Mainland Growth Stocks Outperform, Evergrande Bonds Rally, Week in Review

3 Min. Read Time

Week in Review

- Clean energy stocks rose Monday as the State Council provided new non-fossil fuel energy consumption targets. Renewable energy is expected to reach 20% of energy production by 2025, 25% by 2030, and 80% by 2060.

- Real estate developer Modern Land missed a bond repayment worth $250 million, weighing on market sentiment and distracting from the clandestine meeting between Janet Yellen and Liu He.

- China’s September industrial profits gained +16.3% to RMB 738B versus August’s 10.1% rise driven by higher input prices, according to an official release Wednesday. Meanwhile, US-listed China stocks came under pressure from negative geopolitical headlines.

- Inflation fears weighed on overall market sentiment in Asia on Thursday as internet stocks outperformed.

Friday’s Key News

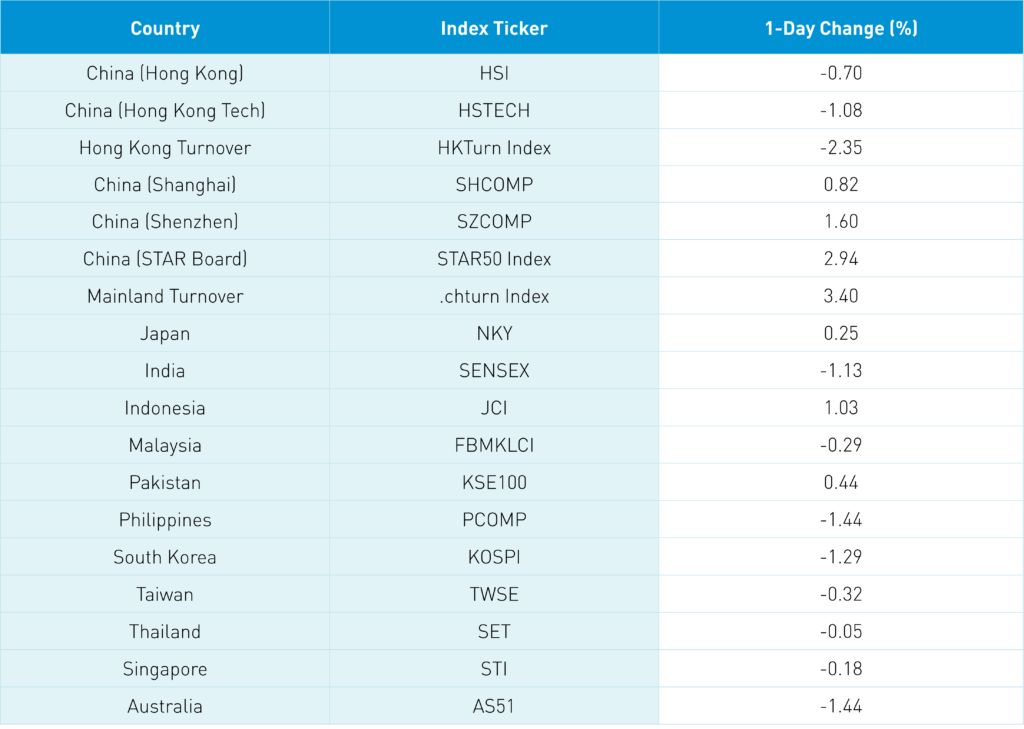

Asian equities were off following Apple and Amazons’ results weighing on sentiment as India and South Korea underperformed while China outperformed. Q3 earnings season kicked into high gear for both Hong Kong and Mainland China.

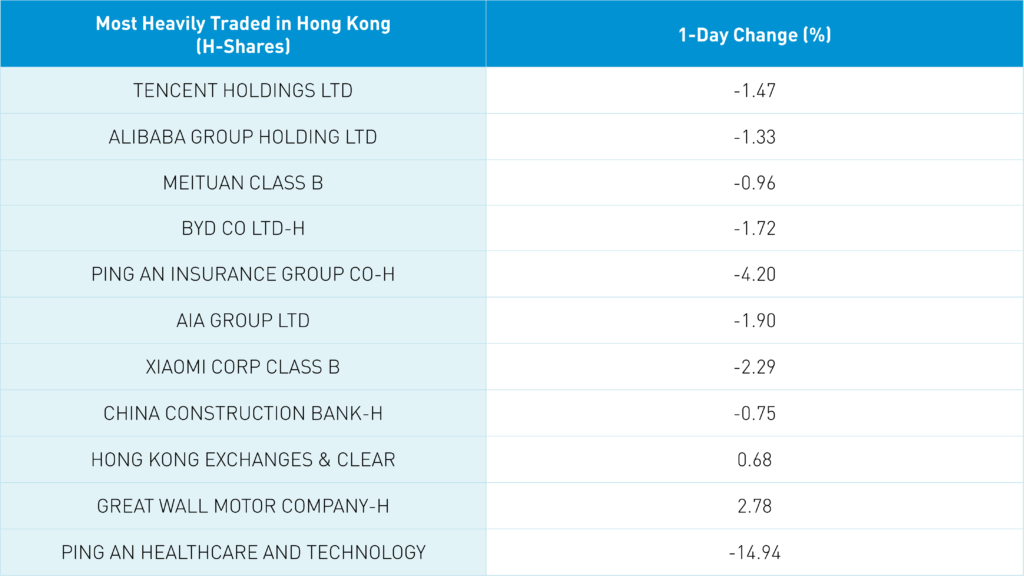

Electric bus maker and battery maker BYD (1211 HK) slipped -1.72% as Q3 revenue grew to RMB 54.3B from last year’s RMB 44.5B though net income declined to RMB 1.27B. After the close, the company announced it will sell 50 million shares, raising $1.8 billion at a price of HKD 273.50 to HKD 279.50 versus today’s closing price of HKD 296.60.

The Hang Seng Index was off -0.7% while the Hang Seng Tech Index was down -1.08% as internet stocks slipped following yesterday’s gain as Tencent fell -1.47%, Alibaba HK fell -1.33%, and Meituan fell -0.96%. Meituan and Kuaishou, both of which fell by -0.29%, were small net buys overnight while Tencent was a small net sell from Mainland investors via Southbound Stock Connect. The Wall Street Journal had a mildly positive article on Alibaba as the company’s low valuation is hard to ignore.

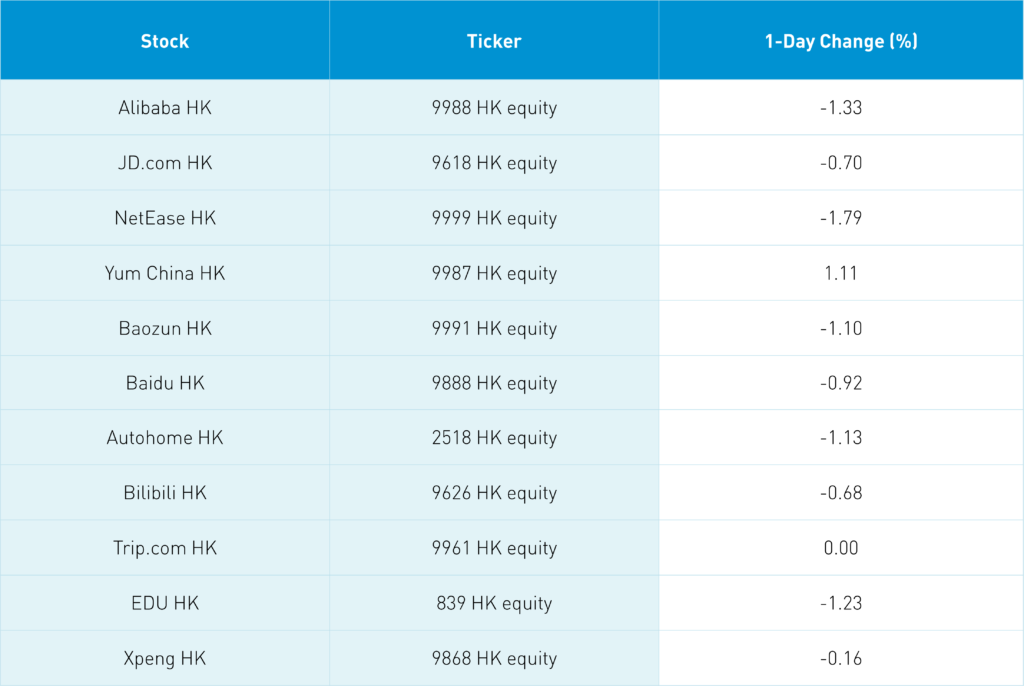

Internet medical stocks were weak on rumors that virtual doctor appointments could be banned as Ping An Healthcare and Technology (1833 HK) was clobbered -14.94%, JD Health fell -3.25%, and Alibaba Health fell -3.25%. I am not a buyer of the rumor as the sheer size of China geographically makes these companies a great resource for its rural population. The rumor’s results show how fragile sentiment can be.

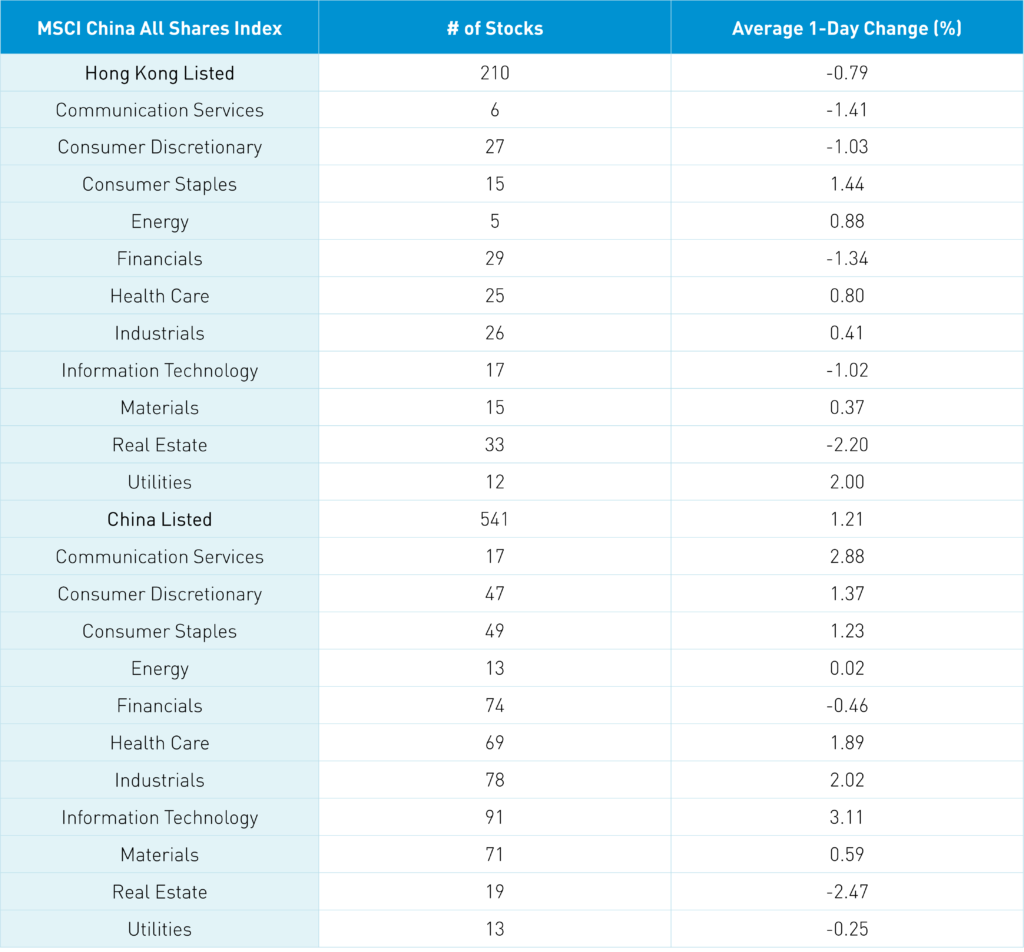

In Hong Kong, Utilities and staples outperformed, gaining +1.99% and +1.44%, respectively, while real estate fell -2.2%, communication fell -1.41%, and financials fell -1.34%.

Evergrande defied the common narrative again by making another coupon payment. As previously stated, the company is not out of the woods yet though a major bond restructuring is likely in the works. Evergrande’s bond due in April 2022 has risen from a low of $20.61 on October 14th to today’s close of $26.57.

Mainland China had a good day led by growth sectors as Shanghai gained +0.82%, Shenzhen gained +1.6%, and the STAR Board gained +2.94%. Tech gained +3.08%, communication +2.85%, industrials +1.99%, and healthcare +1.86%. Meanwhile, real estate was off -2.5% and financials -0.49%. The PBOC once again injected liquidity into the financial system by replacing RMB 100 billion worth of maturing repos with RMB 200 billion for a net injection of RMB 100 billion.

Bloomberg’s article on US-China political rhetoric improving garnered some attention. Unfortunately, President Xi will attend the G20 summit via video, making for a missed opportunity to meet with President Biden. Foreign investors bought $740 million worth of Mainland stocks today via Northbound Stock Connect, bringing the weekly total to $1.66 billion.

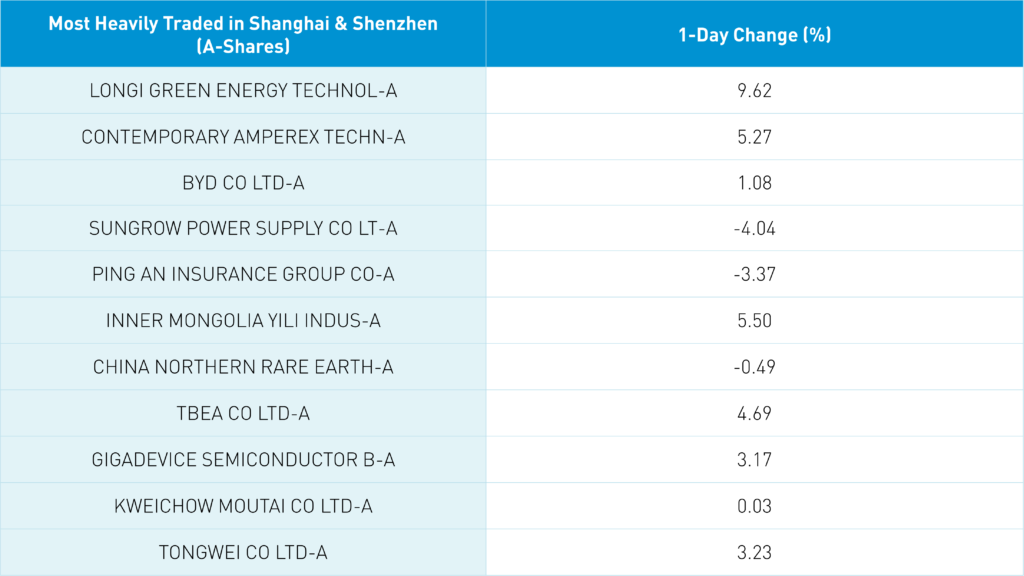

The Mainland’s most heavily traded stock overnight was that of Longi Green Energy Technology (601012 CH), which gained +9.62% after seeing significant buying from foreign investors. The catalyst was Q3 financial results as revenue increased +54% to RMB 21.1B and net income grew +14% to RMB 2.56 billion. Chinese Treasury bonds were flat, CNY was off a touch versus the US dollar, and copper gained.

Apple’s revenue missed analysts’ expectations by a hair though it is worth pointing out that Apple’s Greater China sales doubled from Q3 2020 to $14.563 billion from $7.946 billion. For the past year, Greater China increased to $68.366 billion versus the previous year’s $40.308 billion. The reports of the death of the Chinese consumer have been greatly exaggerated!

Hong Kong Exchanges’ new MSCI China A50 futures seem to be picking up steam as volume picked up steadily along with open interest. Four mainland ETFs will be launching soon based on the index after having raised nearly $4 billion during their subscription periods.

For intra-day updates, I can be followed at @ahern_brendan on Twitter. I can’t get my kids to follow me!

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.41 versus 6.39 yesterday

- CNY/EUR 7.43 versus 7.47 yesterday

- Yield on 1-Day Government Bond 1.70% versus 1.54% yesterday

- Yield on 10-Year Government Bond 2.97% versus 2.97% yesterday

- Yield on 10-Year China Development Bank Bond 3.30% versus 3.31% yesterday

- Copper Price -0.61% overnight