Jerome Powell & US Dollar Summer Global Wrecking Ball Tour Continues

3 Min. Read Time

Key News

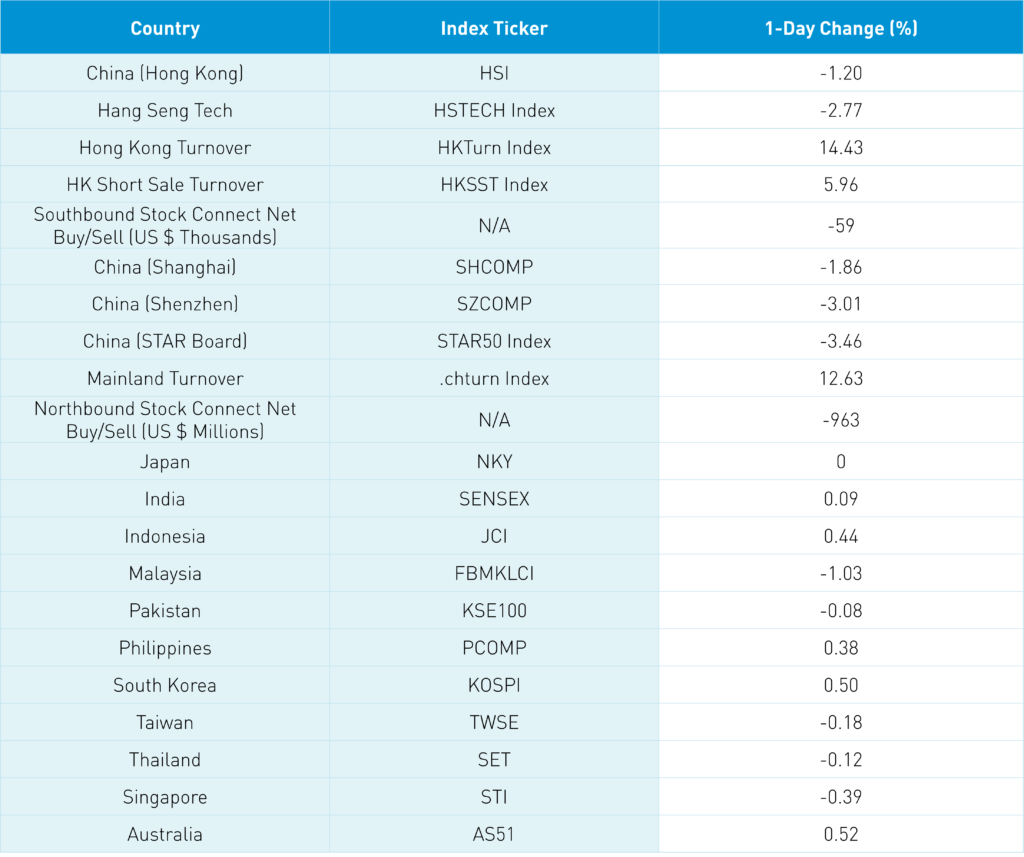

Asian equities were mixed/lower overnight as South Korea, India, and Southeast Asia managed small gains while Japan, Hong Kong, and China were off. Global equities are in a significant slump in advance of the Fed’s Jackson Hole meeting and the specter of higher US interest rates. ADXY, Asia US dollar index, hit another 52-week low today, sinking to a level last seen on September 30, 2004. One has to wonder how much domestic and international carnage the Fed can take before criticism and the media narrative turn negative. Despite opening higher, Hong Kong and China were both off, though for different reasons.

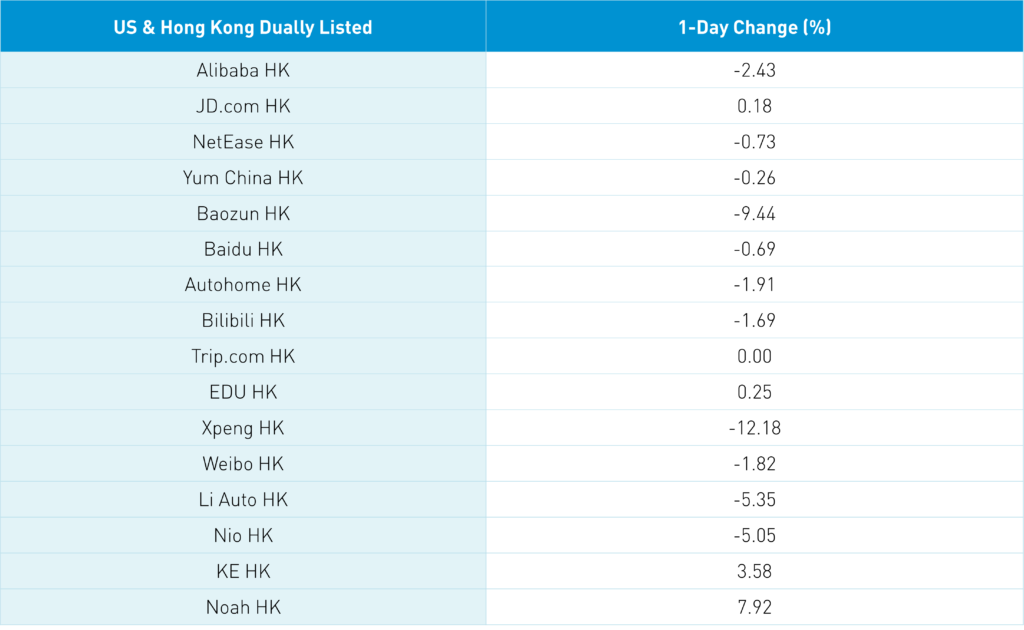

“Despite” was the word of the day in Hong Kong as Kuaishou fell by -8.12% “despite” strong financial results. JD.com HK gained only +0.18% “despite” better than expected results yesterday. Tencent was off -0.9% “despite” buying back shares for the 4th day in a row today. Baidu HK was off -0.69% “despite” a local broker initiating coverage with an outperform and the company being added to the Hang Seng Index in a week. Once again, shorts pressed their bets in Hong Kong as short sale turnover is at 90% of the 1-year average versus total turnover, which stands at only 75%. Xpeng HK was off -12.18% after mixed financial results and a weak outlook resulting in NIO HK falling -5.05% and Li Auto HK falling -5.35%. I had thought Hong Kong stocks trading in Hong Kong dollars, which are pegged to the US dollar, would provide some margin of safety when it comes to the US dollar’s global wrecking ball, though that has not occurred. Ping An (2318 HK) and Anta Sports (2020 HK) managed gains of +2.56% and +3.97%, respectively, following strong results.

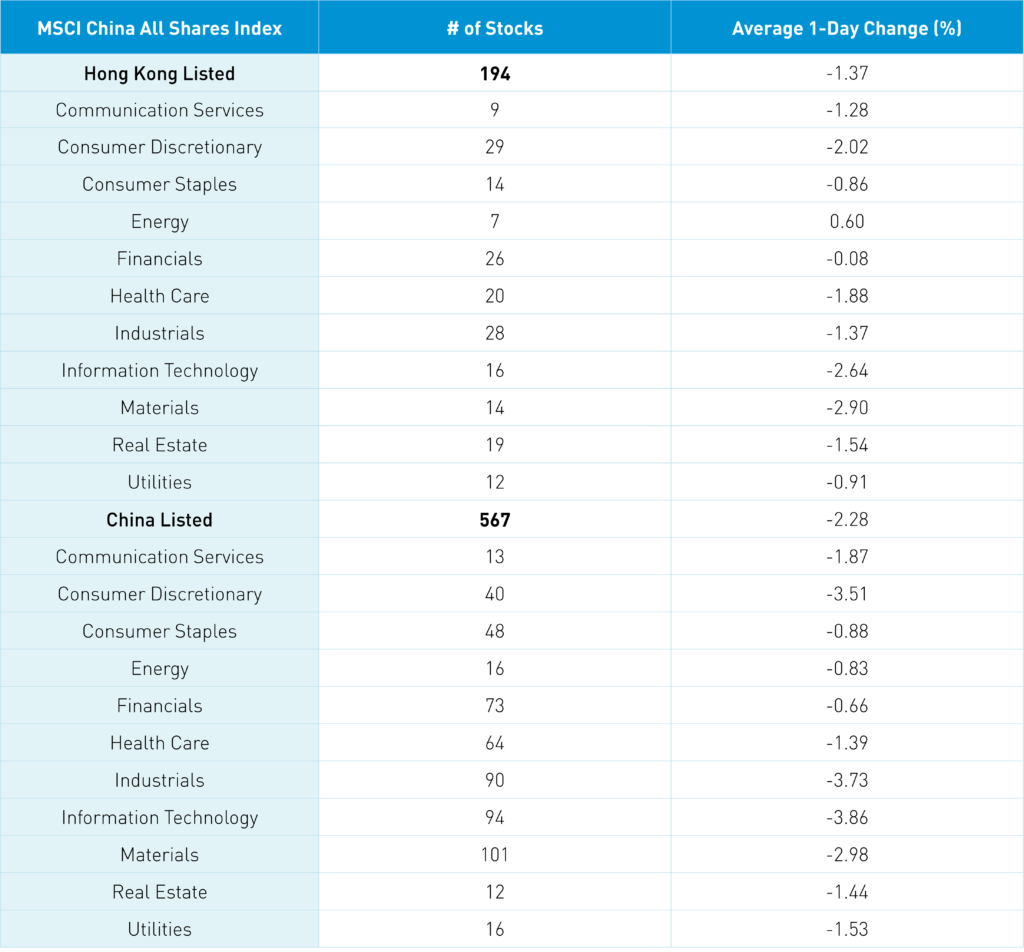

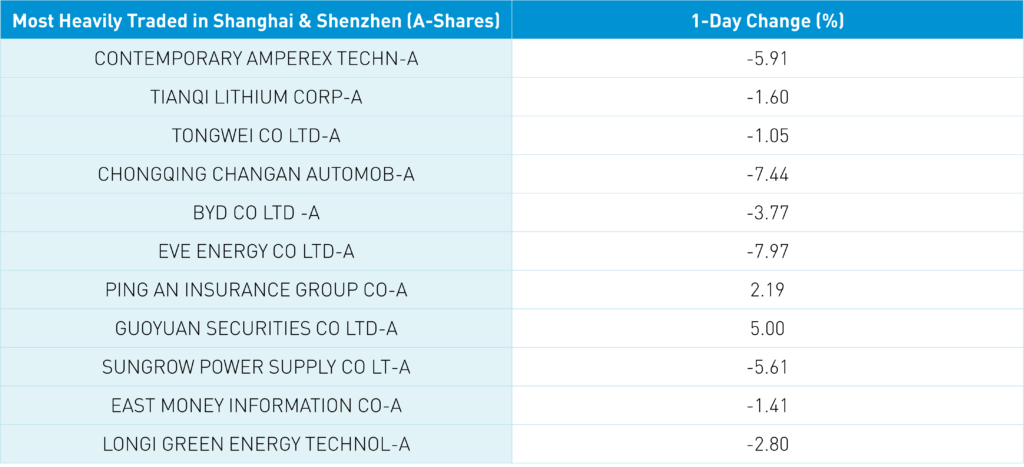

Mainland China had a disappointing day led lower by growth stocks, particularly the clean technology ecosystem. Today was one of the worst breadth/advancers versus decliners I’ve seen since the summer of 2015, with only 536 stocks advanced versus 4,162 declining. Global EV battery maker CATL (300750 CH) was off -5.91% after opening +2.9% on profit taking after very strong earnings. The stock has increased more than 600% since its September 2019 uptrend. Solar names were hit after three government agencies said they would look into the photovoltaic industry’s pricing and supply policies. Due to domestic and international demand for Chinese solar panels, there is concern that manufacturers might be hoarding inputs. Solar’s weakness spread to other growth stocks, sectors, and the STAR Board. After the close, Longi Green Energy (601012) -2.8% reported strong financial results that handily beat estimates. Foreign investors were net sellers of Mainland stocks today -$963mm. After the close, Premier Li and the State Council outlined six policies to support the economy. China’s heatwave continues weighing hydroelectric output as a typhoon barrels down on Hong Kong.

The Hang Seng and Hang Seng Tech fell -1.2% and -2.77% on volume +14.43% from yesterday, which is 75% of the 1-year average. 84 stocks rose while 394 stocks fell. Hong Kong short sale turnover increased +5.97% from yesterday, which is 90% of the 1-year average as short sales accounted for 20% of turnover. Growth and value factors were mixed as large caps outperformed small caps. Energy was the only positive sector +0.6% while materials -2.9%, tech -2.64% and discretionary -2.02%. Top sub-sectors included oil, petrochemical, and shale gas stocks, while online video, telemedicine, and EV-related sub-sectors like lithium, battery, and charging were among the worst. Southbound Stock Connect volumes were moderate as Mainland investors sold -$59mm of Hong Kong stocks, with Meituan seeing another strong outflow day, Li Auto a small buy, BYD, Tencent, and Kuaishou were a very small sell.

Shanghai, Shenzhen, and STAR Board were down -1.86%, -3.01%, and -3.46% on volume +12.63% from yesterday, which is 107% of the 1-year average. 536 stocks advanced while 4,162 stocks advanced. Value factors outperformed growth today as large caps outperformed small caps. All sectors were down, with financials “outperforming” by -0.67% while tech -3.88%, industrials -3.75%, and discretionary -3.52%. Insurance and biotech were among a few green stocks, while industrial sub-sectors and Tesla’secosystem were among the worst. Northbound Stock Connect volumes were moderate as foreign investors sold -$96mm of Mainland stocks today. Treasury bonds were off today, CNY fell -0.47% versus the US $ to 6.86, and copper gained +0.8%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.87 versus 6.85 yesterday

- CNY/EUR 6.82 versus 6.79 yesterday

- Yield on 10-Year Government Bond 2.61% versus 2.61% yesterday

- Yield on 10-Year China Development Bank Bond 2.80% versus 2.80% yesterday

- Copper Price +0.80% overnight