Alibaba’s Softbank Overhang Clarified as Foreigners Fret

3 Min. Read Time

Key News

Asian equities were a sea of red on light volumes as South Asia held up slightly better than North Asia following the US equities meltdown yesterday.

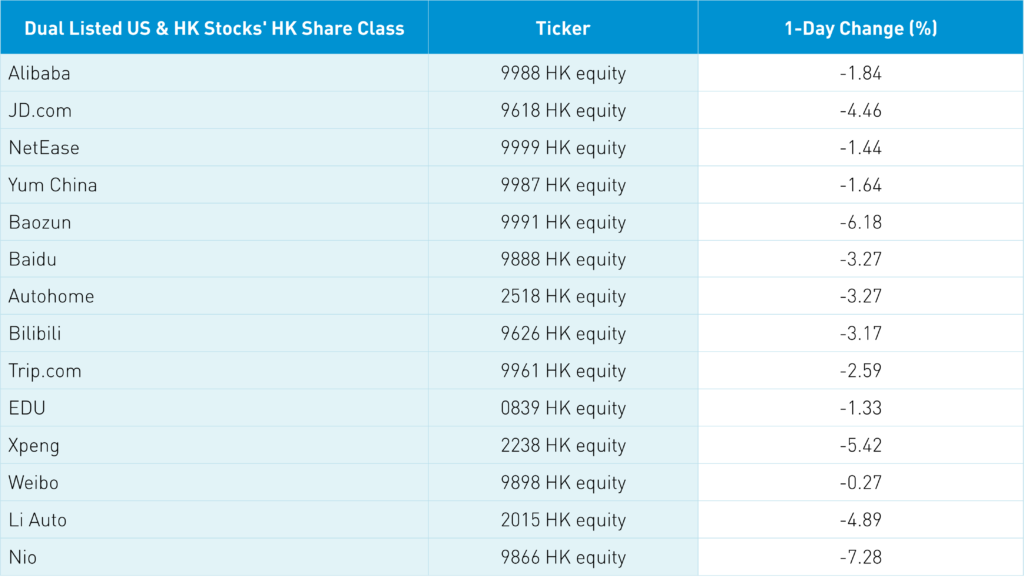

After the Hong Kong close, Alibaba and Softbank issued statements after the latter reduced their position in the former to 14.6% from 23.7% by selling 242 million shares via derivative contracts. Basically, Softbank wrote/sold an in the money call to investment banks allowing the company to collect the proceeds and book a $34 billion gain. The banks would hedge themselves as they effectively sold the shares in the market. The key is Softbank said they wouldn’t do this again alleviating the risk of more shares being sold i.e. an overhang on the stock. Similar to what’s happening to Tencent as Prosus keeps selling shares but no guidance on when it will end.

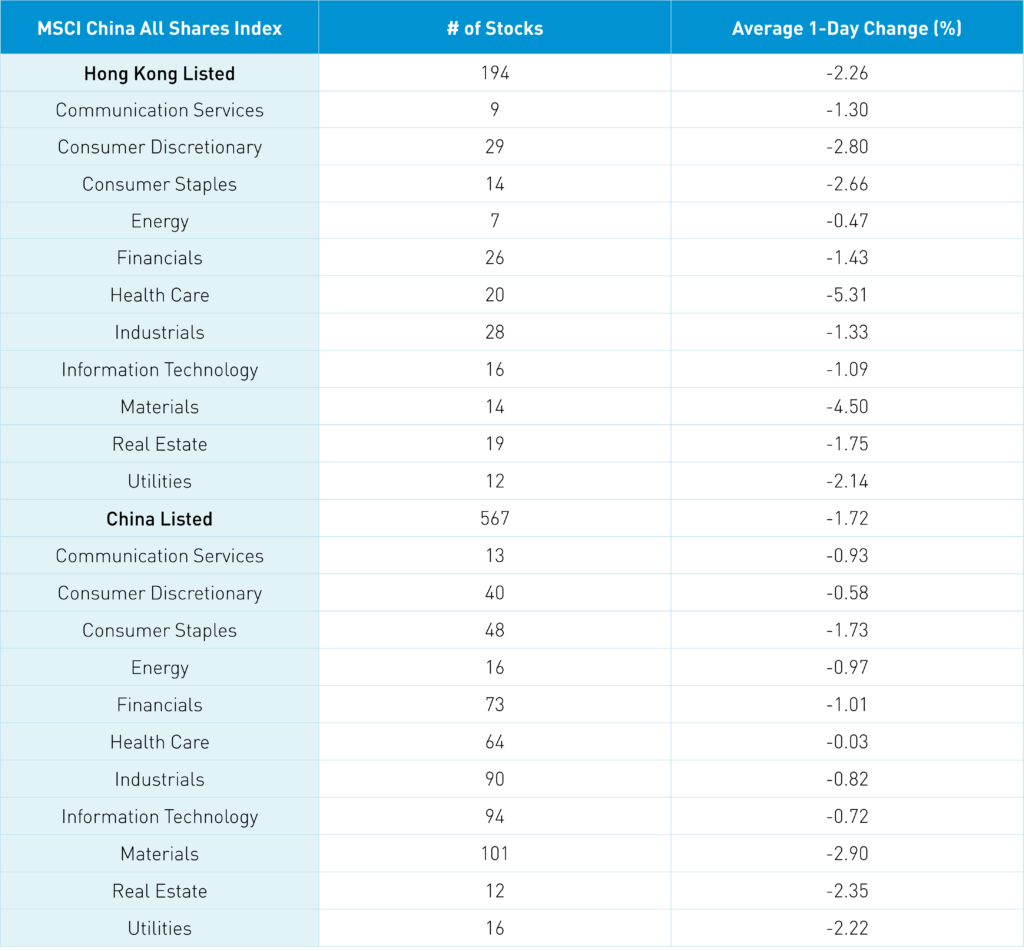

China’s July CPI was 2.7% versus an expected 2.9% and June’s 2.5% was driven by high pork prices while PPI was 4.2% versus an expected 4.9% and June’s 6.1%. Inflation data wasn’t a market mover. Once again Hong Kong/offshore market underperformed as foreign sentiment is weak though the Mainland market was immune. Only 9 of Hong Kong’s 100 most heavily traded stocks were up today. The Hang Seng closed below the 20k level at 19,610 which is nearly down -10% from the Covid lows in March 2020.

It was light night on news though a few negatives had bigger repercussions due to the light/thin volume. Hong Kong and to a lesser degree Chinese healthcare stocks especially Wuxi Biologics -9.26% were hit hard as a few local brokers saying companies’ efforts to be removed from the US’ unverified list aren’t going well. My understanding is the US Department of Commerce isn’t visiting Hong Kong, so they won’t say the companies aren’t involved in nuclear, missile, and chemical/biological weapons.

Real estate names were down after developer Longfor fell -16.4% on no news taking out the whole sector. The stocks and bonds of Chinese real estate companies have been hit exceedingly hard which has completely changed indices. This is not just due to internal issues, as risk off/rising US interest rates have led to credit spreads widening in many fixed income markets. For instance, JP Morgan Asia US $ high yield bond index doesn’t look anything like it did a year ago. Within the index, Chinese property bonds went from 41% to 15% as real estate declined from 48% to 25% of the index! Overnight a Mainland media source noted significant relaxation of property buying rules across multiple Chinese cities and provinces. Clearly the government needs to support this sector and get developers to finish their projects. It will be interesting to see how this issue is addressed.

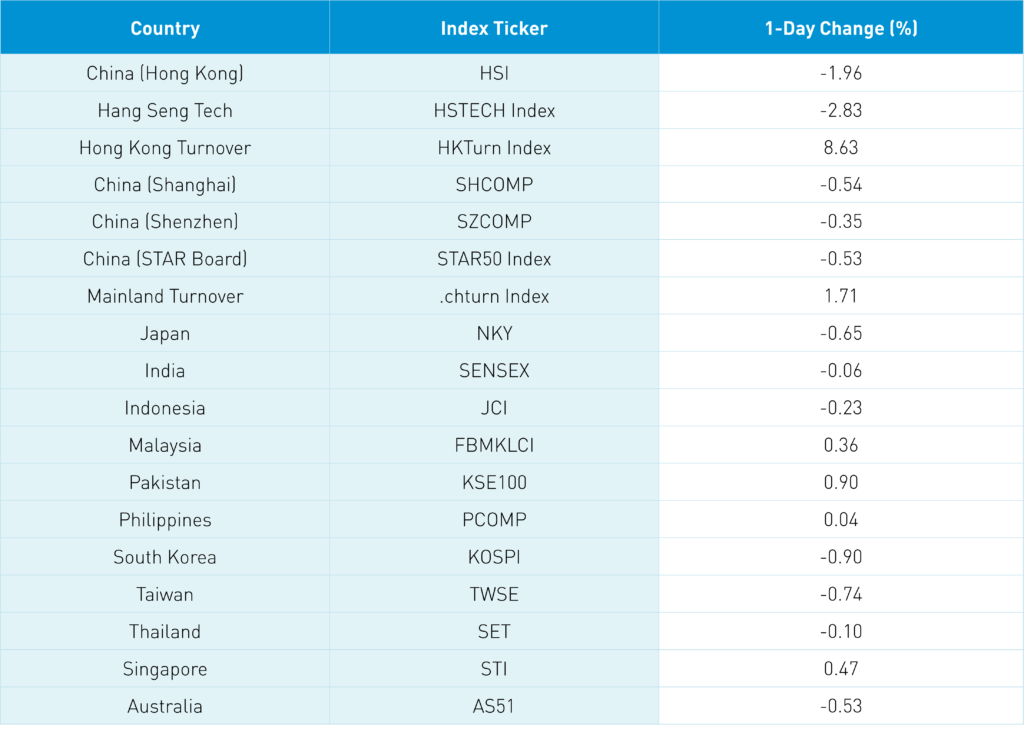

The Hang Seng and Hang Seng Tech declined -1.96% and -2.83% on volume +8.63% from yesterday which is 66% of the 1-year average. Only 36 stock advanced while 454 declined. Hong Kong short sale turnover increased +17.3% which is 73% of the 1-year average while short sale turnover accounted for 18% of total turnover. Growth and value factors were mixed as large caps “outperformed” small caps. All sectors were down with energy -0.48% while healthcare -5.32%, real estate -4.51%, and tech -2.9%. Telecom related sub-sectors were among the few positive sectors while Foxconn ecosystem stocks, healthcare sub-sectors were among the worst. Southbound Stock Connect volumes were light as Mainland investors were buyers of Hong Kong stocks with Tencent, Li Auto, and Tianqi Lithium seeing small net buys while Meituan, Kuiashou, and Xpeng were small net sales.

Shanghai, Shenzhen, and STAR Board declined -0.54%, -0.35%, and -0.53% on volume +1.71% which is 91% of the 1-year average. 1,914 stocks advanced while 2,557 stocks declined. Value factors outperformed growth as large and small were flat versus one another. Materials was the only positive sector +0.01% while discretionary -2.1%, healthcare 1.69%, and staples -1.68%. Top sub-sectors included petrochemicals, precious metals, and solar power while lithium, battery, and aviation/airport were among the worst. Northbound Stock Connect volumes were light as foreign investors sold -$923 million of Mainland stocks. Shorter maturity Treasury bonds sold off again while CNY eased -0.05% versus the US $ and copper gained +0.25%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.76 versus 6.75 yesterday

- CNY/EUR 6.92 versus 6.90 yesterday

- Yield on 10-Year Government Bond 2.74% versus 2.74% yesterday

- Yield on 10-Year China Development Bank Bond 2.91% versus 2.91% yesterday

- Copper Price +0.25% overnight