PCAOB Begins Audit Reviews

3 Min. Read Time

Key News

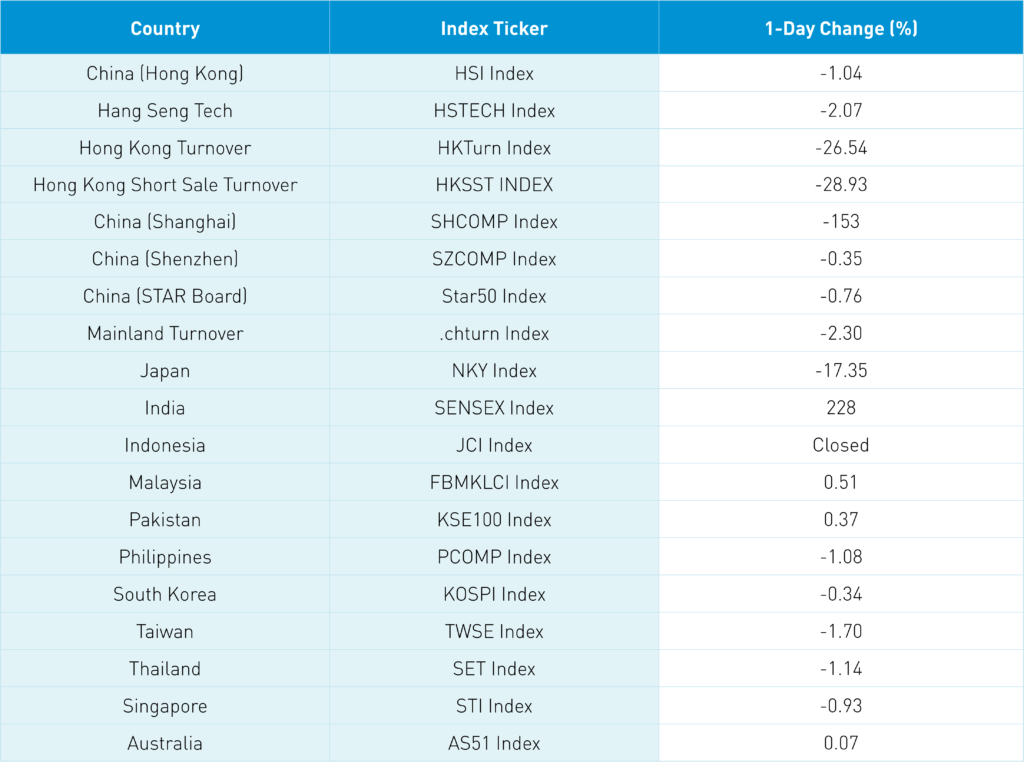

Asian equity markets closed lower to start the week in anticipation of the US Federal Reserve hiking interest rates another 75 basis points. However, India managed a small gain while Japan was closed for the “Respect For The Aged Day” holiday.

I apologize in advance for sounding like a broken record, but offshore China (Hong Kong and US-listed stocks) reacted to the latest news cycle negatively, while onshore China (Shanghai & Shenzhen listed stocks) did not really care. President Biden’s 60 Minutes interview reiterated longstanding US policies on Taiwan but also mentioned defending the island against an attack, which has always been implied, but not stated publicly.

Another offshore factor was that the Public Company Accounting Oversight Board (PCAOB) began the audit review process overnight by meeting with PwC and KPMG in Hong Kong. While we believe such a meeting should be viewed as a positive, considering that a clean audit review would remove the delisting risk, the US media took this as a negative.

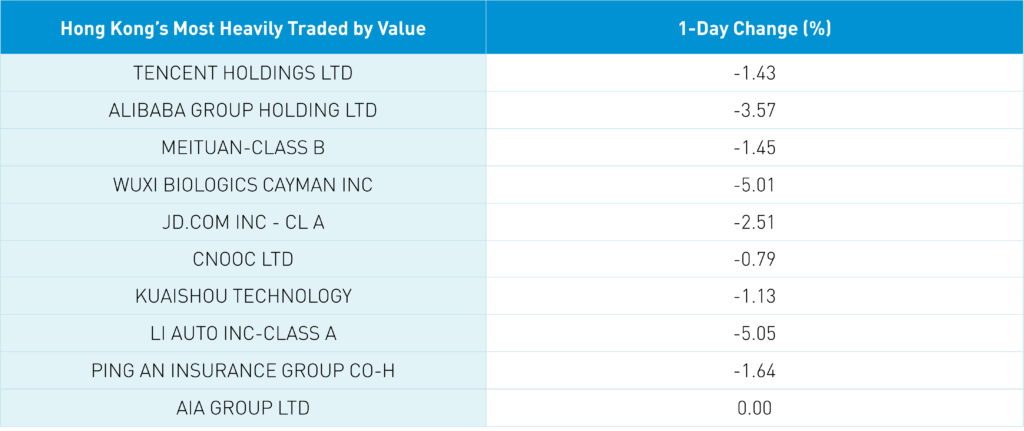

Hong Kong internet names were weak and underperformed today though short volume fell from Friday. However, 30% of Meituan’s turnover was short turnover, compared to 16% for Alibaba HK and 26% for JD.com HK. Meanwhile, Tencent saw short volume fall to just 6% of total turnover.

There is increasing chatter that Hong Kong’s travel restrictions could be removed and that Mainland lockdowns could be eased further. Also, data from trials of CSPC Pharmaceutical's China-made mRNA vaccine looks promising so far, increasing the likelihood of emergency authorization as early as next month.

Among other positive news stories that went unnoticed, President Xi clearly distanced himself from Russia last week during talks, along with India’s Modi. China and India appear to be warming to each other somewhat as they are both Russia’s top trade partners amid sanctions and would like to see the Ukraine conflict come to an end.

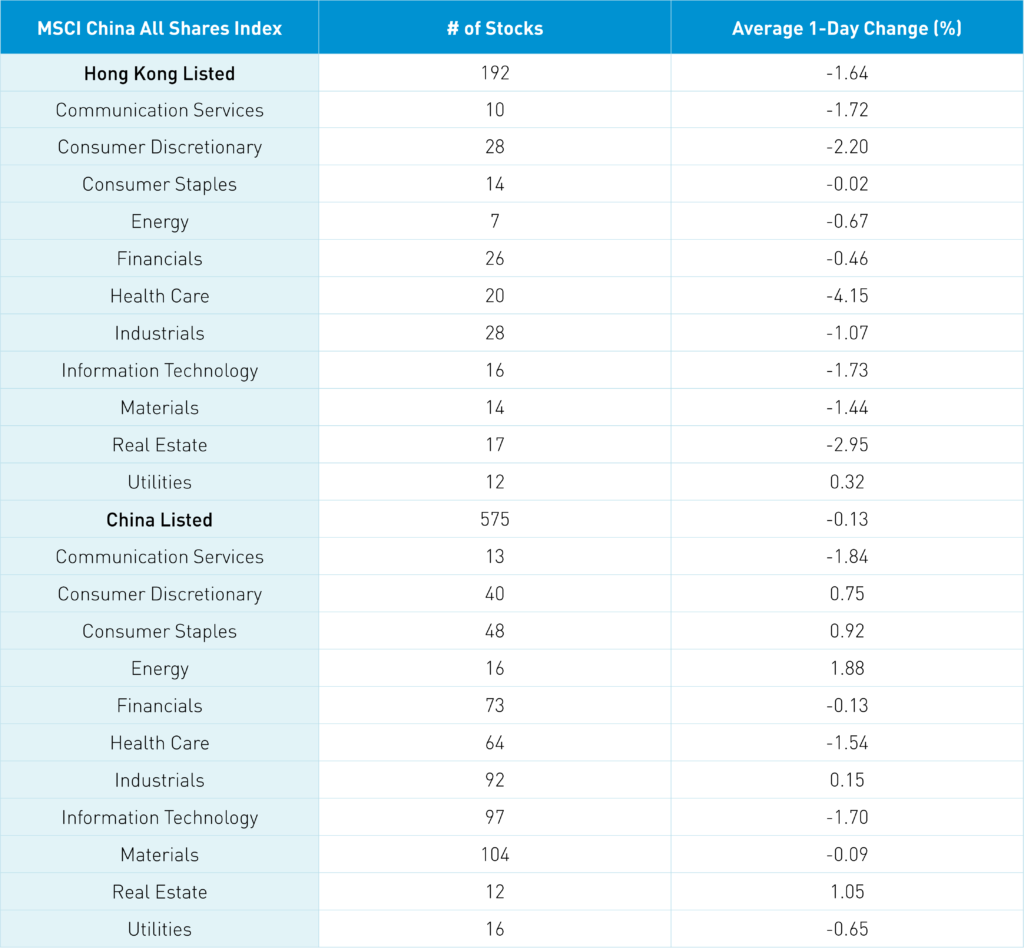

Highlighting the continuing disparity between onshore and offshore equities, real estate was the second-best performer in the onshore market, where it gained +1.11%. Meanwhile, in the offshore (Hong Kong) market, it was the second worst performer, falling -2.95%. The Mainland market was off overall, but not as significantly as the Hong Kong market, on little news. The Asia dollar index hit a 52-week low as the US dollar is near its 52-week high. CNY was off versus the US dollar, falling to 7.01. The People’s Bank of China (PBOC), China’s central bank, will announce the new loan prime rate (LPR) today though the key lending rate is expected to remain unchanged.

The Hang Seng and Hang Seng Tech indexes fell -1.04% and -2.07%, respectively, on volume that was down -26.54% from Friday, which is 71% of the 1-year average. 101 stocks advanced while 390 stocks fell. Hong Kong short sale turnover fell -28.93% from Friday, which is 74% of the 1-year average, as short sale trading accounted for 18% of Hong Kong’s main board turnover. Value factors outperformed growth factors today and large caps outperformed small caps. Utilities were the only positive sector, gaining +0.32%. Meanwhile, healthcare fell -4.15%, real estate fell -2.95%, and consumer discretionary fell -by 2.2%. Gold, food, gas, and lithium batteries were among the top performing sub-sectors, while the Tik Tok ecosystem, biotech, education, and property management were among the worst. Southbound Stock Connect volumes were low, which has become the new normal as Mainland investors sold -$153 million worth of Hong Kong stocks as Tencent, Wuxi Biologics, Kuaishou, and Li Auto were all small net buys, while Meituan was a small/moderate net sell.

Shanghai, Shenzhen, and the STAR Board were off -0.35%, -0.76%, and -2.3%, respectively, as volume fell -17.35% from Friday, which is 65% of the 1-year average. 946 stocks advanced while 3,626 stocks declined. Value factors outperformed growth factors as large caps outperformed small caps. The top performing sectors were energy, which gained +1.92%, real estate, which gained +1.09%, and consumer staples, which gained +0.96%. Meanwhile, communication services fell -1.8%, information technology fell -1.66%, and healthcare fell -1.49%. Airports, autos, and coal were among the top performing sub-sectors, while internet, software, and construction were among the worst performing. Northbound Stock Connect flows were light as foreign investors bought $228 million worth of Mainland stocks today. Bonds were flat, CNY declined -0.41% versus the US dollar to 7.01, and copper gained +0.9%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 7.01 versus 6.99 Friday

- CNY/EUR 7.00 versus 7.00 Friday

- Yield on 1-Day Government Bond 1.13 versus 1.01 Friday

- Yield on 10-Year Government Bond 2.68% versus 6.67% Friday

- Yield on 10-Year China Development Bank Bond 2.83% versus 2.83% Friday

- Copper Price +0.90% overnight