Hong Kong Reopening Announced Along with Pro-Consumption Policies

2 Min. Read Time

Key News

Asian equities had a positive day on light volumes led by growth stocks across the region.

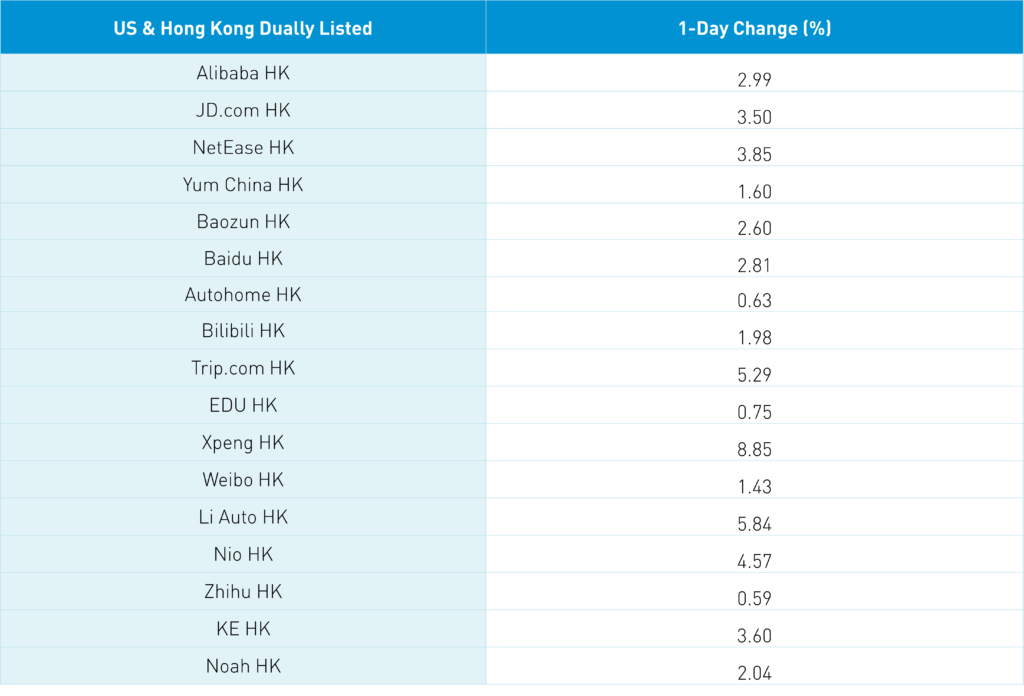

The Hong Kong government announced ending its hotel quarantine for foreign visitors without providing a date on when. Important to note the Mainland government agreed to the reopening. This is despite Hong Kong registering over 5,500 new Hong Kong covid cases overnight as zero covid is clearly being watered down. Macao casino stocks and travel plays like Trip.com HK +5.29% led the market higher along with Hong Kong internet plays as Hong Kong’s most heavily traded by value were Tencent +1.52%, Alibaba HK +2.99%, and Meituan +1.89%.

After the Hong Kong close, the WSJ is reporting that Tencent will divest from publicly traded investments such as Meituan, Kuaishou, and Didi according to “people familiar with the matter”. This rumor flared a week or two ago which the company denied. Can’t the media let us enjoy a strong up day? Short sellers pressed their bets as Meituan saw short volume increase to 36% from 30% yesterday, Tencent 19% from 6% yesterday, Alibaba HK 20% from 16%, and JD.com HK 34% from 26%.

Auto was a strong performer in both Hong Kong and the Mainland after the National Development and Reform Commission (NDRC) stated policies favoring big ticket consumption will be introduced. Auto and the EV ecosystem had a strong day though I was a bit surprised home appliance makers such as Gree Electric Appliance (000651 CH) -0.75% and Haier Smart Home (600690 CH) -1.11% were off despite the announcement appears to include them. Remember 25% of all retail sales flows through e-commerce companies like Alibaba, JD, and Pinduoduo which should help them as well. Real estate was off in both markets as the 1- and 5-year loan prime rates were left unchanged as expected and mixed news on housing support. Worth noting the Asia currency index hit a new 52 week low for the second day in a row.

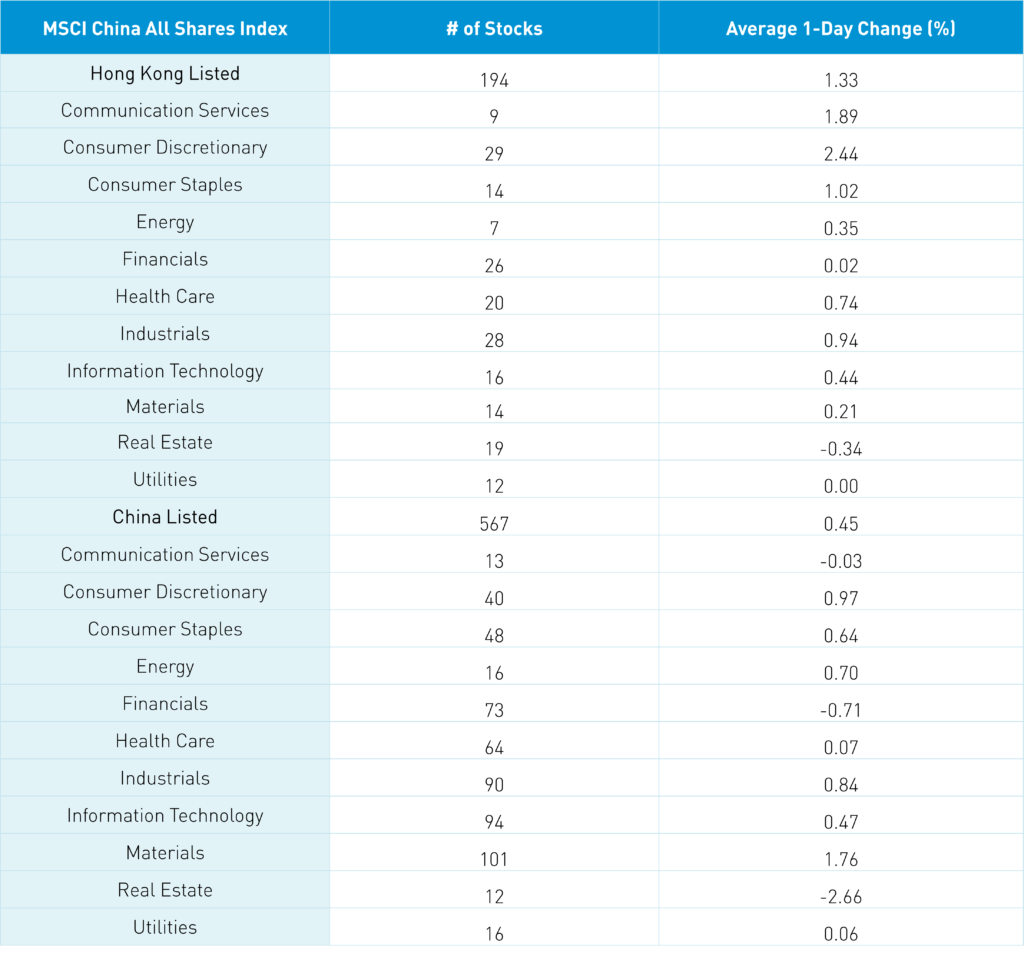

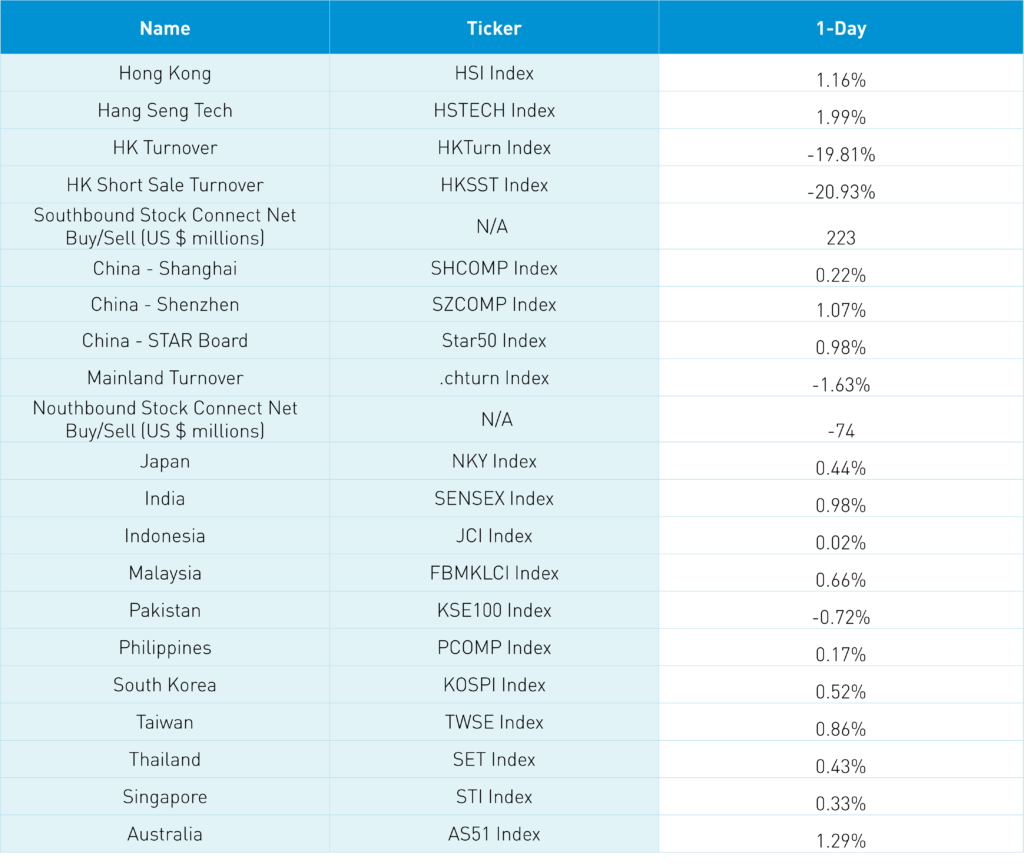

The Hang Seng and Hang Seng Tech gained +1.16% and +1.99% respectively on volume off -19.81% from the 1-year average which is 57% of the 1-year average. 287 stocks advanced while 194 declined. Hong Kong Main Board short selling turnover declined -20.93% from yesterday which is 58% of the 1-year average as short selling accounted for 17% of total turnover. Growth and value factors were mixed as large caps outperformed small caps. Top sectors were discretionary +2.44%, communication +1.9%, and staples +1.02% while real estate was the only negative sector -0.34%. Top sub-sectors included lithium, Macao casino stocks, auto, EV charging, and gold while liquor, cement, and online education were down. Southbound Stock Connect volumes were light as Mainland investors bought $223 million of Mainland stocks with Tencent a moderate buy, Kuaishou a small buy, and Meituan a small sell.

Shanghai, Shenzhen, and STAR gained +0.22%, +1.07%, and +0.98% on volume -1.63% from yesterday which is 64% of the 1-year average. 3,563 stocks advanced while 616 stocks declined. Growth factors outperformed value while small caps outpaced large caps by a small amount. Top-sub sectors were materials +1.76%, discretionary +0.97%, and industrials +0.84% while real estate -2.66%, financials -0.71%, and communication -0.94% fell slightly. Top sub-sectors included lithium mining, solar, and auto parts while real estate, insurance, and infrastructure were among the worst. Northbound Stock Connect volumes were light as foreign investors sold -$74 million of Mainland stocks. Chinese Treasury bonds rallied, CNY was off-0.11% versus the US closing at 7.01, while copper was off -0.14%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 7.01 versus 7.01 yesterday

- CNY/EUR 7.02 versus 7.00 yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.68% yesterday

- Yield on 10-Year China Development Bank Bond 2.81% versus 2.83% yesterday

- Copper Price -0.14% overnight