HFCAA First Step Audit Agreement Reached

4 Min. Read Time

This morning, the SEC, PCAOB, and CSRC, in conjunction with the Ministry of Finance, released statements announcing the signing of a Statement of Protocol allowing the PCAOB to conduct full audit reviews of US-listed Chinese companies. The deal is the first step as the audit reviews still need to take place. Considering all of the companies are audited by the "Big Four" accounting firms' China arms, this should not be a big deal.

The voluntary delisting of five State Owned Enterprises' (SOEs) US ADRs was a significant signal of a deal as these companies do have sensitive information that could be seen in an audit review. Non-SOEs, on the other hand, have nothing to hide, as many have publicly stated. This is significant news as the Holding Foreign Companies Accountable Act (HFCAA) has been an overhang on the space.

Active emerging market mutual funds have an average of 2% underweight to China as they have been hesitant to buy Chinese internet stocks due to potentially bad HFCAA news coming out. These managers are at significant risk of underperforming if the stocks rebound.

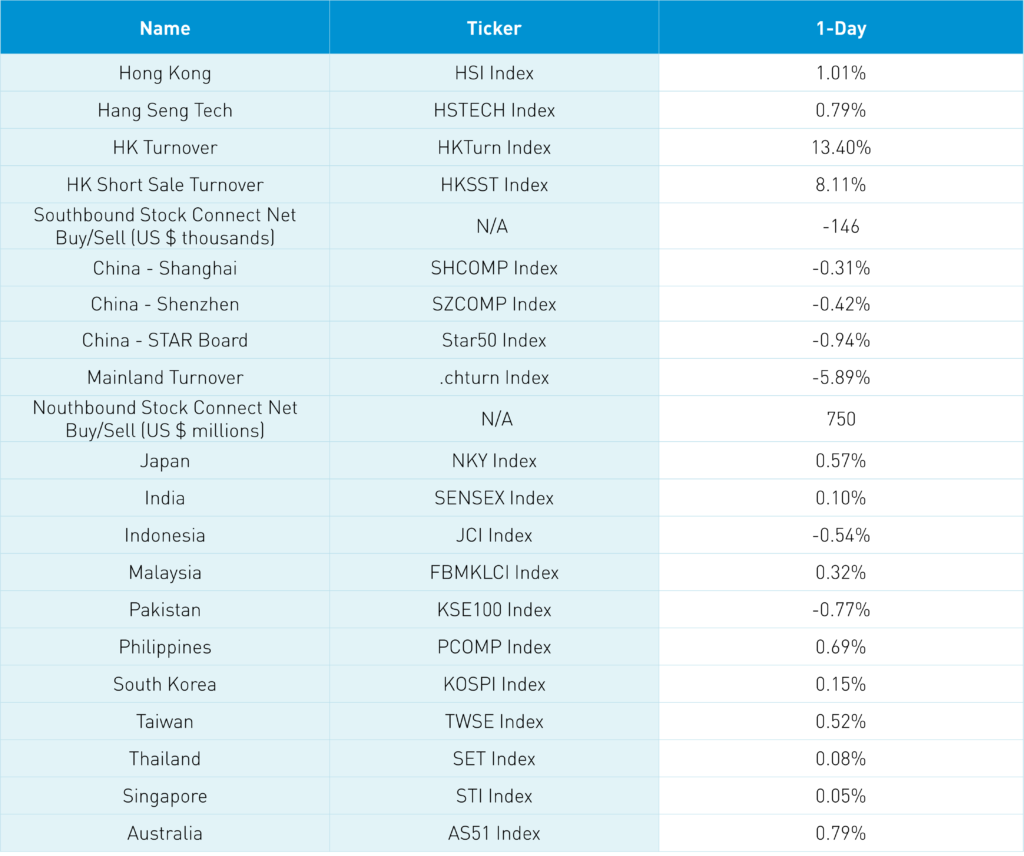

Considering the significant valuation discount due to the HFCAA, one should hope for a significant rebound on re-rating. Hong Kong short sellers have been pressing their bets on the stocks, as evidenced by Hong Kong short sale turnover, which has increased +50% in the last six months versus the 10-year average. Today, Hong Kong's short sale turnover increased +8% from yesterday, which is 83% of its 1-year average, versus total turnover, which was only 78% of its 1-year average. 23% of Tencent’s trading was short today, 24% of Meituan's trading, 15% of Alibaba's, and 21% of JD.com's. 47% of the largest Hong Kong-listed ETF was short volume today! Shorts have pressed their bets based on light summer volumes, knowing that many investors are on vacation or unwilling to step in and defend the stocks due to HFCAA. A strong short squeeze accompanied by institutional buying should be a strong catalyst. Fingers crossed!

Congratulations the SEC, PCAOB, CSRC, and MoF for their hard work and efforts! $2 trillion of US investors' savings was put at risk due to the HFCAA.

Key News

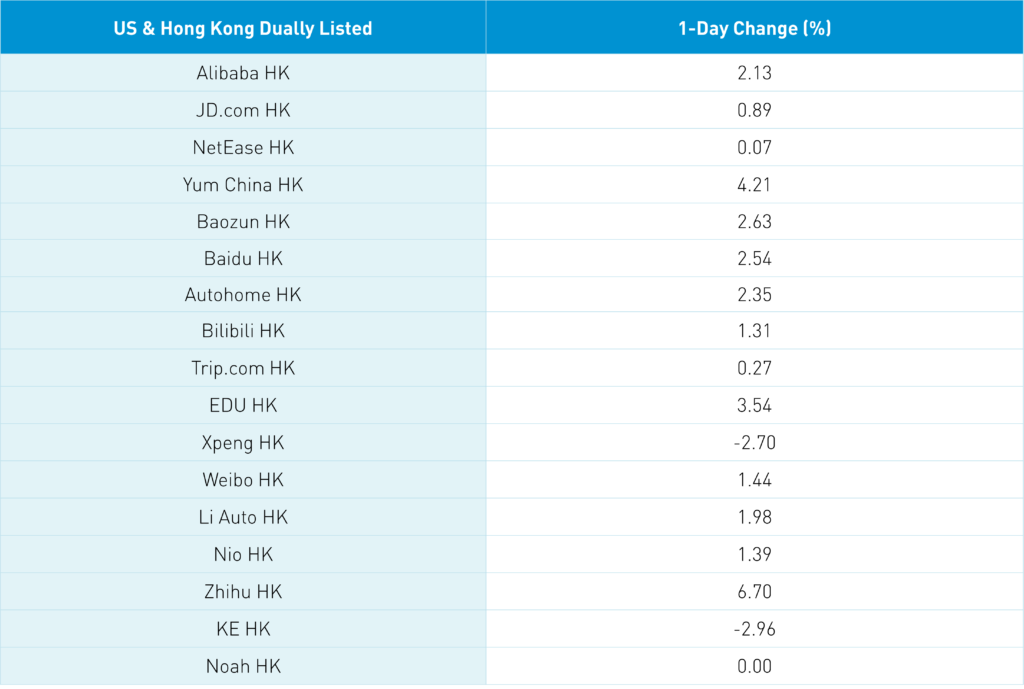

Asian equities ended a slightly down week with small gains in advance of Powell’s Jackson Hole press conference. The most heavily traded stocks by value in Hong Kong were all internet stocks, including Tencent, which fell -0.25%, Meituan, which gained +2.59%, Alibaba HK, which gained +2.13%, JD.com HK, which gained +0.89%, and Kuaishou, which fell -4.07%. The names were up, but not as much as their US-listed counterparts.

This is despite the South China Morning Post releasing an article at the market’s open stating that “China’s securities regulator is amendable to grant access to redacted auditing data to overseas inspectors and use Hong Kong as the neutral ground…according to sources.” Reuters also released an article stating, “Beijing has asked some U.S.-listed Chinese companies and audit firms to prepare for American inspections in Hong Kong, three sources familiar with the matter told Reuters…”. The big clue was two Fridays ago when 5 State Owned Enterprises said they would voluntarily delist from the US, thereby removing companies that may have sensitive information contained in their audit papers.

Hong Kong short sellers pressed their bets today as short sale volume increased +8% from yesterday. With today’s morning announcement, those positions are at significant risk.

After the close in Hong Kong, Meituan announced Q2 financial results, which indicated a +1.4% year-over-year (YoY) revenue increase to RMB 50.9 billion from RMB 43.8 billion versus expectations of RMB 48.58B. Adjusted net income was RMB 2.1 billion, up from a loss of RMB -3.6 billion and expectations of a loss of RMB -2.2 billion. Adjusted EPS came in at RMB 0.33 versus expectations of a loss of RMB -0.38.

Mainland China was lower in advance of the Fed’s announcement today. Yes, investors in China are highly attuned to this issue though sentiment has been fragile due to housing price weakness. Remember that a significant amount of household wealth is in housing, which has seen new sales decline considerably while prices are off. This sentiment weighs on investors though clearly, there is significant policy support for stabilizing housing sales and prices. We should hopefully see animal spirits rebound! Foreign investors bought $750 million worth of Mainland stocks today.

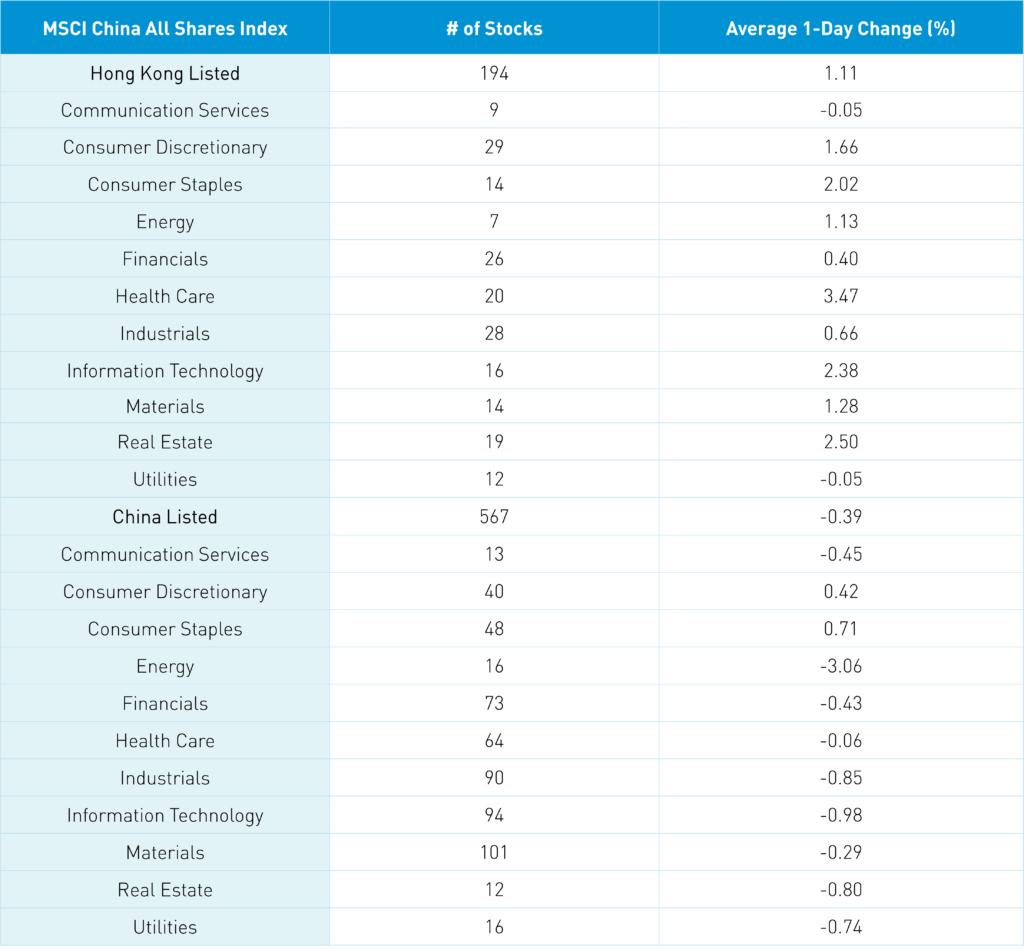

The Hang Seng and Hang Seng Tech indexes gained +1.01% and +0.79%, respectively, on volume that increased +13.4% from yesterday, which is 78% of the 1-year average. 364 stocks advanced while 102 stocks declined. Hong Kong short sale turnover increased +8.11% from yesterday, which is 83% of the 1-year average, as short sale trading accounted for 18% of turnover. Growth factors outpaced value though both did well as large caps outpaced small caps. The top performing sectors were healthcare, which gained +3.47%, real estate, which gained +2.5%, tech, which gained +2.38%, and staples, which gained +2.02. Meanwhile, communication services and utilities were both off -0.05%. The top performing sub-sectors today included autos, electric vehicles, and healthcare-related subsectors such as contract research organizations (CROs) and biotech, while electric utilities, online video, and e-cigarettes were among the worst. Southbound Stock Connect volumes were light/moderate as Mainland investors sold -$146 million worth of Hong Kong stocks as Meituan and Kuiashou saw moderate selling, and Tencent saw moderate net buying.

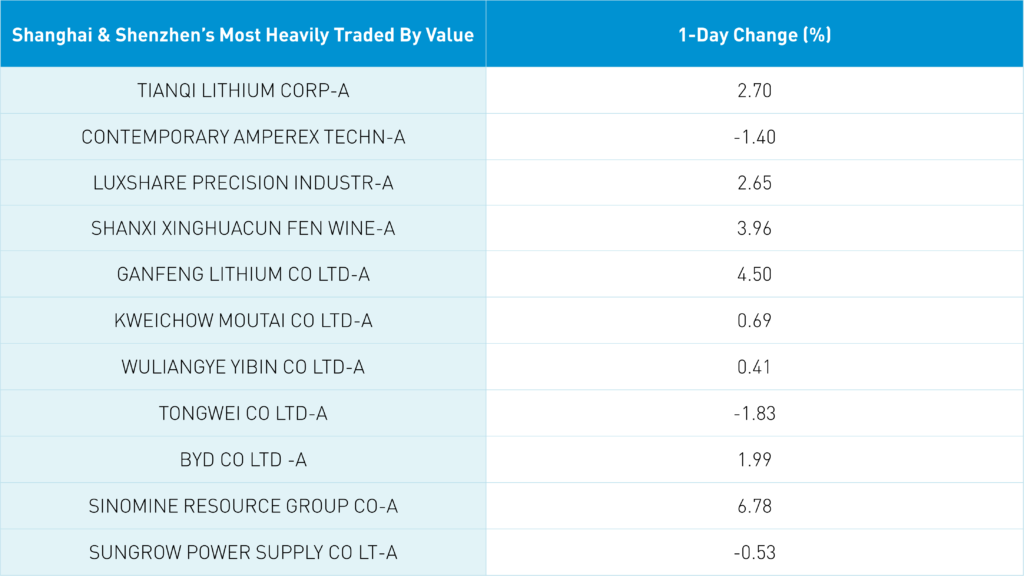

Shanghai, Shenzhen, and the STAR Board were off -0.31%, -0.42%, and -0.94%, respectively, on volume that was down -5.94% from yesterday, which is 97% of the 1-year average. 1,978 stocks advanced while 2,522 stocks declined. Value factors outperformed growth as large caps outperformed small caps. The only positive sectors today were consumer staples, which gained +0.72%, and discretionary, which gained +0.44%. Meanwhile, energy fell -3.04%, tech fell -0.96%, and industrials fell -0.84%. The top performing sub-sectors on the Mainland included lithium, electric vehicles, and dairy, while shipping, semiconductors, and software were among the worst. Northbound Stock Connect volumes were moderate as foreign investors bought $750 million worth of Mainland stocks. The treasury bond yield curve steepened, CNY was off -0.2% versus the US dollar to 6.86, and copper gained +1.15%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.86 versus 6.85 yesterday

- CNY/EUR 6.89 versus 6.83 yesterday

- Yield on 1-Day Government Bond 1.15% versus 1.13% yesterday

- Yield on 10-Year Government Bond 2.64% versus 2.64% yesterday

- Yield on 10-Year China Development Bank Bond 2.84% versus 2.83% yesterday

- Copper Price +1.15% overnight