Hang Seng & Shanghai Composite Approach Key Levels For Policy Support

3 Min. Read Time

Key News

Asian equities were largely off on light volume though a few countries managed small gains. Australia avoided the Fed and Putin's escalation induced risk-off day due to a holiday for mourning the Queen's passing. Hong Kong followed US-listed Chinese stocks south but didn't fall as far, which should lead to a rebound in US trading. Fed Chair Powell's tough language on future hikes weighed on risk assets. China's currency fell -0.37% overnight to 7.07 from 7.04 as the Asia dollar index hit a 52 low despite the Bank of Japan "intervening" to stem the collapse in the Yen versus the dollar.

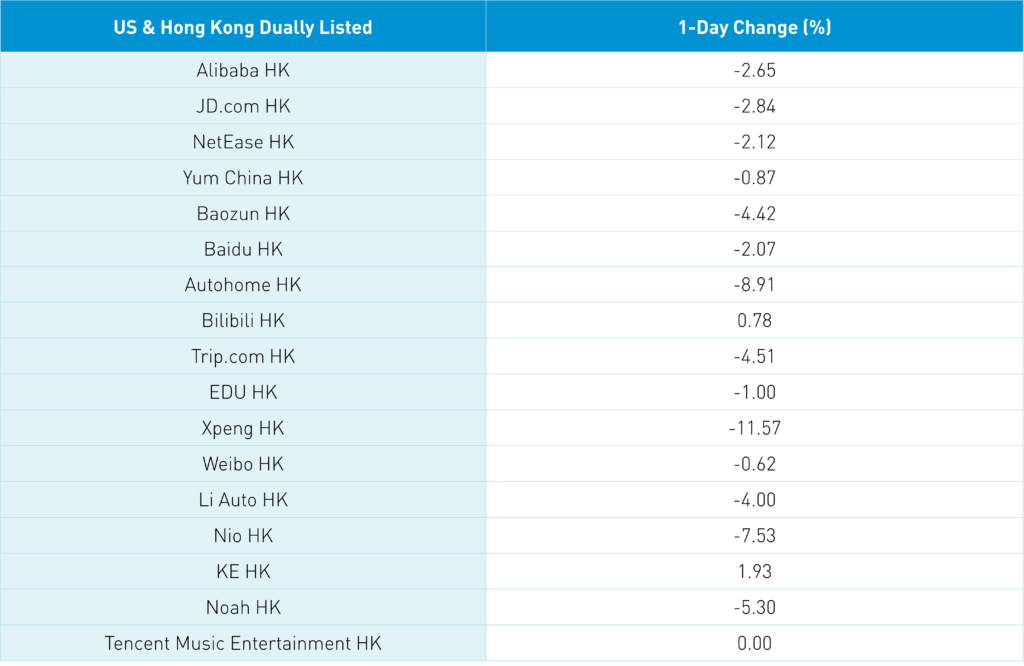

Chatter that President Xi's speech on China maintaining military readiness is said to have weighed on US-China ADRs yesterday though the lack of buyers is the real culprit despite rock bottom valuations and price levels for the space. Reuters is reporting that the "…10 officials from the China Securities Regulatory Commission (CSRC) and the Ministry of Finance (MOF) have arrived in Hong Kong and joined the audit inspection, which started on Monday…". Remember, delisting risk has kept active managers from overweighting/holding the names and defending the names in sell-offs like yesterday. Dutch listed and early investor in Tencent, Prosus' pace of selling in Tencent slowed slightly as the company bought back its shares which is a positive.

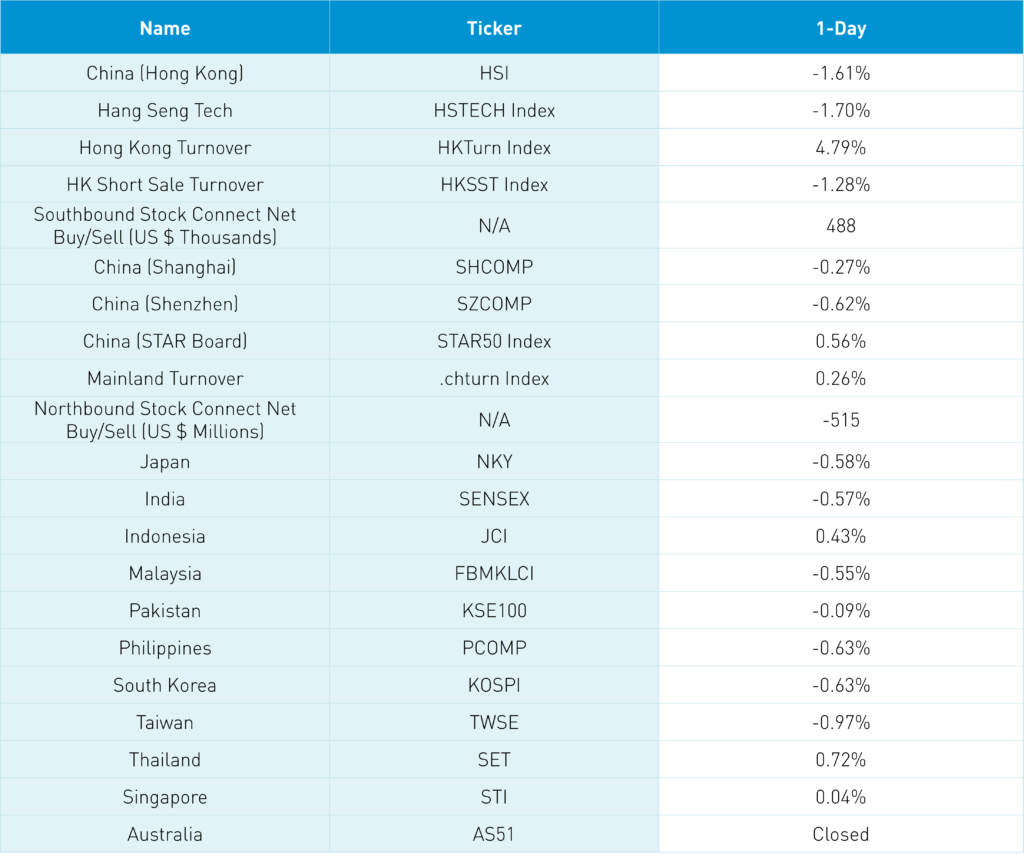

Trip.com (TCOM US, 9961 HK) reported mixed Q2 results after the US close though a positive outlook should help today. TCOM will also benefit from news overnight that Hong Kong's visitor policies will be amended in October instead of November as the city prepares to open up to visitors. The Hang Seng Index is approaching the big round number of 18,000, while the Shanghai Composite is sitting near the 3,100 level. Breaching these levels is meaningless but psychologically not sound. It could be time for more significant policy announcements to boost investor confidence. Hong Kong shorts continued to press their bets as Tencent had 26% of its volume sold short, Meituan 25%, Alibaba HK 17%, and JD.com HK 35%. Mainland investors bought a healthy $488mm of Hong Kong stocks today via Southbound Stock Connect, as it is good to see someone buy the dip. Mainland markets held up better than Hong Kong though foreign investors sold -$516mm of Mainland stocks via Northbound Stock Connect. Interesting that real estate stocks have been off despite relaxed Mainland property buying rules. After the close, it was reported that Premier Li presided over a State Council meeting focused on the economy.

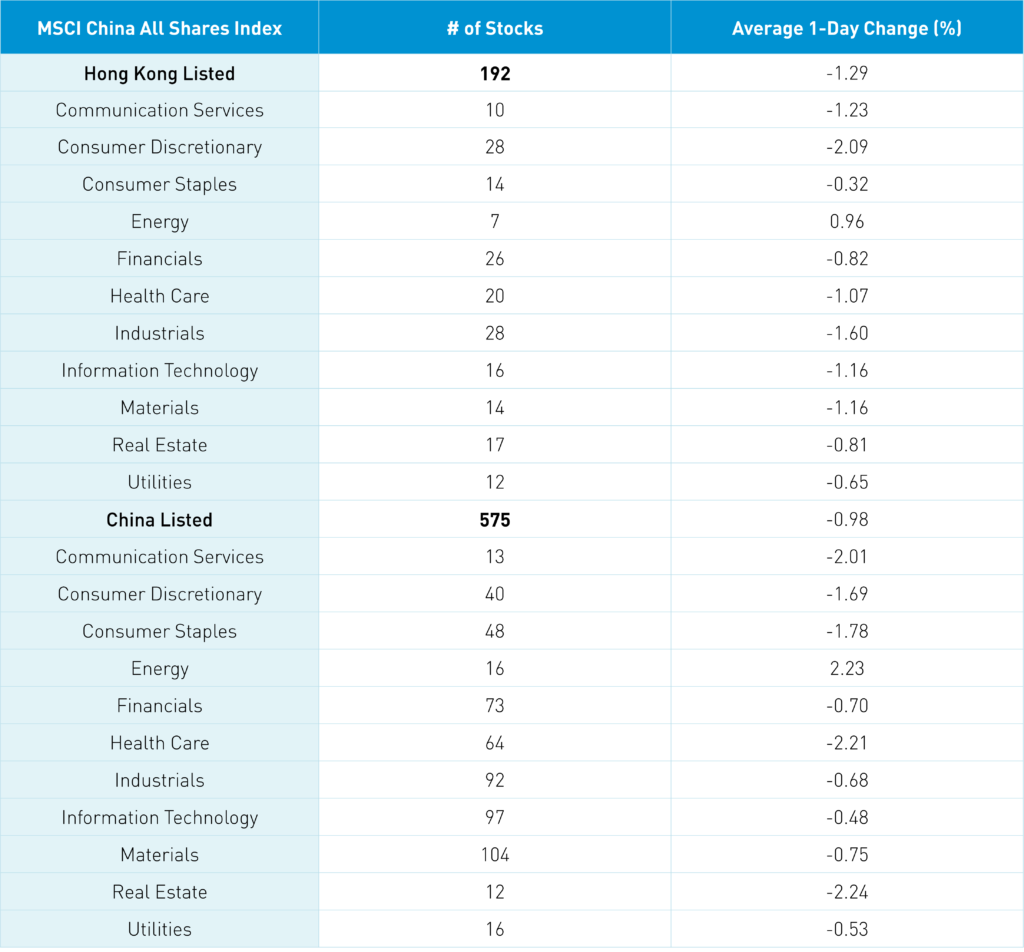

The Hang Seng and Hang Seng Tech fell -1.61% and -1.7% on volume +4.79% from yesterday, which is 67% of the 1-year average. 90 stocks advanced while 401 stocks fell. Main Board short volume fell by -1.27% from yesterday, 79% of the 1-year average, as short trading accounted for 20% of total turnover. Value factors outperformed growth today as large caps outpaced small caps. Energy was the only sector in the green +0.96% while bottom performers were discretionary -2.09%, industrials -1.6% and communication -1.23%. Top sub-sectors included online education, coal, and steel, while liquor, auto, and retail were among the worst. Southbound Stock Connect volumes were light/moderate as Mainland investors bought $488mm of Mainland stocks with Tencent as a moderate buy, Meituan as a moderate/small sell, Sunny Optical as a small sell, and Xpeng as a small buy.

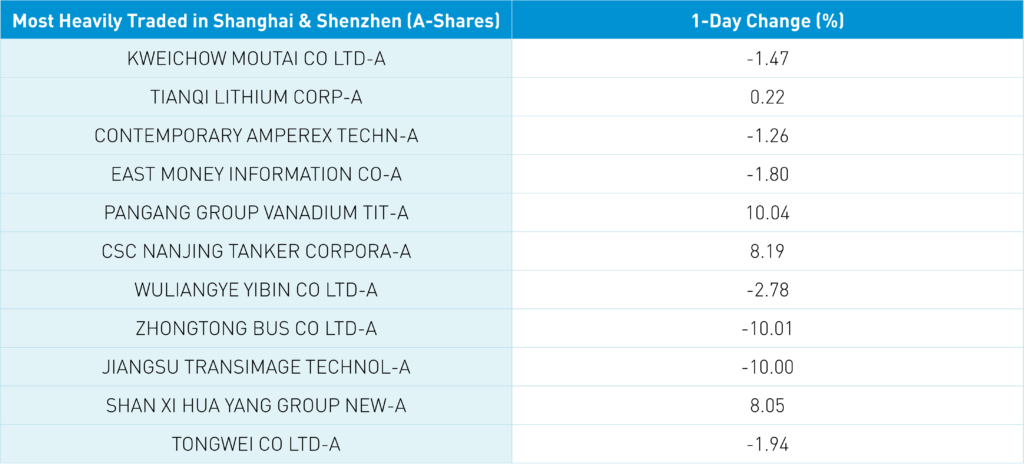

Shanghai, Shenzhen, and STAR Board were off -0.27%, -0.62%, and +0.56% on volume +0.26%, which is 63% of the 1-year average. 1,559 stocks advanced while 2,956 stocks declined. Value and growth factors were mixed, while large caps outperformed small caps. Energy was the only positive sector +2.39%, while real estate -2.09%, healthcare -2.06%, and communication -1.86%. Top sub-sectors included coal, solar, and military/defense names, while pharma, travel, aviation, and EV were among the worst. Northbound Stock Connect volumes were light/moderate as foreign investors sold -$516mm of Mainland stocks today. Treasury bonds sold off slightly, CNY fell -0.37% versus the US $ to 7.07, and copper eased -0.26%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 7.08 versus 7.05 yesterday

- CNY/EUR 6.98 versus 6.99 yesterday

- Yield on 10-Year Government Bond 2.65% versus 2.65% yesterday

- Yield on 10-Year China Development Bank Bond 2.80% versus 2.79% yesterday

- Copper Price -0.26% overnight