Hong Kong Short Sellers Press Their Bets, Week in Review

4 Min. Read Time

Week in Review

- It has been a difficult week for markets globally as the US and Asia saw sharp equity declines on recession fears in the US and a higher-than-expected inflation print in the US of over 9%, the highest in 40 years.

- China released credit data for June that beat expectations, demonstrating the extent of China’s dovish monetary stance.

- A historic moment for electric vehicle maker BYD occurred on Tuesday as Warren Buffet sold his stake in the company for $9 billion after buying 225 million shares for $230 million in 2008.

- Growth and internet stocks were bright spots in China on Wednesday and Thursday following the approval of 67 new video games.

Key News

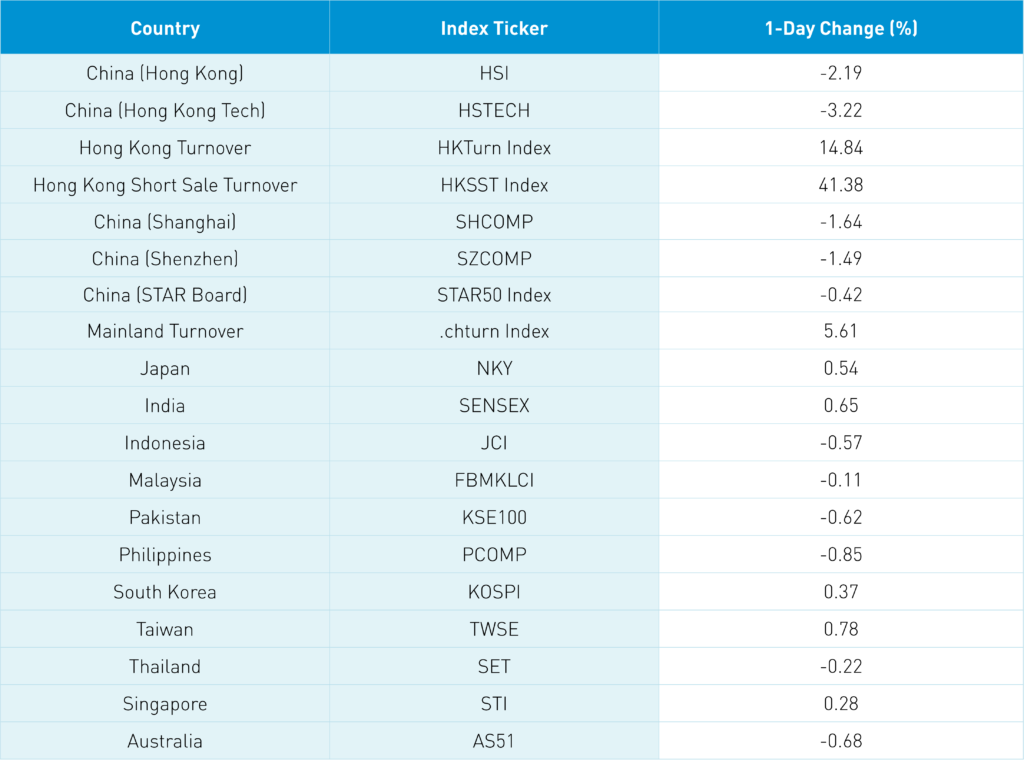

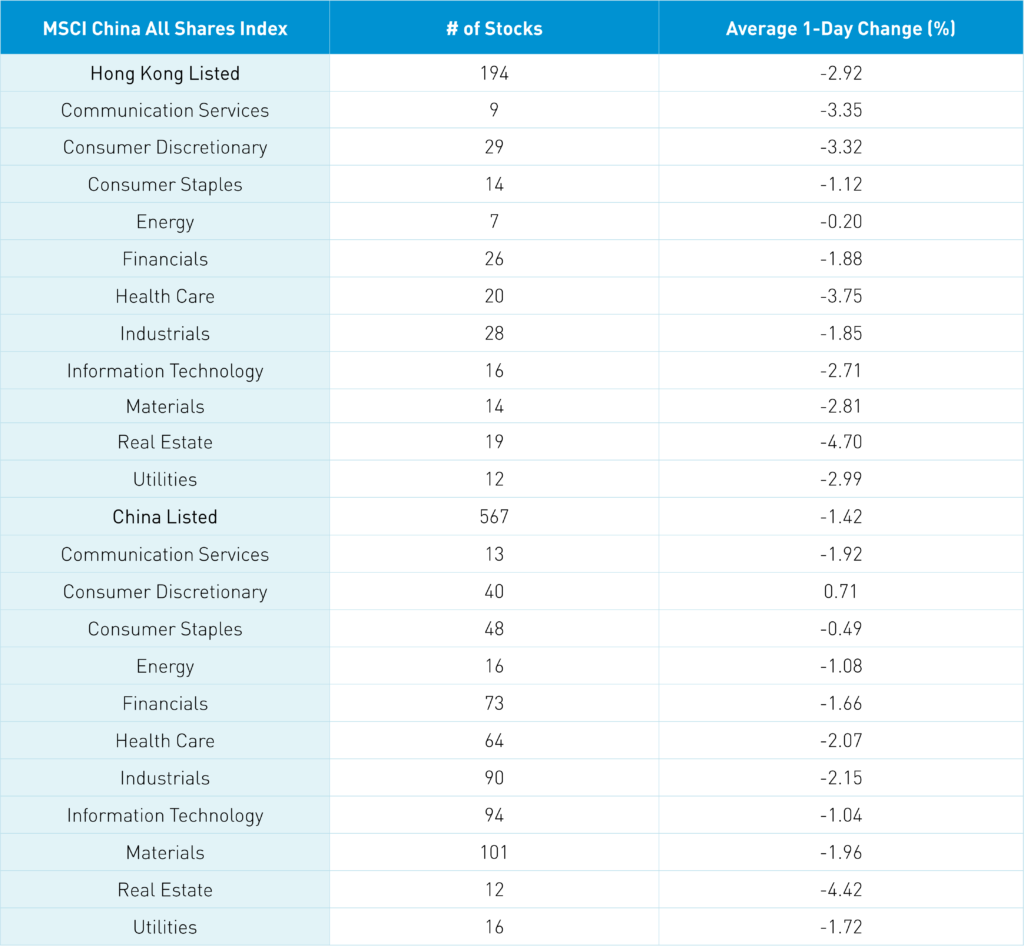

Asian equity markets ended an off week lower though Taiwan and India bucked the trend with positive performance overnight. Both Mainland China and Hong Kong markets were off as real estate was the worst performer in both markets, falling -4.7% in Hong Kong and -4.42% in Mainland China.

Concerns about apartment buyers waiting for their home purchases to be constructed not paying their mortgages was big news in Chinese social media. This weighed on China’s performance today. The culprit is property developer Evergrande, which is clearly not moving quickly enough to finish the projects it started due to its continuing financial difficulties.

The government’s response is going to give Evergrande and other property developers who are building slowly a swift kick in the pants. Who can blame the apartment buyers for not paying for a good that has yet to be delivered? I anticipate zero sympathy from the government on this issue. However, I do not believe this will be a significant problem though it has weighed on real estate and bank stocks in addition to overall sentiment on the Mainland.

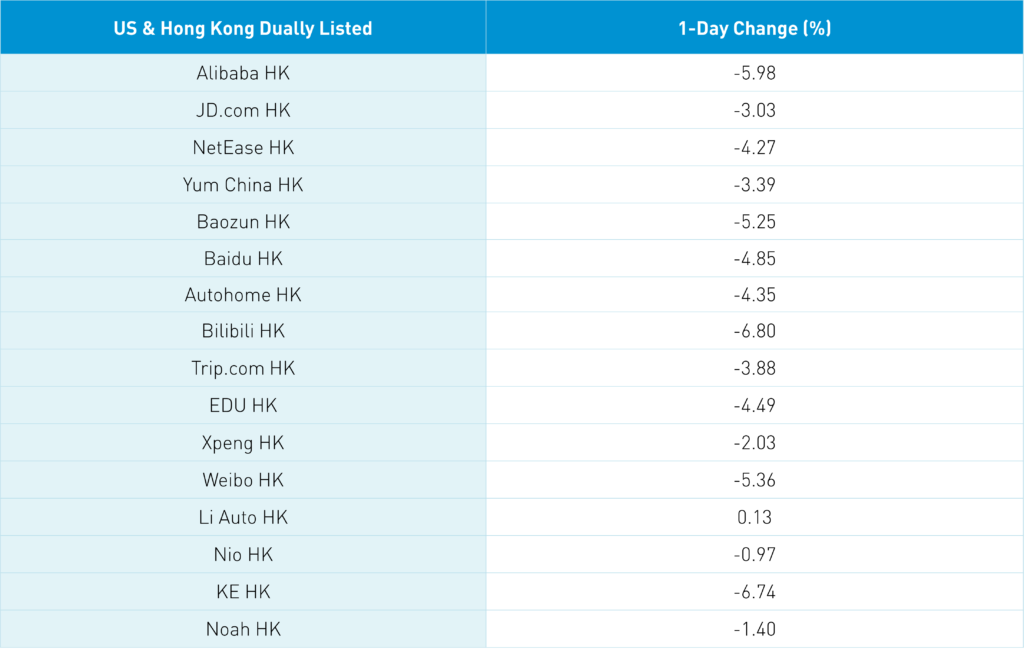

Hong Kong’s down day was the work of a different culprit: the Wall Street Journal’s article saying that Alibaba’s cloud unit executives met with Shanghai officials over a recent data breach that sent US-listed Chinese stocks lower yesterday. This news has neither been verified by the company nor by other sources. However, it did not matter. Short sellers pressed their bets significantly against Hong Kong-listed internet stocks as Hong Kong short sale turnover increased +41% from yesterday to 119% of the 1-year average. Long-only managers have not given much of a fight back and have not committed capital to defend the names against the backdrop of the constant barrage of negative media headlines. The vacuum created by the lack of buying has led to significant pressure on the names.

The Hang Seng Index is almost back to the 20k level from its late June high of 22,449. The release of June economic data, which occurred at 10 am local time, led to a rebound from worst levels in the morning as China’s GDP grew +0.4% year-over-year in Q2. This should be seen as a positive and it will lead to more policy support. However, the mid-morning rally could not hold up as afternoon selling intensified.

Foreign investors sold Mainland stocks via Northbound Stock Connect to the tune of -$1.3 billion, leading to pressure on the stocks and weighing on sentiment. However, it wasn’t a total washout as electric vehicles and automakers generally held up in both markets. Meanwhile, June retail sales beat expectations of +0.3% with a print of +3.1%. Online retail sales of physical goods increased +5.6% year-over-year, which now accounts for 25.9% of total retail sales of consumer goods. Consumption clearly picked up in June though industrial production was a touch light, coming in at 3.9% versus an expected 4% while fixed asset investment came in at 6.1% versus an expected 6%. It is feasible that we will see the real estate situation further addressed over the weekend along with additional supportive economic policies announced.

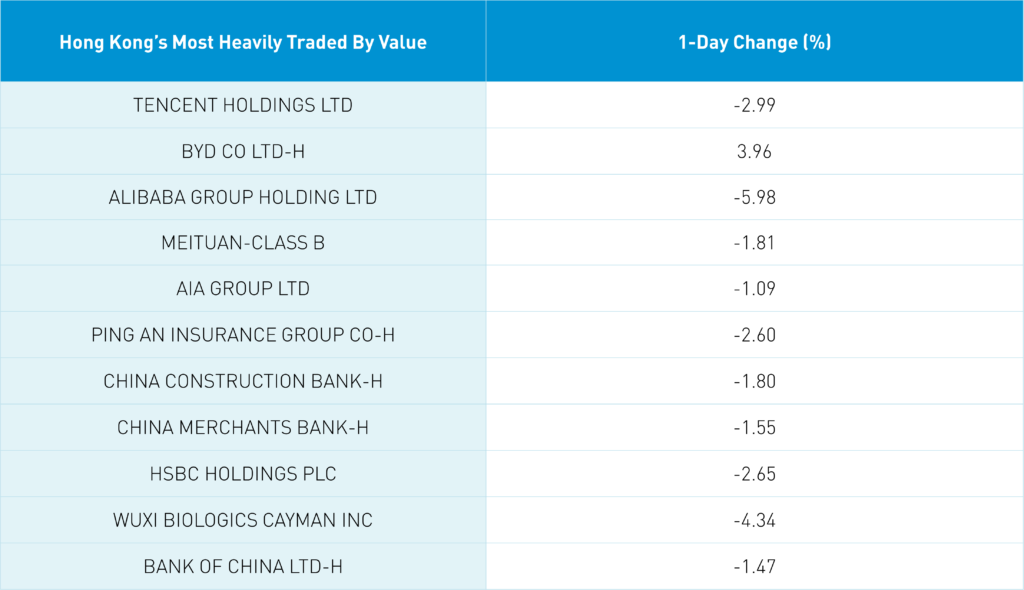

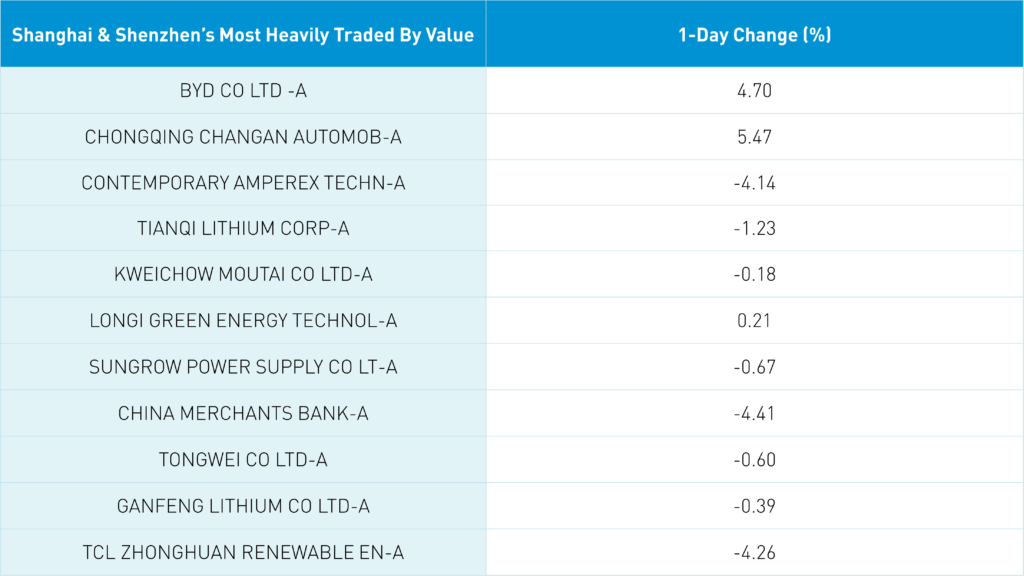

The Hang Seng and Hang Seng Tech indexes fell -2.19% and -3.22%, respectively, as volume increased +14.84% from yesterday, which is 92% of the 1-year average. 34 stocks advanced while 466 declined. Hong Kong short sale turnover increased +41.38% from yesterday, which is 119% of the 1-year average as short sale volume accounted for 21% of trading. Value outperformed growth as large caps outperformed small caps. All sectors were down today as energy fell -0.2%, real estate fell -4.7%, healthcare fell -3.75%, and communication services fell -3.35%. Electric vehicle battery plays including lithium stocks constituted one of the few bright spots overnight while online education, precious metals, and healthcare sub-sectors were among the worst. Southbound Stock Connect volumes were light/moderate as Mainland investors were net buyers of Hong Kong stocks, including Tencent and BYD, though Meituan saw some selling.

Shanghai, Shenzhen, and the STAR Board were off -1.64%, -1.49%, and -0.42%, respectively, on volume that increased +5.61% from yesterday, which is 100% of the 1-year average. 1,106 stocks advanced while 2,426 stocks declined. Growth and value factors were mixed while large caps outperformed small caps slightly. Consumer discretionary was the only positive sector, gaining +0.72%. Meanwhile, real estate fell -4.41%, industrials fell -2.14%, and healthcare fell -2.07%. Auto parts was a top sub-sector along with semiconductors while real estate related sub-sectors including infrastructure and iron ore among the worst performing sub-sectors. Northbound Stock Connect flows were moderate as foreign investors sold -$1.3 billion worth of Mainland stocks. Treasury bonds rallied, CNY was flat versus the US dollar, and copper was off -2.05%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.76 versus 6.76

- CNY/EUR 6.82 versus 6.76 yesterday

- Yield on 1-Day Government Bond 1.21% versus 1.19% yesterday

- Yield on 10-Year Government Bond 2.79% versus 2.79% yesterday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.06% yesterday

- Copper Price -2.05% overnight