Buyers Strike as CSRC Recommends Raising Equity Allocations

4 Min. Read Time

| Upcoming Event: |

| KraneShares Bay Area Innovation Forum Join us Thursday, April 28th for our virtual conference at 11:00 am PST (2:00 pm EST) Featuring 12th US ambassador to China, Terry Branstad Click here to register. |

Key News

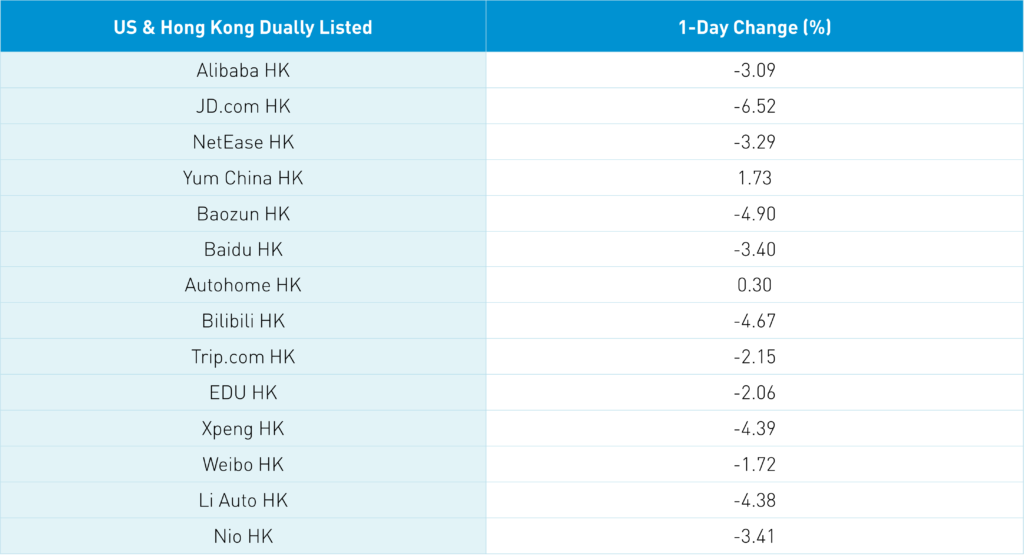

Asian equities had a mixed day as Japan and India rebounded while Hong Kong, China, and the Philippines were down/underperformed. Going into today’s session, we knew things would be off as US ADRs, and China ETFs were down yesterday during US trading hours. A global investment bank released a research piece yesterday afternoon noting the under-allocation to China and internet plays from active managers. Overnight the lack of buyers was as much of an issue as shorts pressing their bets. Hong Kong volumes were still only 83% of the 1-year average though short selling volume was 105% of the 1-year volume. The reasons range from China’s lockdown/quarantine response to covid, i.e., Shanghai, investors' expectations for stronger monetary easing as the PBOC prefers incremental easing, HFCAA/ADR delisting, and the broader US-China political relationship. Uncle! Today was one of the worst breadth (advancers versus decliner) days that I’ve ever seen. Post Tesla results, one would think Nio, Li, and Xpeng’s Hong Kong shares would have risen overnight though they were down.

There was little stock-specific news though a Bloomberg article noting shares outstanding in dual-listed stocks is picking up as US ADRs are converted to Hong Kong shares. The article misses one of the key points: companies are converting their Treasury stock (non-issued shares), management shares, and stock plans to the Hong Kong shares from the US shares as a precaution due to HFCAA. The evidence: low relative volumes in the Hong Kong shares versus the US shares. A Mainland broker called today’s price action “tragic” as domestic investors’ sentiment turns. This explains the post-close announcement that the CSRC held a meeting with “the principles of the National Council of Social Security Fund and some large banking and insurance institutions.” A key point was these investors should “increase the proportion of equity investment.” These investors tend to buy low so coming into the market makes sense. It was also announced that “person pension plans” would be launched with tax-deductible contributions. Details are scarce, but this sounds like IRA-like vehicles will be introduced. Bigger picture, we need action/catalysts such as a strong covid vaccine to prevent further lockdowns and a solution to the HFCAA.

According to a Mainland media source from the Boao Forum, Fang Xinghai, Vice Chairman of the CSRC, said that the audit and supervision issues between China and the United States are the core, and some arrangements need to be made. It's not easy to find a reasonable arrangement, but the teams of both sides have held discussions every week, and I believe this uncertainty will be eliminated soon.

Last Saturday, the period ended on removing the rule preventing PCAOB from doing onsite audit reviews. Where is the follow-up? Other factors include rising US interest rates and value/growth rotation. Overnight CNY weakened -0.48% to 6.45 from 6.41, driven by US and Chinese Treasury yields are now the same (US 10 Year 2.87% versus China 10 Year 2.82%). Net-net, today’s crisis in confidence, shall too pass.

Significant chatter on Didi this morning as early headlines said Didi’s regulatory probe results would be delayed, followed by news regulators though its penalty was too late. A penalty might mean that the company has paid for its sins. The company has proposed a delisting vote on May 23rd with Didi executives’ shares allowing them to control the fate. A move to the pink sheets could be interesting as most investors would be shocked at how well Luckin Coffee did once it went to the pink sheets.

Charlie Munger has gotten a lot of grief for his purchase of Alibaba. What the Twittersphere misses is his time frame. Berkshire Hathaway bought BYD back in 2009. It did NOTHING for a decade before investors understood the EV opportunity. He’s an investor and not a trader with a time horizon, a key differentiator.

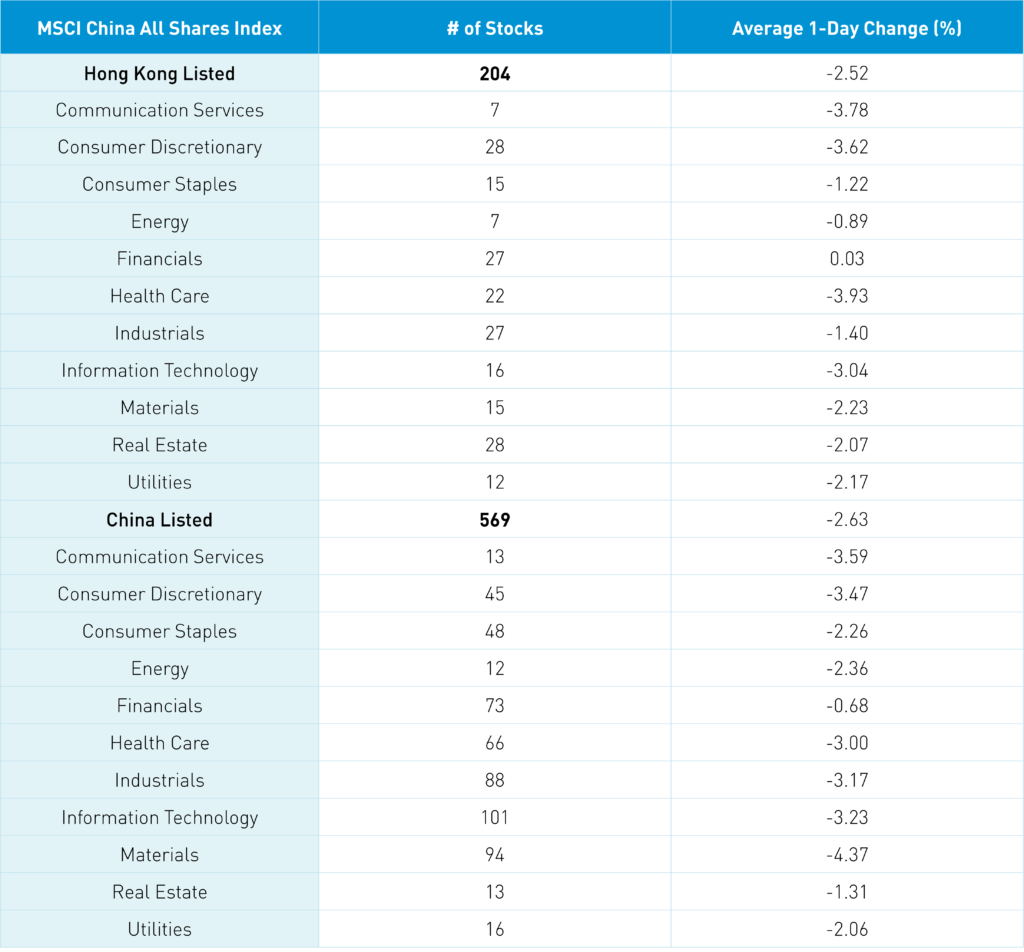

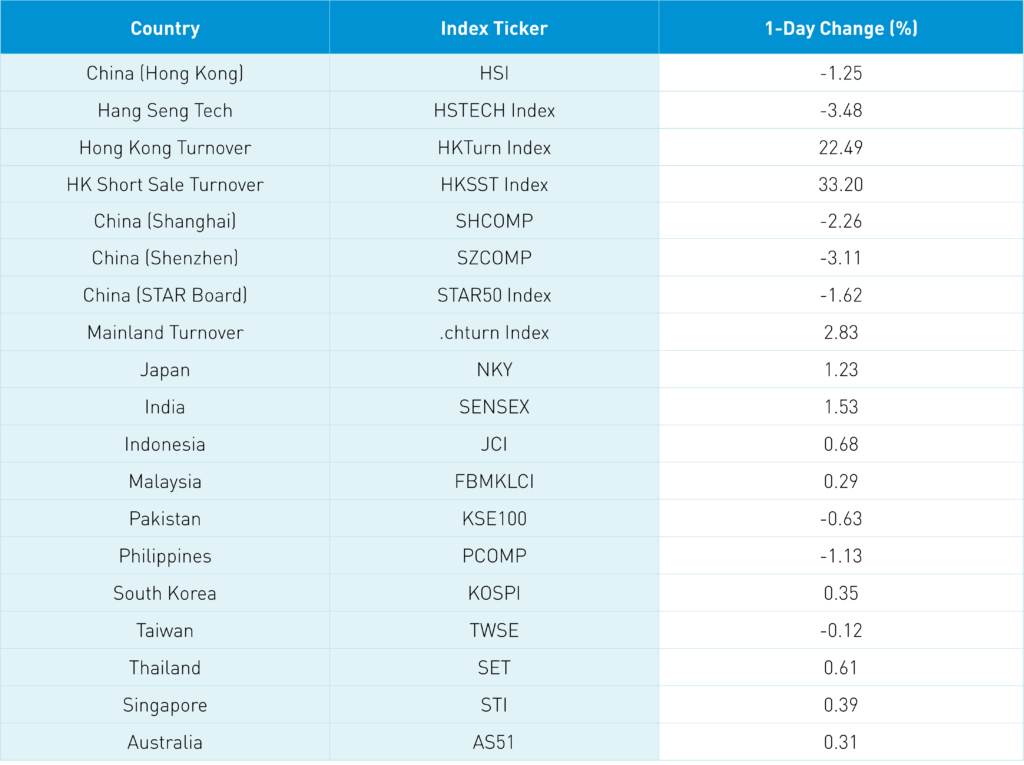

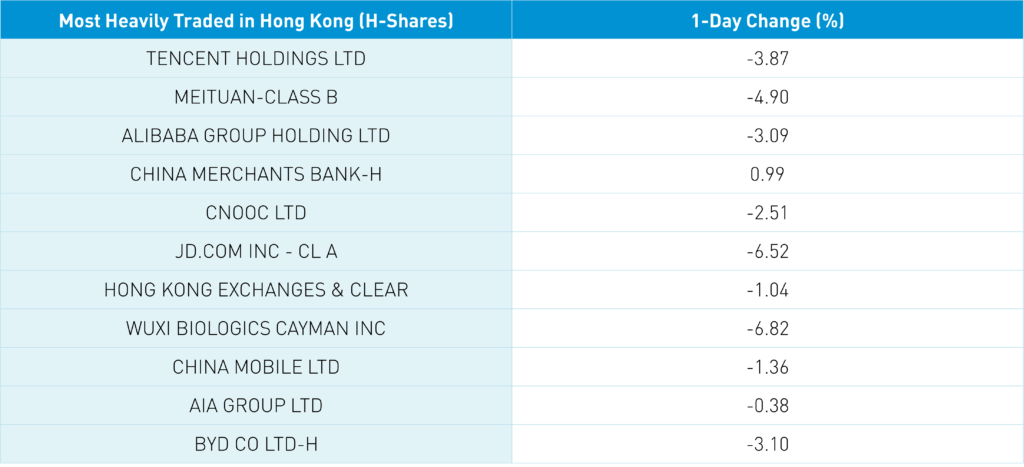

The Hang Seng Index and Hang Seng Tech Index lost -1.25% and -3.48% on volume +22.49% from yesterday, 83% of the 1-year average. There were only 64 advancers versus 426 advancing stocks as financials was the only sector in the green +0.03%. Hong Kong's short-selling volume increased 33% from yesterday, 105% of the 1-year average. Tech/growth sectors were off led by healthcare -3.93%, communication 03.79%, discretionary -3.62% and tech -3.05%. Growth and volatility factors were the worst performers today as dividends and value held up better. Mainland investors were a net seller of Hong Kong stocks today though Meituan managed a strong net inflow day.

Shanghai, Shenzhen, and STAR Board lost -2.26%, -3.11%, and -1.62% on volume +2.83% from yesterday, 78% of the 1-year average. Breadth had just 317 advancing stocks and 4,106 declining stocks. Every sector was down, with financials down the least -0.69% while materials -4.38%. Dividends and value were the best-performing factors while volatility was the worst, with growth factors off. Foreign investors were net buyers of Mainland stocks via Northbound Stock Connect to the tune of $141mm. Treasury bonds rallied, CNY was off -0.48% versus the US $, and copper was off -0.05%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.45 versus 6.41 yesterday

- CNY/EUR 7.02 versus 6.96 yesterday

- Yield on 10-Year Government Bond 2.83% versus 2.83% yesterday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.07% yesterday

- Copper Price -0.05% overnight