Internet Regulation Cycle Eases as Domestic Consumption Becomes Job #1, Week in Review

3 Min. Read Time

Week in Review

- Asian equities registered another choppy week of trading, mirroring US and developed markets. Markets were deepest in the red on Monday as investors feared a potential lockdown in Beijing.

- Multiple positive statements from the People’s Bank of China (PBOC), China’s central bank, and the State Council on the platform economy and real estate led to some minor equity rallies throughout the week.

- Several large cap A shares names reported positive Q1 earnings on Wednesday as earnings season kicked off in Mainland China.

- On Thursday, Baidu received official permission to offer completely driverless taxi rides in Beijing through its Apollo Go program. Previously, the company’s autonomous vehicles required emergency safety drivers.

Friday’s Key News

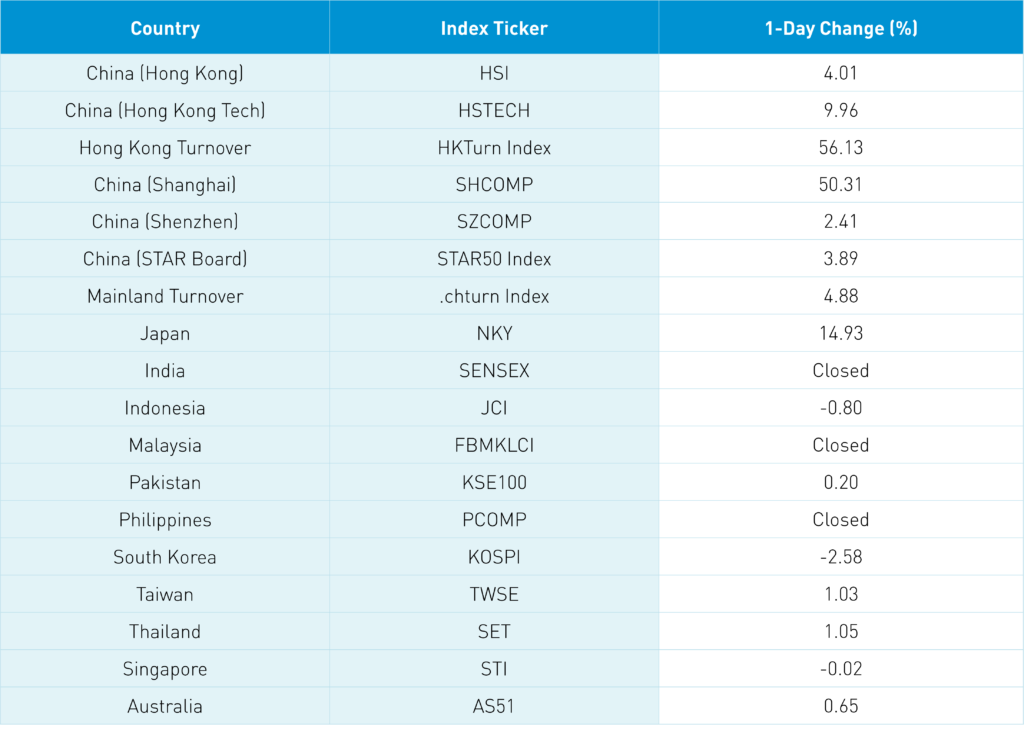

Asian equities had a strong day except for India and the Philippines as Mainland China and Hong Kong both outperformed.

Both Mainland China and Hong Kong were down in the morning session but ripped in the early afternoon following a release from the CPC Central Committee, which was presided over by President Xi. Specific to internet stocks, the release stated that “It is necessary to promote the healthy development of the platform economy, complete the special rectification of the platform economy, implement normalized supervision, and introduce specific measures to support the standardized and healthy development of the platform economy.” The interpretation is that this marks the end or, at least, a significant easing of internet regulation.

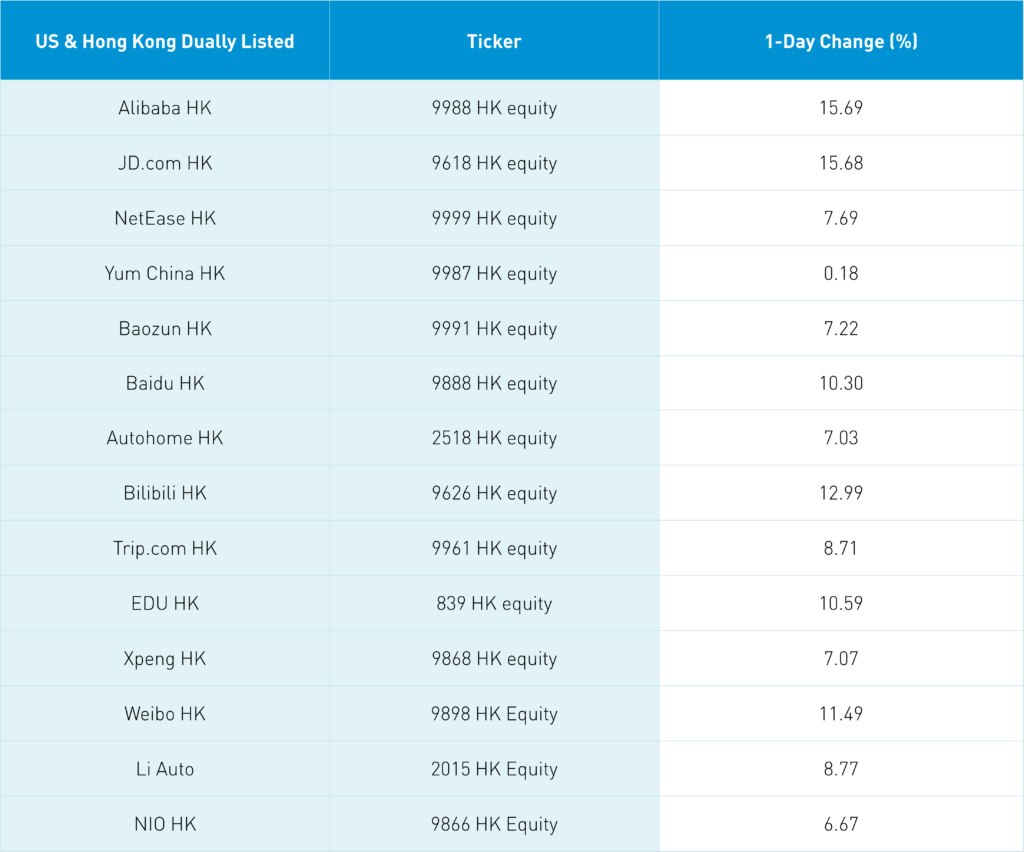

Hong Kong’s most heavily traded stocks were Tencent, which gained +11.07%, Meituan, which gained +15.51%, Alibaba HK, which gained +15.69%, JD.com HK, which gained +15.68, and Kuaishou, which gained +8.98%. Hong Kong volumes increased +56% from yesterday, showing strong investor participation in the rally. Was there short covering? 100%. Hong Kong short turnover increased +50% from yesterday, which is 161% of the 1-year average. Southbound Stock Connect was closed so today’s move was without the participation of Mainland investors.

After the Hong Kong close, Bloomberg News reported that “according to people familiar with the matter,” China is close to allowing the Public Company Accounting Oversight Board (PCAOB) to perform onsite audit reviews in China, which would eliminate the potential for ADR delisting presented by Holding Foreign Companies Accountable Act (HFCAA). Let’s hope so!

The South China Morning Post stated that regulators will meet with internet companies next week in an effort to prioritize domestic consumption. We have repeatedly pointed out the necessity for domestic consumption to pick up. Furthermore, one third of all retail sales go through internet companies. It makes sense to alleviate regulatory pressure as the transmission engines for domestic consumption are needed to jump start the economy.

It was a very strong and broad move in both China and Hong Kong. The CPC meeting was held to “analyze and study the current economic situation and economic work”. It acknowledged that the impacts of both covid and the Ukraine crisis “have led to increased risks and challenges,” while reiterating “people first, life first.” It seemed to indicate a balance “to efficiently coordinate epidemic prevention and control and economic and social development”. To stabilize the economy, it was recommended to “implement policies such as tax rebates, tax reduction and fee reductions, and make good use of various monetary policy tools.” This should be done “quickly” while emphasizing “the leading role of consumption in the economic cycle.” It reiterated that “houses are for living in, not for speculation” but also the need to “support localities to improve real estate policies based on local condition and promote the stable and healthy development of the real estate market.” We often view China as a singular entity though it is a diverse country not only geographically, but also economically. Not all Chinese cities have high real estate prices. Allowing flexibility on policies at the local level makes sense.

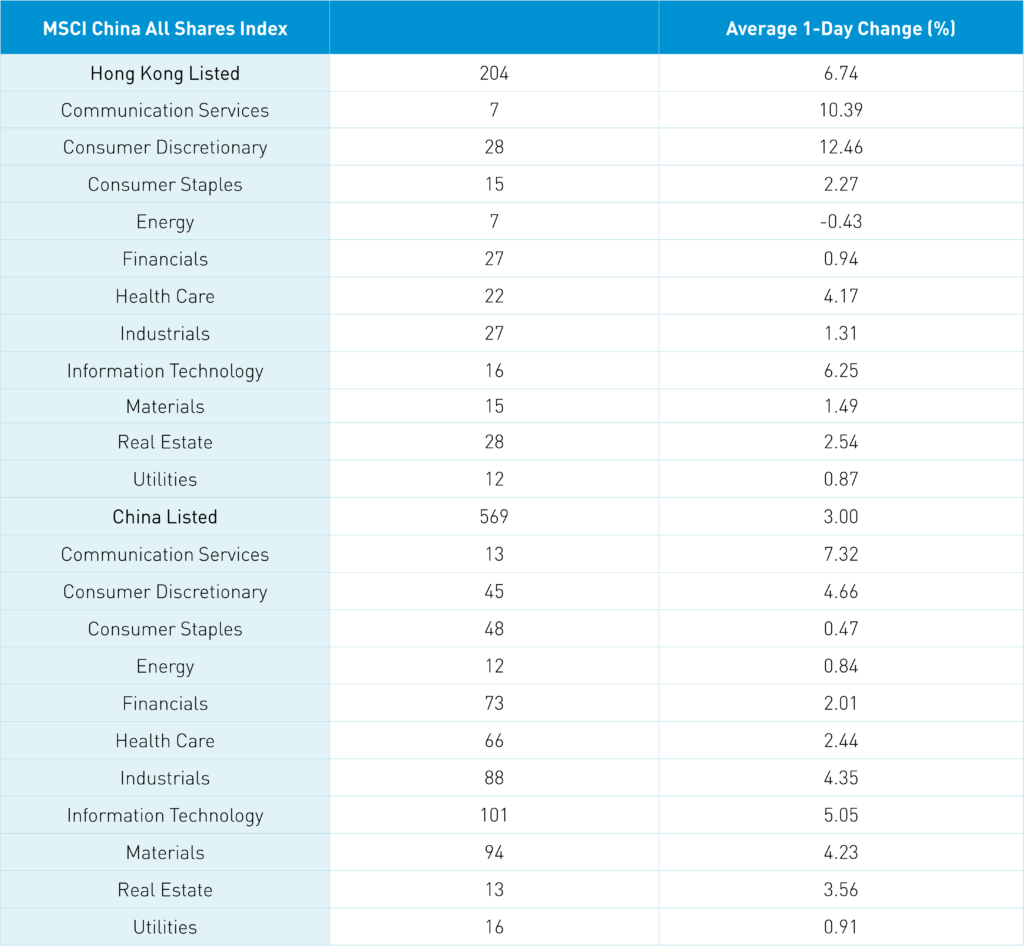

The Hang Seng Index and Hang Seng Tech Index closed +4.01% and +9.96%, respectively, on volume that was +56% higher than yesterday, which is 114% of the 1-year average. There were 393 advancing stocks and just 98 declining stocks. Hong Kong short sale volume rose +50%, which is 161% of the 1-year average. Leading sectors were discretionary, which gained +12.47%, communication, which gained +10.39%, and tech, which gained +6.26% while energy was the only off sector, down -0.43%. Growth factors outperformed while value sectors underperformed today. Southbound Stock Connect was closed due to Monday’s holiday.

Shanghai, Shenzhen, and the STAR Board gained +2.41%, +3.89%, and 4.88% on volume which was +14.93%, which is 89% of the 1-year average. There were 4,238 advancing stocks and just 218 declining stocks. Leading sectors were communication, which gained +7.26%, tech, which gained +4.99%, discretionary, which gained +4.61%, industrials, which gained +4.29%, and materials, which gained +4.17% as all sectors were positive. Growth factors outperformed value and dividend factors. Foreign investors bought $644 million worth of Mainland stocks today via Northbound Stock Connect. Treasury bonds gained, CNY gained +0.63% versus the US dollar, and copper gained +0.16%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.60 versus 6.63 yesterday

- CNY/EUR 6.96 versus 6.97 yesterday

- Yield on 1-Day Government Bond 1.59% versus 1.32% yesterday

- Yield on 10-Year Government Bond 2.84% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.07% versus 3.07% yesterday

- Copper Price +0.16% overnight