MSCI Grabs GRAB, Seeks SE, and Loves LU

3 Min. Read Time

Upcoming Webinar: Join us on Tuesday, February 15, 2022 for our webinar at 10:00 am EST.

Get Your “A” Game On – KraneShares and MSCI Discuss the Future of Investing in Mainland China

Click here to register.

Key News

Asia’s equity markets had a decent day as Northern Asia markets outperformed Southern Asia markets with a hint of the global growth/value rotation showing. There are a few items to discuss.

Last night MSCI released its Pro-forma for the quarterly index review (QIR), which will require passive index fund and ETF managers to rebalance/trade their portfolios at the end of the month. The big surprises were the new additions of Southeast Asian ride-sharing company Grab, airplane leasing company AerCap, and fintech company Lufax to their global standard indexes. Southeast Asia-focused e-commerce/gaming company Sea Ltd will see the final and largest of its three-stage inclusion into MSCI Singapore and MSCI developed market indexes.

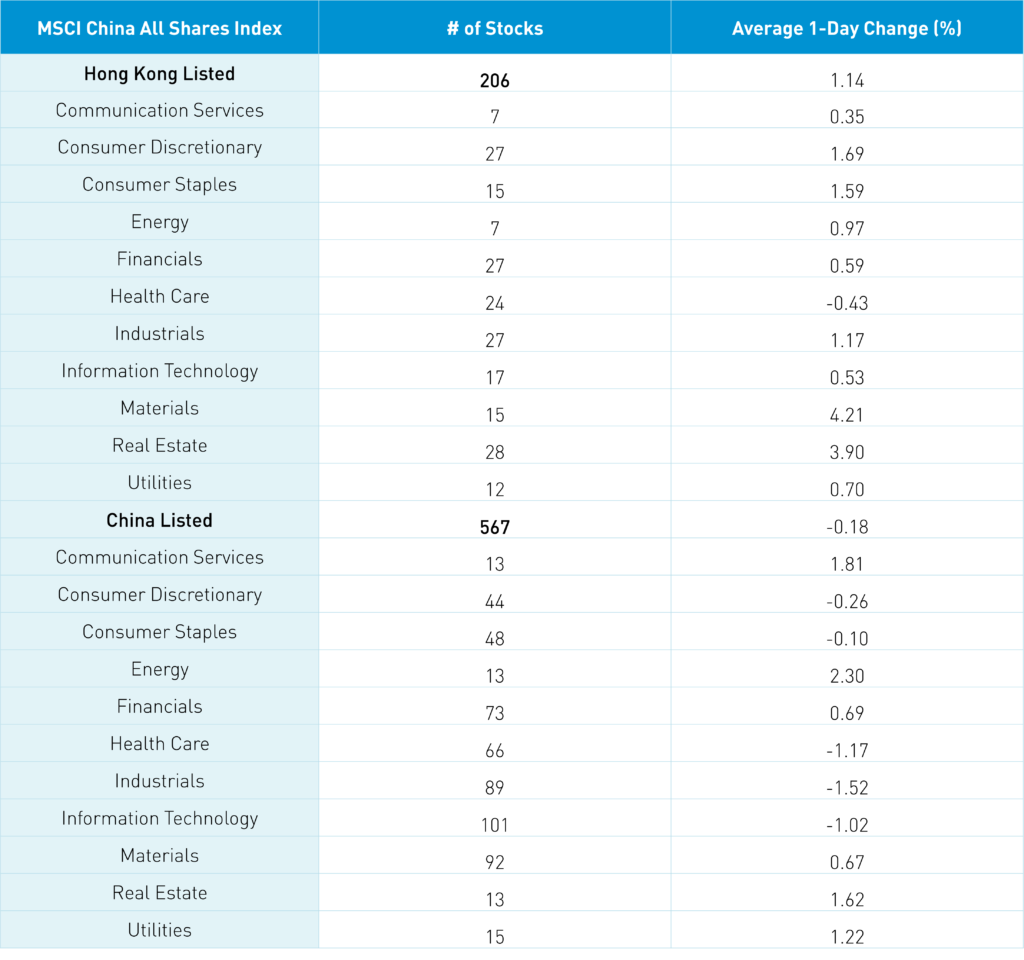

China’s weight in the MSCI Emerging Markets (EM) Index will increase from 32.1% to 32.2% as the country accounts for 14 of the 16 EM stock additions. China’s free-float market capitalization is now $2.558 trillion, which is nearly 2X Taiwan ($1.3 trillion), 2.5X bigger than South Korea ($981 billion) and India ($1.011 trillion), 2X MSCI Emerging Markets Europe, Middle East, and Africa ($1.125 trillion), and 5X bigger than MSCI Emerging Markets Latin America ($547 billion).

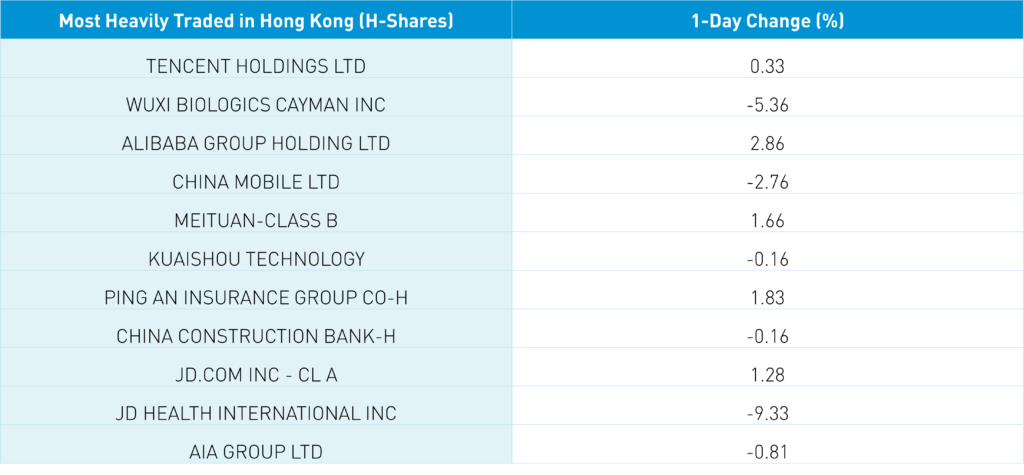

Tencent raised its stake in Didi to 78.9mm shares following its investment at IPO. Obviously, this is a great thing for Didi’s suffering shareholders (we hold zero shares as an FYI) but also another indication that China’s regulatory crackdown has ended or, at least, is in its late stages.

Wuxi Biologics (2269 HK) was off again overnight in Hong Kong, falling -5.36% after the US’ inclusion of the company on the “unverified list”. I believe investors are grossly misinterpreting this list as the company will very likely be removed in a few months. The only reason it is on the list is due to the pandemic as the US Commerce Department cannot verify the company. I am up to my eyeballs in China exposure candidly though I’m VERY tempted to be a buyer personally.

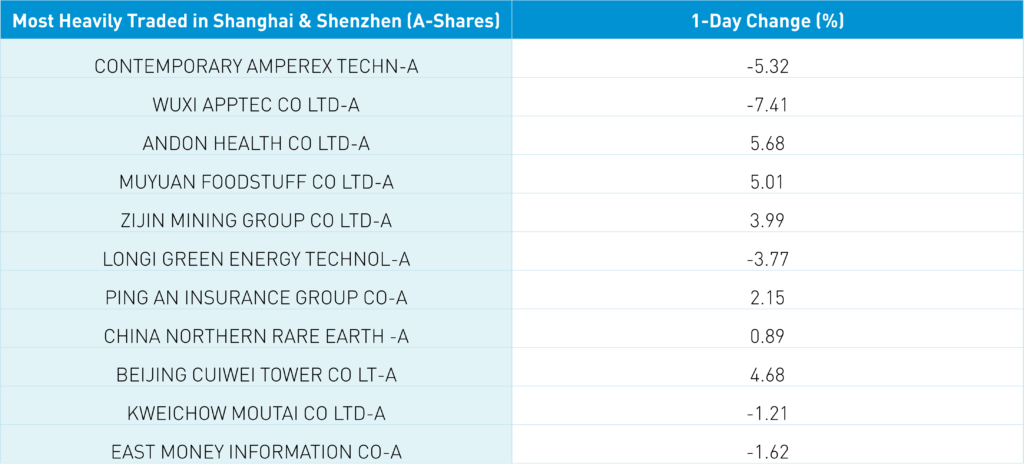

Healthcare was off overnight in Hong Kong, falling -0.44%, and on the Mainland, falling -1.18% on chatter that there is the potential for China’s drug procurement program to be expanded. Growth stocks/sectors/themes were weak on the Mainland as institutional investors rebalanced their portfolios between value and growth. As most investors are watching the Olympics, this rebalancing is occurring in the context of a thin tape and low volumes, which is causing big moves, i.e. CATL fell -5.32% overnight.

The Hang Seng Index bounced around the room as it opened higher and declined intra-day before rebounding to close +0.38%. Volumes were off -8.26% from yesterday, which is only 83% of the 1-year average while advancing stocks outpaced declining stocks by more than 2 to 1. Hong Kong internet stocks outperformed overnight as Tencent gained+0.33% and was the most heavily traded stock in Hong Kong despite seeing a net sale from Mainland investors overnight via Southbound Stock Connect. All sectors were in the green except for healthcare as value sectors outpaced growth sectors.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.17%, -0.64%, and -1.83%, respectively, on volume that was +0.38% higher than yesterday, which is only 89% of the 1-year average as declining stocks outpaced advancing stocks by 3 to 2. It is interesting that the Mainland media noted that the national team was active today for the first time this year. There was chatter that the national team, Chinese institutional investors who buy on market dips, was active earlier this week though that appears to be false. For those of you saying, “that’s market manipulation!” “Free markets!” please take a look at the US Fed balance sheet. Ultimately, these entities are simply buying low as they hold a lot of stocks with a low long-term investment horizon. Foreign investors bought $710 million worth of Mainland stocks overnight via Northbound Stock Connect. Bonds and the currency were basically flat while copper gained +2.46%.

After the close, January New Loans data was RMB3.98 trillion versus expectations of 3.7 trillion and December’s 1.13 trillion. Aggregate Financing was 6.17 trillion versus expectations of 5.4 trillion and December’s 2.37 trillion. Obviously, December suffered from year-end seasonality though the data was stronger than anticipated. What’s happening? Banks are lending! Remember most of the world is tightening, which will lead to future headlines about homes sales, car sales, etc. slowing as interest rates rise.

We needed a new SUV recently. Can you believe what a Chevy Suburban costs these days? It's not a big deal when you finance at 0% though as rates go up, interest-free financing will go away. The opposite is occurring in China.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.36 versus 6.37 yesterday

- CNY/EUR 7.28 versus 7.28 yesterday

- Yield on 10-Year Government Bond 2.73% versus 2.73% yesterday

- Yield on 10-Year China Development Bank Bond 3.00% versus 2.97% yesterday

- Copper Price +2.46% overnight