Loan Support For Clean Tech Leads To Sector Rally

2 Min. Read Time

Key News

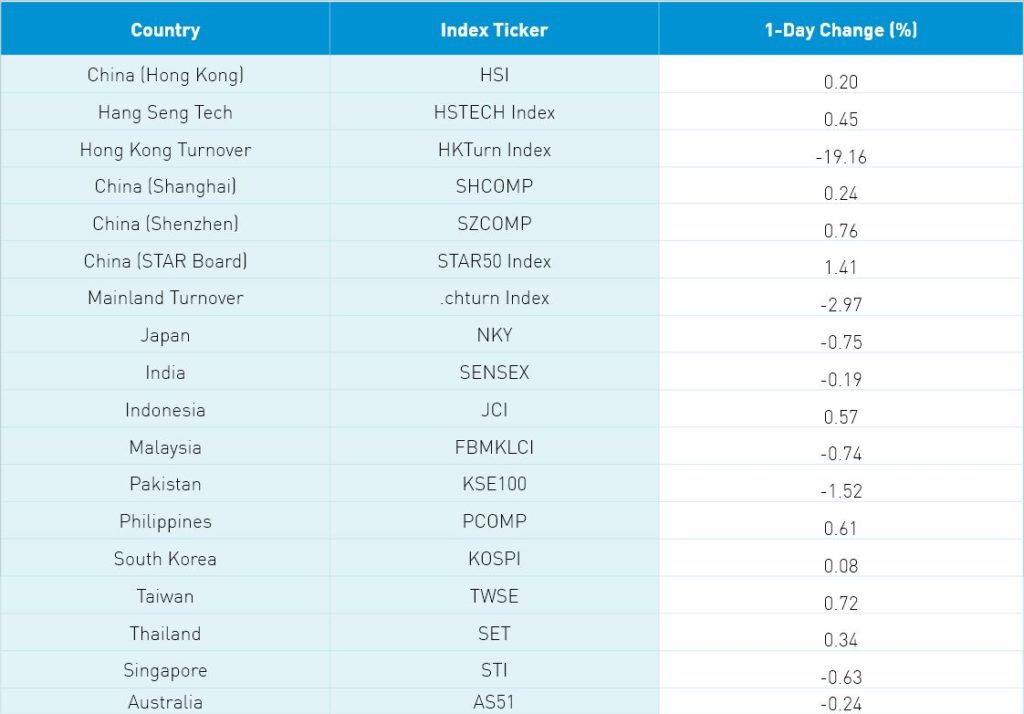

Asian equities had a mixed day with eerily quiet volumes, except for Taiwan, which had a decent day on strong volumes. The Hang Seng Index gained +0.2% on very light volumes that were only 57% of the 1-year volume. Shanghai, Shenzhen, and the STAR Board gained +0.24%, +0.76%, and +1.41%, respectively, on volumes that were just above the 1-year average.

Health care was a strong performer in both Hong Kong and China as the UK added Sinovac’s vaccine to its approved vaccine list. The clean energy ecosystem had a strong day following the PBOC guidance to banks to offer lower loan rates to companies helping China achieve its carbon goals.

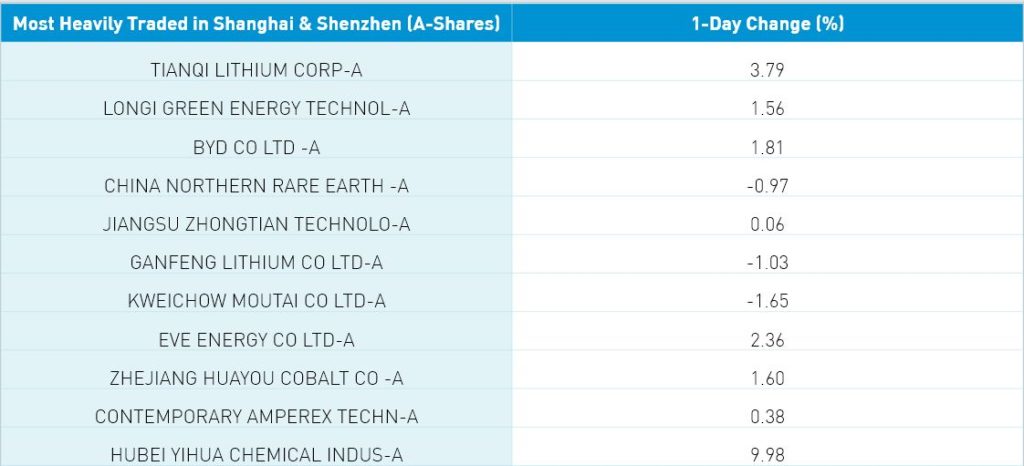

The Mainland’s top two most heavily traded stocks by value were Tianqi Lithium, which gained +3.79%, and Longi Green Energy, which gained +1.56%. Passenger cars slumped -14.1% in October year-over-year though gained month-over-month +8.4%. BYD rallied after announcing October sales of passenger electric vehicles (EVs) increased more than 300% year over year to 80,000, raising the year-to-date sales to 410,000. However, BYD’s EV bus sales fell. Semiconductors powered the STAR Board to a strong day.

Western media headlines are screaming about China’s real estate market, though Mainland media is not at all! A Mainland media source noted that Goldman Sachs was buying Chinese real estate companies’ debt as spreads versus US high yield hit record levels. Evergrande’s April 2022 bond slipped -2.35% to $29 while the June 2025 bond fell -2.24% to $25. The PBOC replaced RMB 10 billion worth of maturing repos with RMB 100 billion, providing a solid liquidity injection.

Hong Kong and China may loosen travel restrictions, with the latter aiming for opening in early Q2.

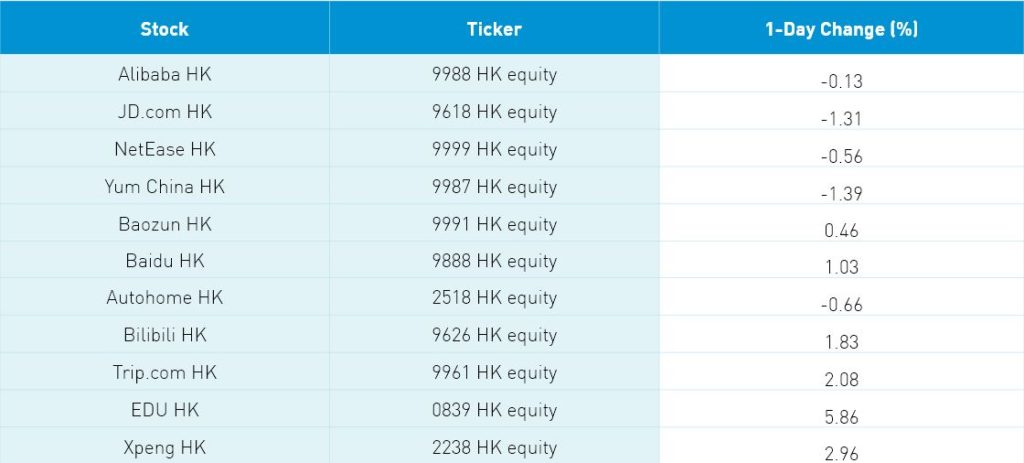

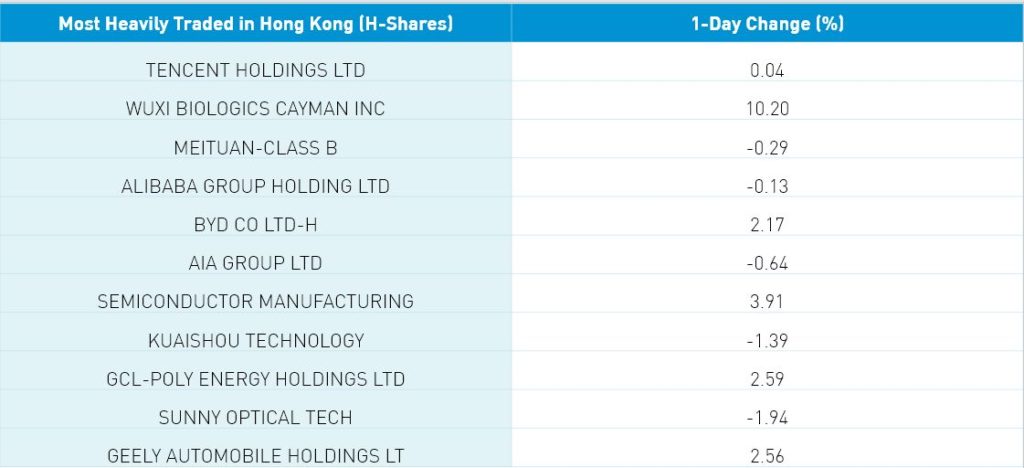

Hong Kong internet stocks had a mixed day with Tencent +0.1% on a small net sell via Southbound Stock Connect, Alibaba HK fell -0.13%, and Meituan fell -0.3% on net buying via Southbound Stock Connect. Tencent will report Q3 results after the Hong Kong close tomorrow. Foreign investors sold -$331 million worth of Mainland stocks today following yesterday’s sale of -$156 million, led by a decent sell in Ping An Insurance.

Online real estate company KE Holdings (BEKE US) beat revenue estimates handily though missed on EPS this morning. Tencent Music Entertainment (TME US) was similar though its revenue beat was small. Investors appeared to like BEKE’s earnings call as shares jumped pre-market.

Looking for a China macro update? The CFA Society Stamford is hosting me virtually next Thursday after the market close. Feel to register at: https://us02web.zoom.us/webinar/register/WN_f0pBfS3qRZK1kjAlw3hTLw

Next Thursday night is MSCI’s pro forma release for the December 1st Semi-Annual Index Review, which will require passive managers to trade at the close on November 30th.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.39 Yesterday

- CNY/EUR 7.40 versus 7.41 Yesterday

- Yield on 10-Year Government Bond 2.90% versus 2.90% Yesterday

- Yield on 10-Year China Development Bank Bond 3.17% versus 3.18% Yesterday

- Copper Price +0.70% today