai, Shenzhen and STAR Board diverged closing +0.4%, -0.25% and +0.41% as volume declined -14.67% from Friday which is 119% of the 1-year average. The 541 mainland stocks within MSCI China All Shares were off -0.59% led by utilities +6.93%, energy +5.84%, real estate +4.09% while staples -3.02%, -2.72%, financials -1.84% and communication -1.37%. The mainland’s most active by value traded were China Three Gorges +9.97%, TBEA +9.32%, Tianqi Lithium -2.85%, China Northern Rare Earth +0.72%, Xinjiang Goldwind -1.27%, China Merchants Bank -3.59%, Kweichow Moutai -2.87%, China CSSC Holding +9.15%, Wuliangye Yibin -3.97% and Yunnan Yuntianhua +2.06%. Northbound Stock Connect was closed.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.47 yesterday

- CNY/EUR 759 versus 7.59 yesterday

- Yield on 10-Year Government Bond 2.86% versus 2.87% yesterday

- Yield on 10-Year China Development Bank Bond 3.19% versus 3.20% yesterday

- Copper Price -1.11% overnight