JD and Alibaba Lead Internet Rally, PBOC Accepts Ant’s Financial Holding Company Application, Week in Review

4 Min. Read Time

Week in Review

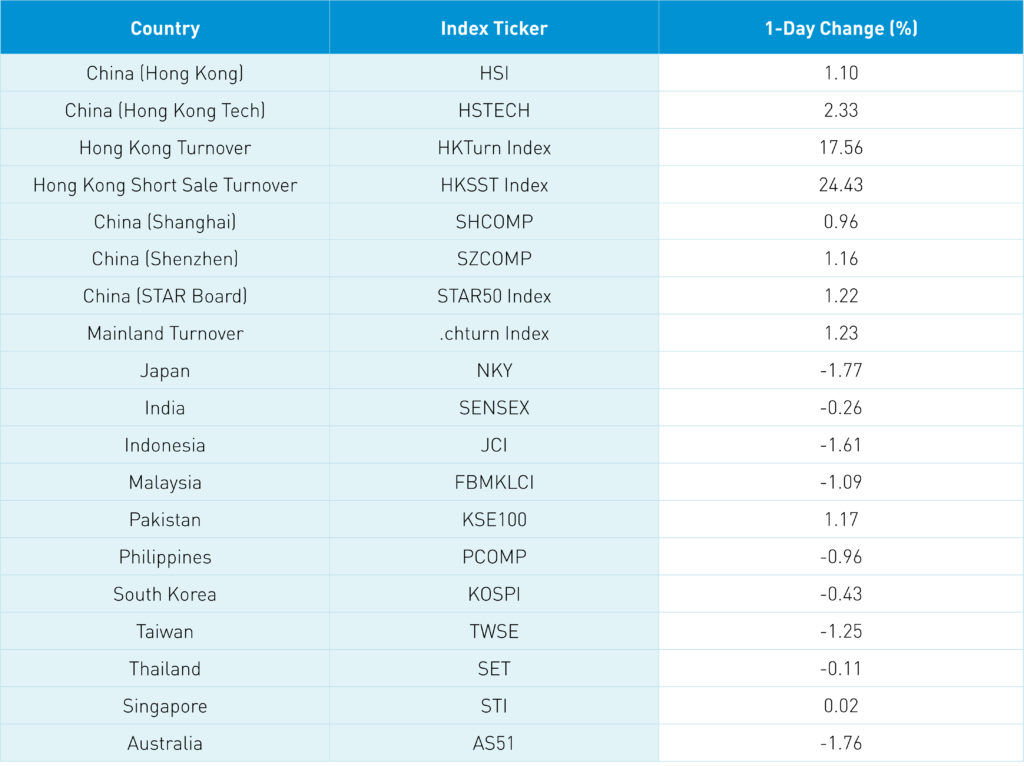

- Hong Kong and Mainland China were the only markets in Asia with positive performance for the week.

- Southbound Stock Connect volumes were elevated on Monday as Mainland investors snapped up shares in Tencent, Meituan, and Li Auto, among other growth names, amid renewed enthusiasm for tech shares and positive preliminary sales during the 6/18 shopping festival.

- The People’s Bank of China (PBOC), China’s central bank, refrained from instituting a cut to the medium-term lending facility rate, which was expected on Wednesday.

- China released a handful of better-than-expected economic indicators on Wednesday, including a slight uptick in retail sales.

- Asian equities were clipped on Thursday as the Swiss National Bank raised interest rates by 50 basis points, which sent risk assets lower across the globe. The Swiss bank’s move followed the US Fed’s announcement of a 75 basis point rate hike, the highest since 1994.

Friday’s Key News

Asian equities were largely lower, except for Hong Kong and Mainland China, which posted nice gains despite yesterday’s US equity meltdown. Hong Kong and Mainland China were the only Asian equity markets with positive performance for the week. They might end up being the only markets globally to end the week with positive performance as Europe and the Americas were hit. Remember that China is easing while central banks globally are largely tightening.

Reuters reported that, according to “sources,” the People’s Bank of China (PBOC) has accepted Ant Group’s application to become a financial holding company, which could pave the way for an IPO. Alibaba’s 1/3rd ownership of the fintech giant makes it a big beneficiary. If you believe that Ant’s pulled IPO marked the beginning of China’s internet regulation cycle, today’s news could be taken as a sign of its end. The key is that the Ant news came out after the close in Hong Kong such that US-listed China ADRs were going to have a good day today regardless of the Ant news.

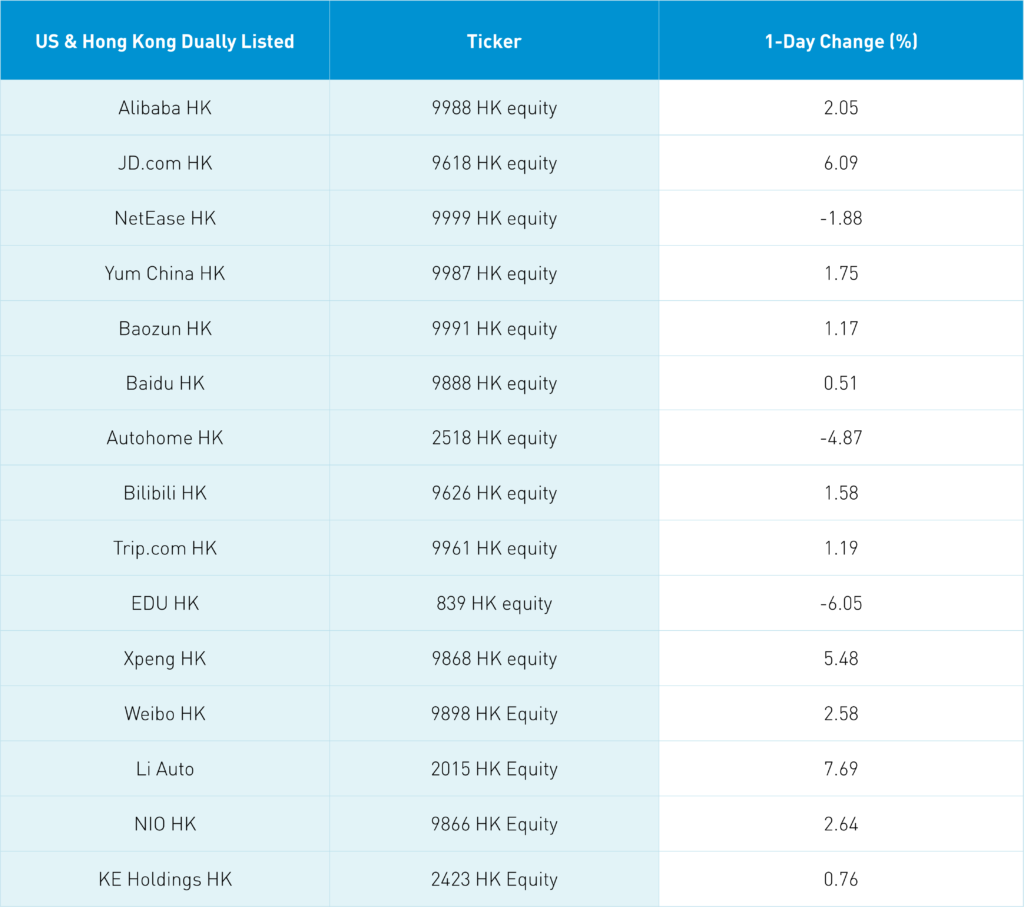

Hong Kong’s most heavily traded stocks by value were JD.com, which gained +6.09%, Alibaba HK, which gained +2.05%, Meituan, which gained +5.23%, and Tencent, which gained +0.49%. As previously mentioned, the preliminary 618 e-commerce sales event figures look strong.

Hong Kong’s rally was on strong volume that came in at 131% of the 1-year average. FTSE Russell and S&P indices rebalance today and we will have Quad Witching in the US, both of which could have contributed to the high volumes in Asia. Also, some below-the-radar US/China discussions appear to be taking place, which may have contributed to positive sentiment.

Hong Kong's short sale volume did increase, so we have a battle between the longs and the shorts shaping up. I favor the longs as we are headed into month/quarter-end and professional investors that are underweight the space may need to “window dress” i.e. add the stocks to their portfolios prior to disclosing their holdings to investors.

Online education stocks were hit with profit-taking in both Hong Kong and Mainland China after their recent strong move higher.

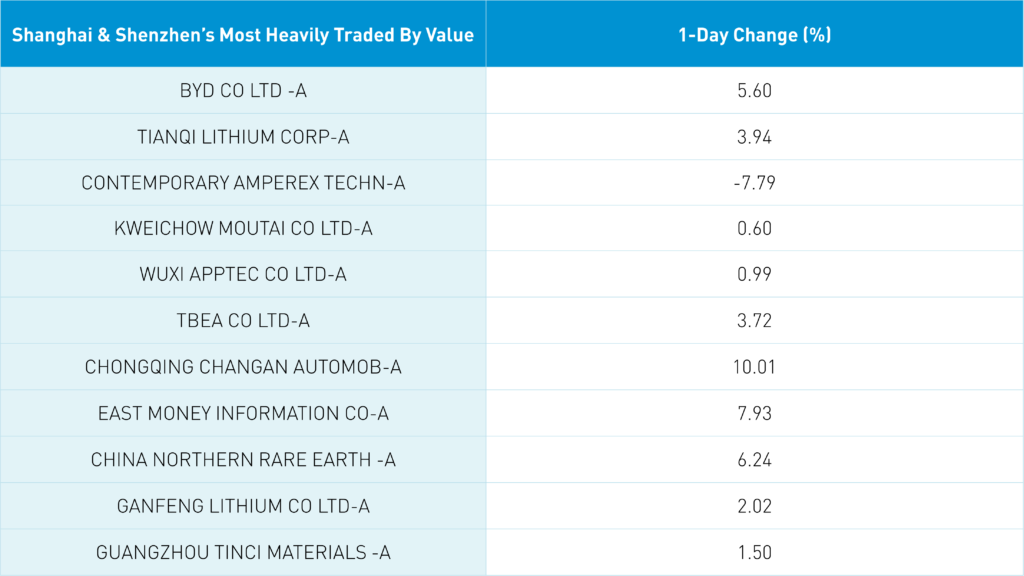

Mainland China had a strong day and was also led by growth stocks, especially lithium-related and electric vehicle (EV) battery-related stocks, including today’s most heavily traded stock by value, CATL, which gained +5.6% on news that it will be rolling out a new battery. Out of the top 35 most heavily traded stocks by value in China, only one was down!

Foreign investors bought a healthy $1.37 billion worth of Mainland stocks today, which brings the weekly total to a net inflow of $2.6 billion. Mainland volumes have been strong, over RMB 1 trillion in 9 out of the last 10 trading days. Shanghai (+3,300), Shenzhen (+2,100), and the Hang Seng (+21,000) closed above big round numbers. These numbers do not mean anything, but our brains make them feel important, so they are worth noting.

Yesterday, Yicai Global reported that Air China is resuming flights to the US, Europe, and Asia. This is a potential sign that zero covid/lives-first policies are being loosened.

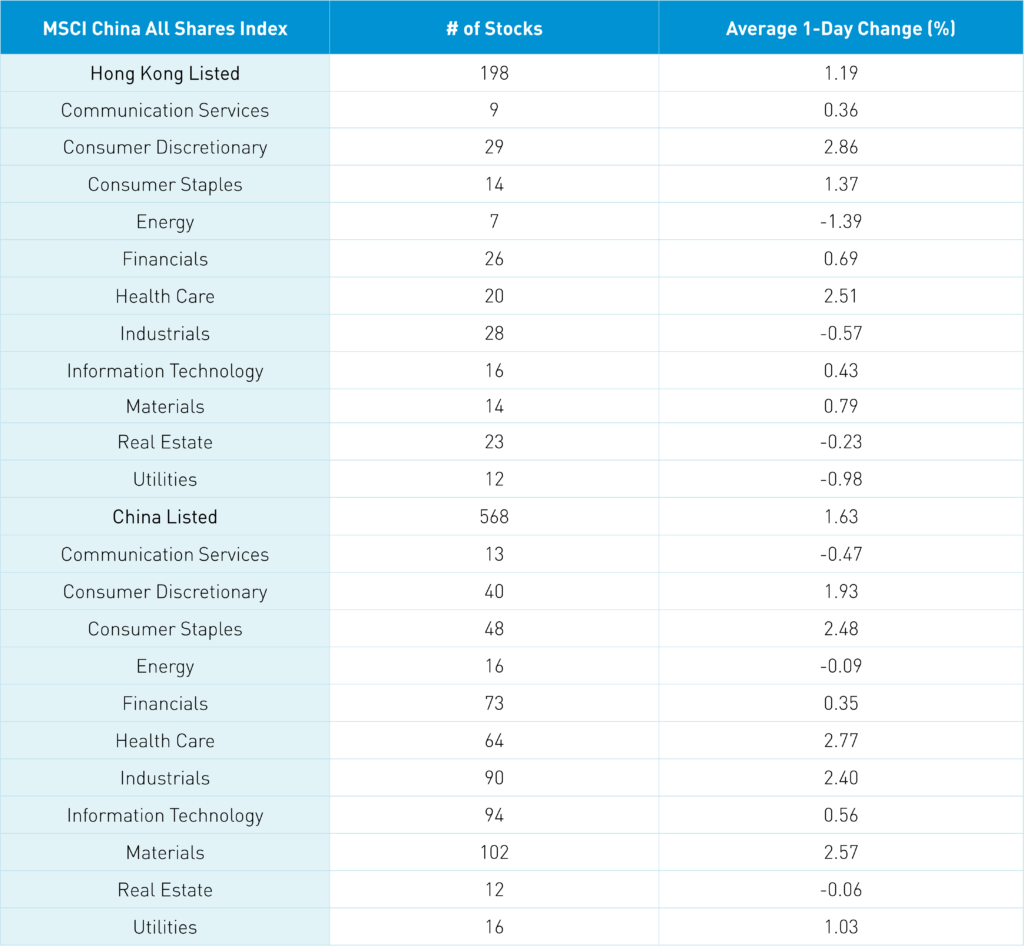

The Hang Seng and Hang Seng Tech indexes gained +1.1% and +2.33%, respectively, on volume that was +17.56% higher than yesterday, which is 131% of the 1-year average. 246 stocks advanced while 233 declined. Hong Kong short sale volume increased +24.42% from yesterday, which is 146% of the 1-year average. Growth factors outperformed value and dividend factors, while small caps outperformed large caps. The top sectors were consumer discretionary, which gained +2.86%, healthcare, which gained +2.51%, and consumer staples, which gained +1.37%. Meanwhile, energy fell -1.39%, utilities fell -0.98%, and industrials fell -0.57%. Top sub-sectors were cobalt and internet while online education was the worst performer. Southbound Stock Connect volumes were moderate/high as Mainland investors bought Hong Kong stocks. Kuaishou was a small net buy via Southbound Stock Connect, while Tencent and Meituan were small net sales.

Shanghai, Shenzhen, and the STAR Board gained +0.96%, +1.16%, and +1.22%, respectively, on volume that was +1.23% higher than yesterday, which is 102% of the 1-year average. 1,916 stocks advanced while 2,458 stocks declined. Growth factors outperformed value factors today, while large caps outperformed small caps by a small amount. The top sectors were healthcare, which gained +2.76%, materials, which gained +2.56%, staples, which gained +2.47%, and industrials, which gained +2.4%. Meanwhile, communication fell -0.48%, energy fell -0.1%, and real estate fell -0.07%. The top sub-sectors were lithium and battery-related stocks, while online education was a laggard. Northbound Stock Connect volumes were moderate as foreign investors bought $1.37 billion worth of Mainland stocks today. Treasury bonds were flat, CNY appreciated slightly versus the US dollar, and copper was smoked, falling -1.65% in price.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.71 versus 6.70 yesterday

- CNY/EUR 7.03 versus 7.05 yesterday

- Yield on 1-Day Government Bond 1.18% versus 1.18% yesterday

- Yield on 10-Year Government Bond 2.78% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 2.98% versus 2.98% yesterday

- Copper Price -1.65% overnight