Pinduoduo Harvests Profits in Agriculture Push

3 Min. Read Time

Key News

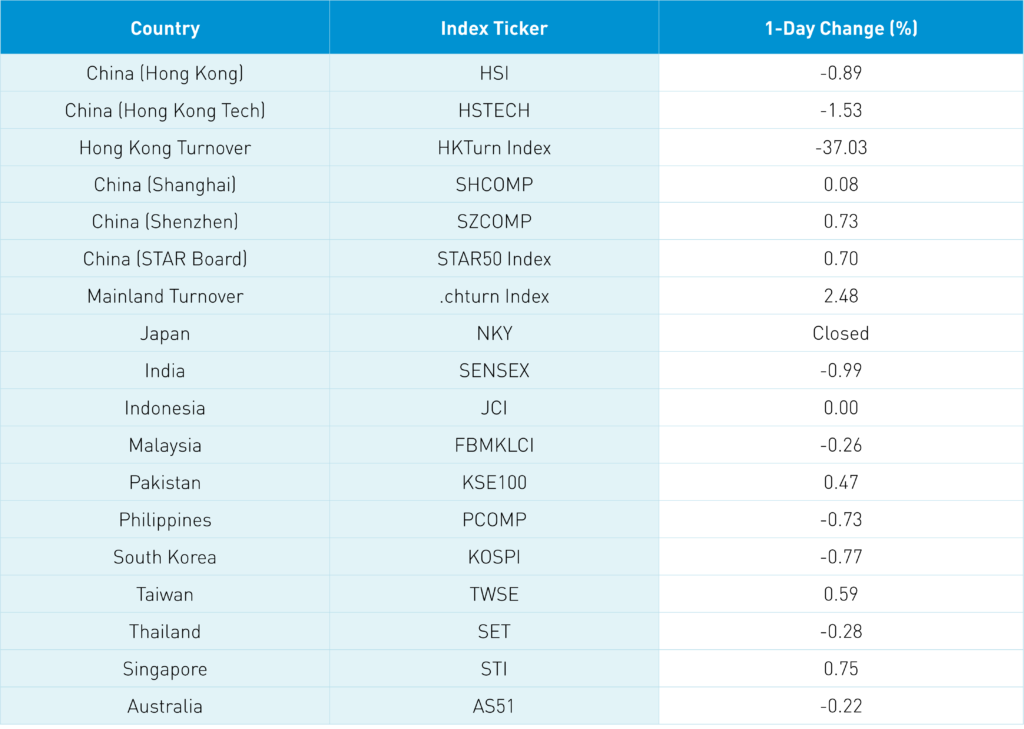

Asian equities were mixed overnight as equity markets in China, Taiwan, and Singapore gained while Hong Kong, India, and South Korea were off and Japan was closed. Volumes were off significantly from Friday’s FTSE Russell index rebalance as investors look for material policy following Vice Premier Liu He’s speech last week that sent markets soaring due to its optimism around internet regulation, covid policy, and delisting.

The People’s Bank of China (PBOC), China’s central bank, kept the 1 and 5-year loan prime rates (LPRs) unchanged at 3.7% and 4.6%, respectively, in line with expectations though some had hoped for a cut. The PBOC likely made its decision to keep the LPRs steady well in advance of Liu He’s speech. However, the lack of a further cut to the key lending rate was a slight let down for some, leading to some profit taking while some investors remain on the sidelines, waiting for a material increase in policy support. After the close it was reported that a State Council meeting attended by Premier Li was focused on new tax reductions and rebates.

Market sentiment may have been dampened by the terrible news of a Boeing airplane crash in southern China. Trading in Evergrande’s Hong Kong stock was halted pending an expected release from the company, leading to real estate weakness and further dampened sentiment.

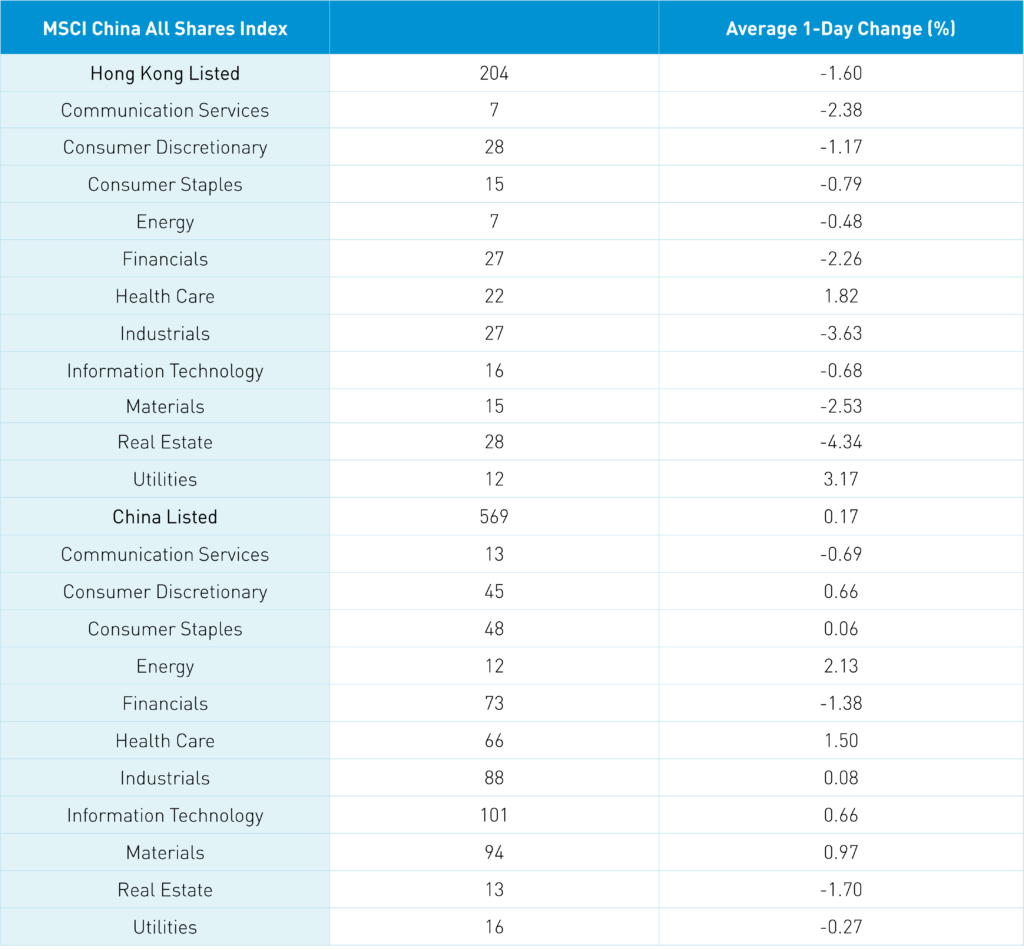

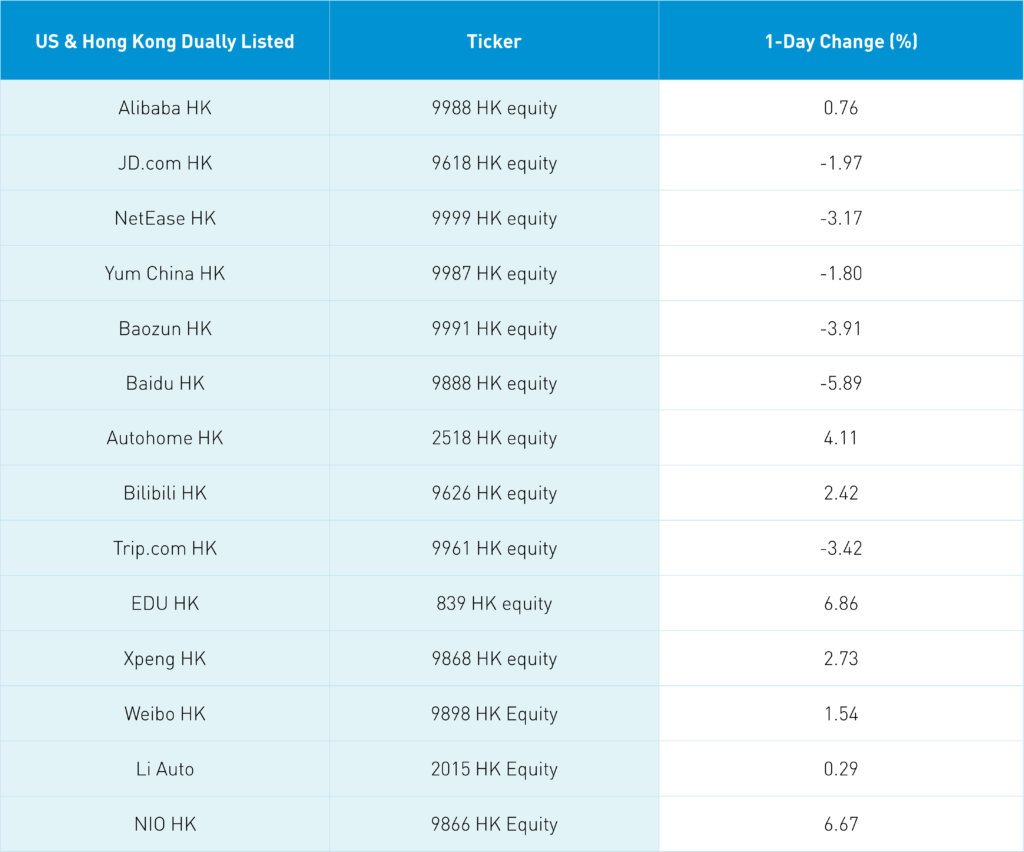

The Hang Seng Index was off -0.89% after opening +1.92% while the Hang Seng TECH Index was off -1.53% on volume that was -37.03% lower than Friday, which is just below the 1-year average, while decliners outpaced advancing stocks by 2 to 1. Hong Kong listed internet stocks did not match the strong performance of their US-listed ADRs on Friday, which was driven by Biden and Xi’s positive video call. The fact that the Hong Kong listings did not follow their US ADRs higher overnight may lead to a downdraft in the US ADRs today. However, Alibaba HK did manage a gain of +0.76% despite broad weakness in the space. Tencent and Meituan saw small net buying via Northbound Stock Connect.

Healthcare had a strong day as Hong Kong moves to dial back its draconian lockdown policy by allowing US flights and reducing the mandated quarantine time to seven days.

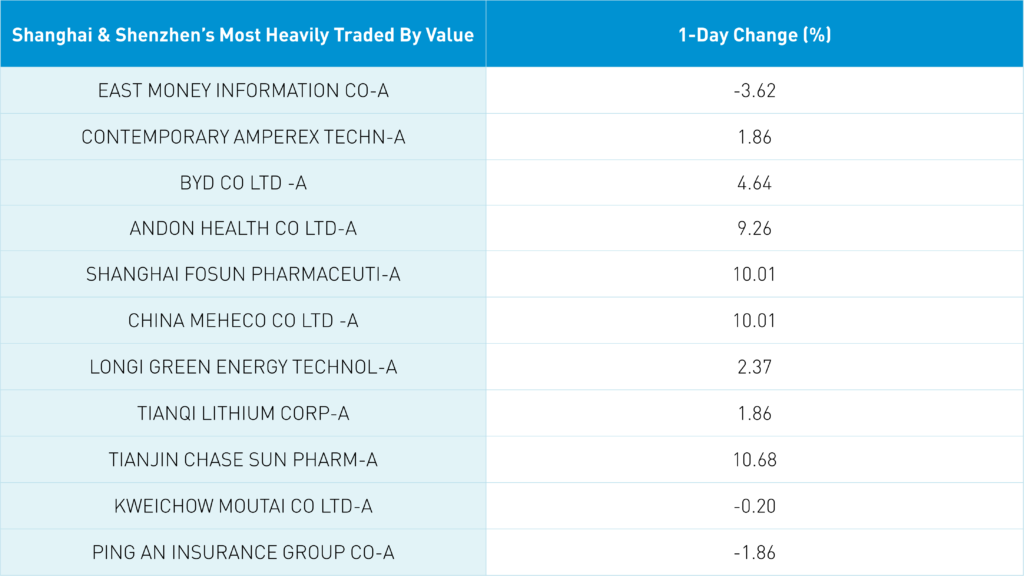

Shanghai gained +0.08%, Shenzhen gained +0.73%, and the STAR Board gained +0.7% on volumes that were +2.48% higher than Friday as advancers outpaced decliners by 2 to 1. Energy and healthcare were the leading sectors, gaining +2.13% and +1.5%, respectively, while financials were weak. Foreign investors flipped to net sellers of -$1.32 billion worth of Mainland equities via Northbound Stock Connect. Treasury bonds were weak while CNY gained versus the US dollar and copper gained +0.49%.

Pinduoduo Q4 Overview

E-commerce company Pinduoduo (PDD US) reported Q4 financial results after the Hong Kong close this morning. Revenue missed analyst expectations though net income and EPS beat significantly as the company controlled costs. I found the earnings call interesting as management focused on its efforts to bring agricultural goods to its clients while downplaying its past quarters of higher revenue growth. Expectations were not high going into the release due to macroeconomic headwinds for the E-Commerce industry. I thought management did not take enough credit for managing the company and controlling costs. There was no mention of Pinduoduo listing on the Hong Kong Stock Exchange, which is disappointing.

% changes are year over year i.e. Q4 2022 versus Q4 2021

- Revenues increased +3% to $4.273B (RMB 27.230B) from RMB 26.547 led by online marketing services increasing +19% to $3.519B (RMB 22.425B)

- Gross Merchandise Value increased 46% to $383B (RMB 2.441 trillion)

- Monthly active users increased 2% to 73.4mm from 719.9mm while active buyers increased +10% to 788.4mm

- Total cost of revenues -43% to $1.022.4B (RMB 6.515B) while total operating expenses declined to $2.166.8B (RMB 11.808B)

- Operating profit swung to a gain of $1.083B (RMB 6.907B) from a loss of RMB 2.047B while Adjusted profit (non-GAAP) $1.318B (RMB 8.399B)

- Adjusted Net Income $1.325B (RMB 8.444B) versus a loss of RMB -184.5mm and analyst expectations of RMB 2.973B

- Adjsuted EPS $0.92 (RMB 5.88) versus a EPS loss of RMB -0.15

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.35 versus 6.36 Friday

- CNY/EUR 7.01 versus 7.02 Friday

- Yield on 1-Day Government Bond 1.54% versus 1.49% Friday

- Yield on 10-Year Government Bond 2.81% versus 2.79% Friday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.05% Friday

- Copper Price +0.49% overnight