Local Investors Less Pessimistic, Week in Review

3 Min. Read Time

Week in Review

- Last weekend was the start of China’s dual sessions, from which China's GDP growth target of 5.5% for 2022 was announced along with a slew of supportive economic policies.

- On Tuesday, declining stocks outpaced advancing stocks nearly 10 to 1 (3,987 decliners and only 408 advancing stocks).

- The market ignored a stealth monetary stimulus announcement on Wednesday as the PBOC moved RMB 1 trillion to the Ministry of Finance to support small, private companies.

- Thursday morning the SEC identified five US-listed ADRs including Yum China (YUMC US) and biotech company Beigene (BGNE US) for failing to comply with the Holding Foreign Companies Accountable Act (HFCAA).

Key News

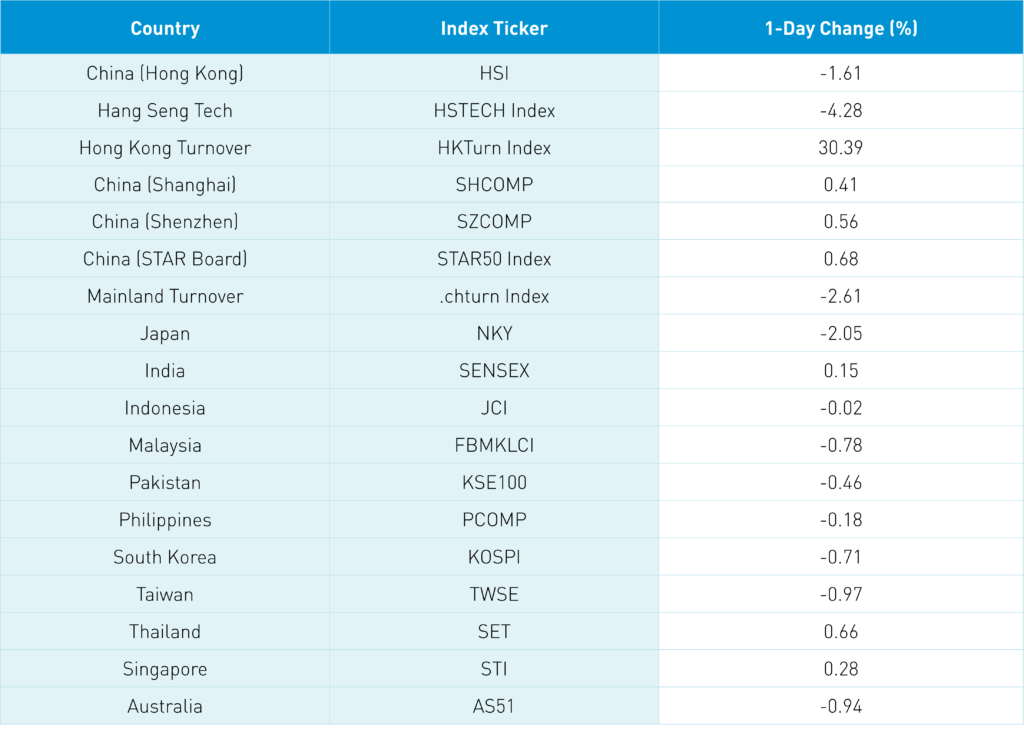

Asian equities had a mixed night with China, India, Singapore, and Thailand in the green. Japan, Hong Kong, Taiwan, South Korea, and SE Asia were down. "The Longest Day," the definitive book on World War Two’s D-Day, sums up how I felt yesterday.

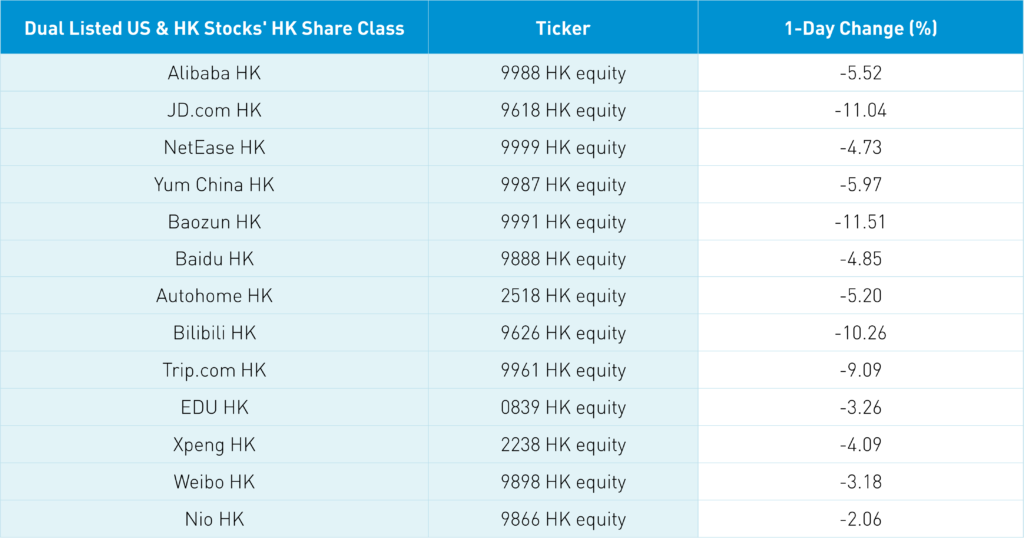

The SEC’s identification of five US-listed Chinese ADRs that would face delisting in 2024 due to the Holding Foreign Companies Accountable Act (HFCAA) sent the entire US-China ADR universe plummeting yesterday. Identifying companies is the first step in the SEC’s HFCAA enforcement. One should anticipate all US-listed Chinese ADRs will be identified as they submit their 2021 annual reports to the SEC. Investors were indiscriminate in their selling despite both Yum China (YUMC US) and Beigene (BGNE US) having Hong Kong share classes. Why would you sell their US ADRs when you can simply convert to the Hong Kong share class? That’s what we are doing. The reason is many investors are unaware of ADR conversion, their broker/custodian can’t convert or they simply don’t want to hold a Hong Kong stock.

Hong Kong investors were fairly less pessimistic as US-China ADRs were down -10% while the Hang Seng Tech Index was down -4.28%. YUMC and BGNE fell -10.94% and -5.87% yesterday though their Hong Kong shares fell -6.02% and -4.96%. This was true for internet stocks as JD.com’s US shares fell -15.83% versus HK’s -11.08%, Alibaba US fell -7.94% versus HK’s -5.56%, Baidu US -6.29% versus Baidu HK -4.9%.

Overnight Reuters is reporting that “sources” in China are reporting that a resolution is making progress. Former SEC Chair Jay Clayton had proposed a co-audit solution though there has been little talk of his solution since his departure. We also had the CSRC release a statement at nearly midnight China time saying that talks with the SEC were making progress. Hopefully, a solution avails itself but one shouldn’t take that risk in light of the delisting window likely being shortened from 2024 to 2023. We are migrating out of the US ADRs to the Hong Kong share classes.

Premier Li gave his annual speech at the end of the dual sessions political and economic meetings today. This was Premier Li’s last speech as he confirmed his retirement later this year having been in his current role since 2013. We have historically mentioned that China’s implied government official retirement age of 68 could lead to several changes at a high level in China’s government later this year at the party congress. In a nutshell, Premier Li said the 5.5% 2022 GDP target is ambitious but feasible. The economy will be supported by RMB 2.5 trillion of tax cuts and refunds with emphasis on assisting small companies. On Ukraine, he stated the hope for a peaceful resolution and for providing humanitarian aid to Ukraine.

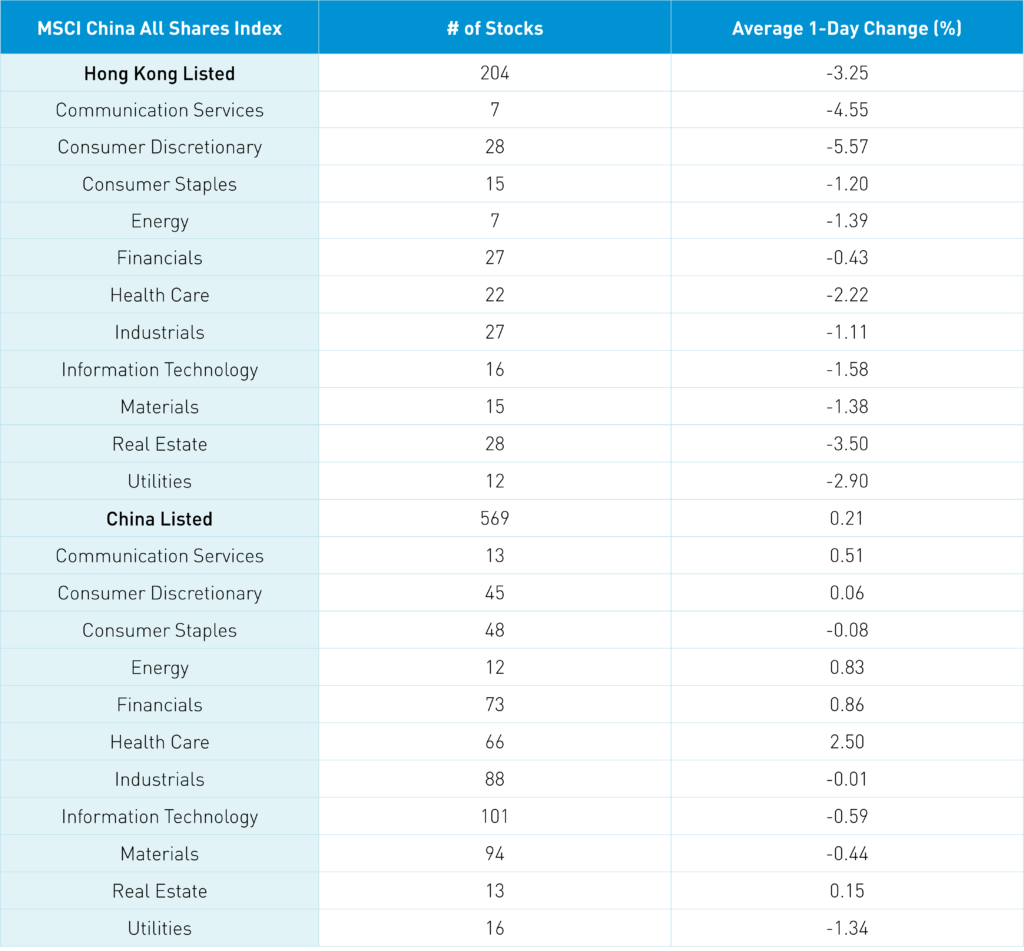

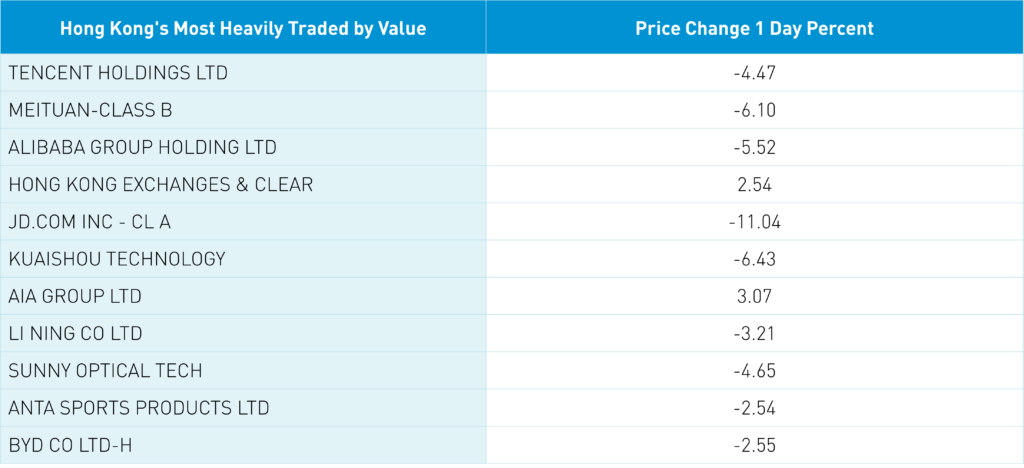

The Hang Seng Index was off -3.88% intra-day before an afternoon rally curtailed losses at -1.61% as volume surged +30% from yesterday, which is 128% of the 1-year average. Decliners outpaced advancers 3 to 1. All sectors were off with financials down the least as the Hong Kong Exchanges gained +2.54% as a beneficiary of the HFCAA. Tencent, Meituan, and Kuaishou were bought in size from Mainland investors via Southbound Stock Connect. Healthcare was weak due to three of the five stocks identified by the SEC happening to be biotech stocks.

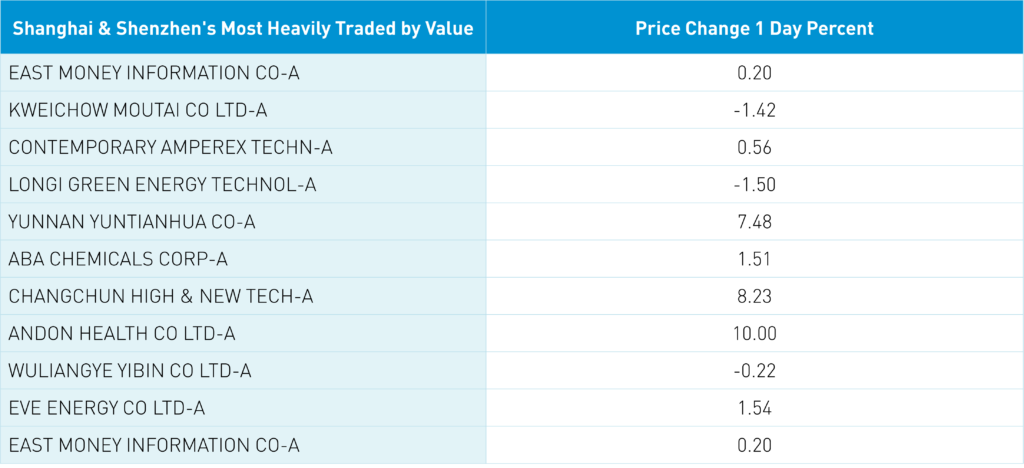

Shanghai, Shenzhen, and STAR Board also reversed off intra-day lows to close +0.41%, +0.56%, and +0.68% on volume -2.61% from yesterday, which is about the 1-year average. Advancers outpaced decliners nearly 2 to 1. Healthcare was the best sector as a Covid outbreak in both China and Hong Kong is flaring. Both Aggregate financing and new loan data was released coming in lower than anticipated due to a drop in real estate. The release is apt to reinforce the view that supportive policies need to be implemented to support the economy. Foreign investors sold Mainland stocks today to the tune of -$795mm which brings the weekly total to $5.745B. Chinese Treasury bonds rallied as CNY depreciated -0.18% versus the US $ and copper rallied.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.33 versus 6.32 yesterday

- CNY/EUR 6.97 versus 6.98 yesterday

- Yield on 10-Year China Government Bond 2.79% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.05% versus 3.13% yesterday

- Copper Price +0.39% overnight