Markets Wait For PBOC, Internet Stocks Play Catch Up

3 Min. Read Time

| Upcoming Event: | Join us Thursday, April 28th for our virtual conference at 11:00 am PST (2:00 pm EST). KraneShares Bay Area Innovation Forum Click here to register. |

Key News

There was a strong storm in NYC last night. The wind howled like a hurricane, waking me up several times. My patchy sleep was similar to Asian markets, which were mixed overnight. Japan rebounded from yesterday’s decline, India took another hit, and Hong Kong returned from its four-day holiday with a thud. Hong Kong-listed internet stocks caught up following the recent dip in their US-listed ADR counterparts after being closed last Friday and Monday.

There were several negative “headlines” that did not appear worrisome to me though investors continue to act with a shoot first and ask questions later mentality. Yesterday’s announcement from Didi on delisting from the NYSE without pursuing a Hong Kong listing weighed on sentiment. There is chatter about delivery companies being told not to gouge Shanghai residents, though that is hardly surprising.

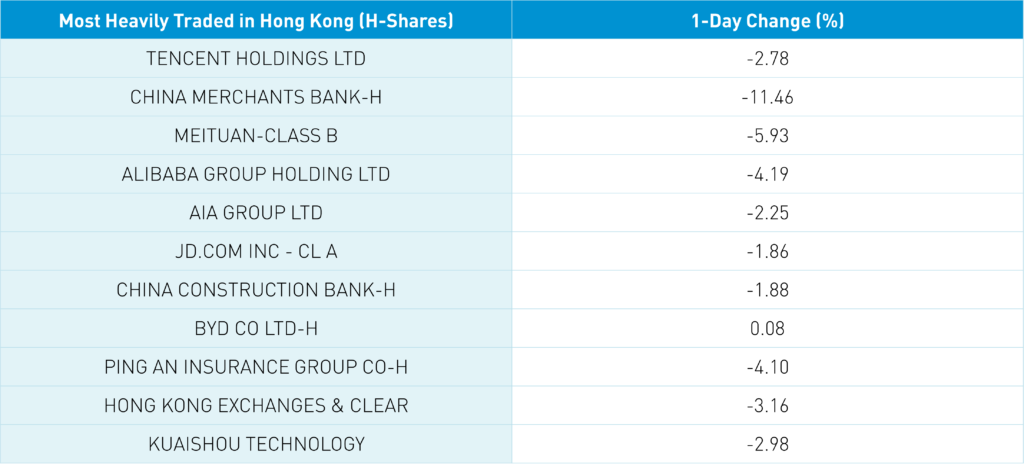

Bilibili’s Hong Kong listing was off -10.92% despite denying rumors that it is laying off employees. However, a follow-up examination of online video companies sent the subsector down. The China tech sector is under such an intense media microscope that any “announcement” is interpreted as the end of the world.

Against the backdrop of high commodity prices driving a value/growth rotation and the terrible situation in Ukraine, higher beta tech/growth stocks are taking the brunt of investor angst globally. A factor analysis confirms this view, as today in Hong Kong, dividends and value factors gained +2.02% and +1.85%, respectively, while growth and volatility were off -1.26% and -3.66%, respectively. A similar situation occurred overnight in Mainland China as the value sector gained +2.16% while growth and volatility factors were off -0.44% and -0.66%, respectively. While I understand the issue with holding higher duration and/or profitless tech stocks in a rising rate environment, many of the China internet stocks are hardly profitless compared to US internet/tech stocks and are trading at one-half the multiples of the latter, on average. Investors may have expected a more aggressive PBOC policy response though there is an argument for an incremental easing.

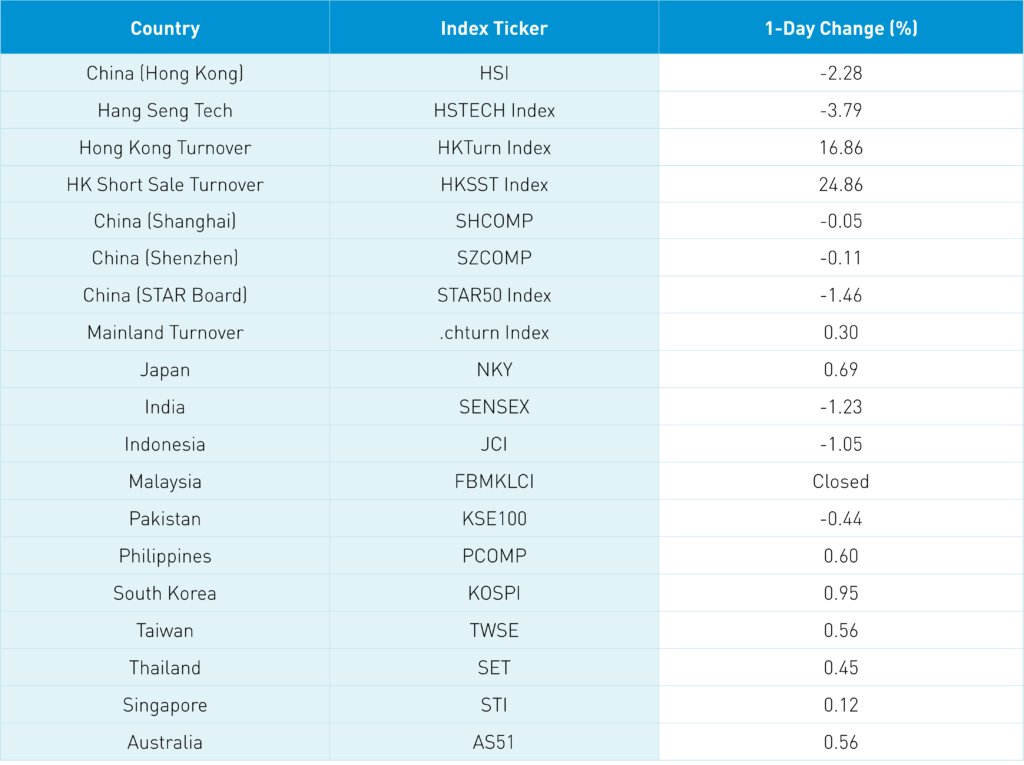

Shanghai, Shenzhen, and Hang Seng are sitting on support levels (i.e. big round numbers) of 3,200, 2,000, and 21,000, respectively, making the next several days key. Tonight, the new loan prime rate will be announced. Hong Kong short-sellers pressed their bets overnight amid above-average volume while total volume was light. This is a strong indication that buyers are looking for catalysts before stepping in. It certainly feels like peak pessimism, in my opinion.

The People’s Bank of China (PBOC) and State Administration of Foreign Exchange (SAFE) statements overnight on supporting the economy garnered little media attention, while Ant Group’s strategic partnership with Singapore mobile payment company 2C2P garnered even less. This means that the broad China market could be ripe for a rally as the market tends to do what is least expected.

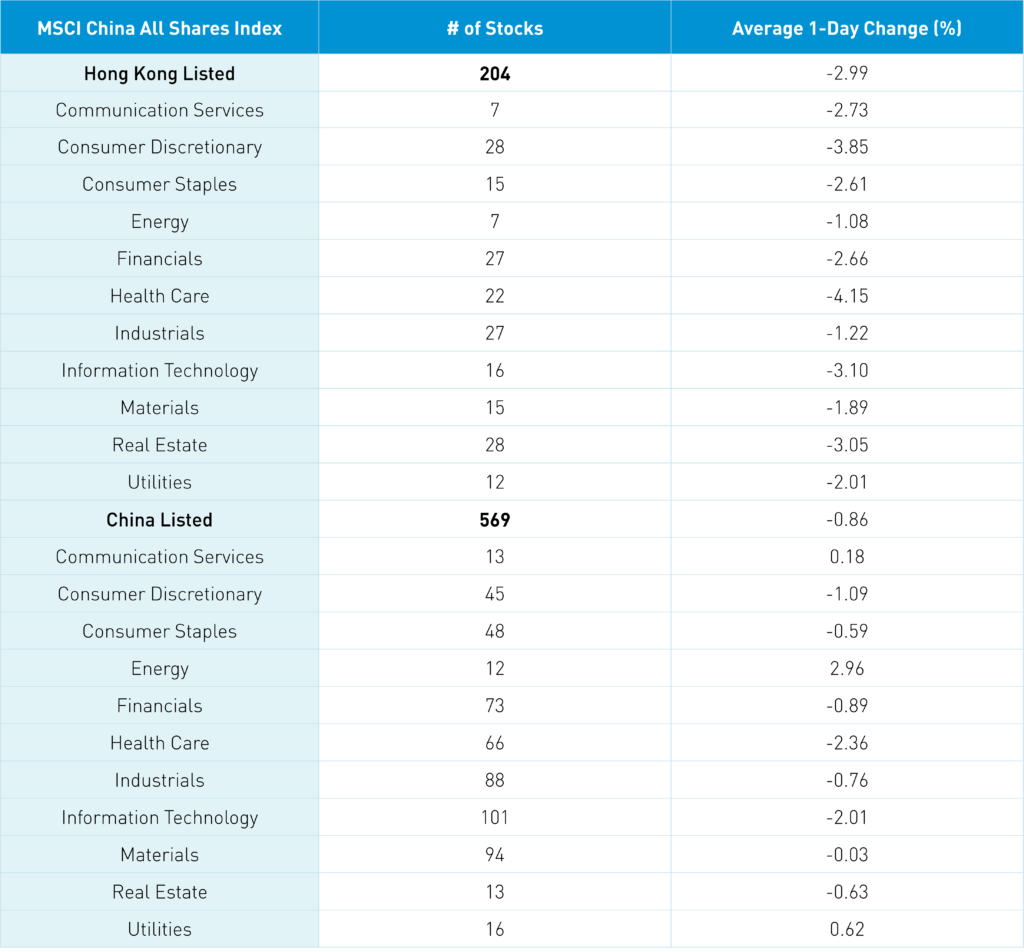

The Hang Seng Index was off -2.28%, led lower by tech/growth plays as the Hang Seng Tech fell -3.79% as volumes increased +16.86%, only 79% of the 1-year average. Decliners outpaced advancers by 4 to 1 as every sector was down. Healthcare was surprisingly the worst performer due to the covid outbreak in China, falling -4.13%. Mainland investors were net buyers of Hong Kong stocks today as Tencent and Meituan were net buys. Hong Kong's short sale volume was 108% of the 1-year average.

Shanghai, Shenzhen, and the STAR Board were off -0.05%, -0.11%, and -1.46%, respectively, as value stocks/sectors outperformed growth. Volumes were up +0.3% from yesterday, 72% of the 1-year average. There were 2,170 advancing stocks and 2,144 declining socks as energy gained +2.94%, led by coal and nuclear stocks, while healthcare fell -2.37% and tech fell -2.03%. Foreign investors sold a net $304 million worth of Mainland stocks via Northbound Stock Connect. The Treasury yield curve steepened slightly, CNY was off versus the US dollar, and copper gained +0.31%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.37 yesterday

- CNY/EUR 6.89 versus 6.88 yesterday

- Yield on 1-Day Government Bond 1.38% versus 1.40% yesterday

- Yield on 10-Year Government Bond 2.82% versus 2.81% yesterday

- Yield on 10-Year China Development Bank Bond 3.05% versus 3.04% yesterday

- Copper Price +0.31% overnight