PCAOB Auditors Leave Hong Kong as Zero COVID Rollback Rumor Rolls On

3 Min. Read Time

Week in Review

- China’s State Council has outlined eight proposals to support the digital economy, and representatives from key financial regulators made comments this week assuring investors that reform and opening up would continue in China despite leadership changes and Xi’s unprecedented third term.

- Markets in Hong Kong and Mainland China saw strong gains on Tuesday thanks to rumors that a government committee has been established to study and plan for a full reopening in China in March of 2023. While officials talked down rumors, evidence suggests the country is gradually scaling back its Zero COVID policy.

- More than 12 cities in China have signed up to distribute an inhalable COVID vaccine developed by CanSino Biologics, sending the company’s shares sharply higher on Wednesday.

- Electric vehicle sales in China have increased by +87% since October last year, according to data released on Thursday, with BYD, Tesla, and General Motors as the leading automakers.

Key News

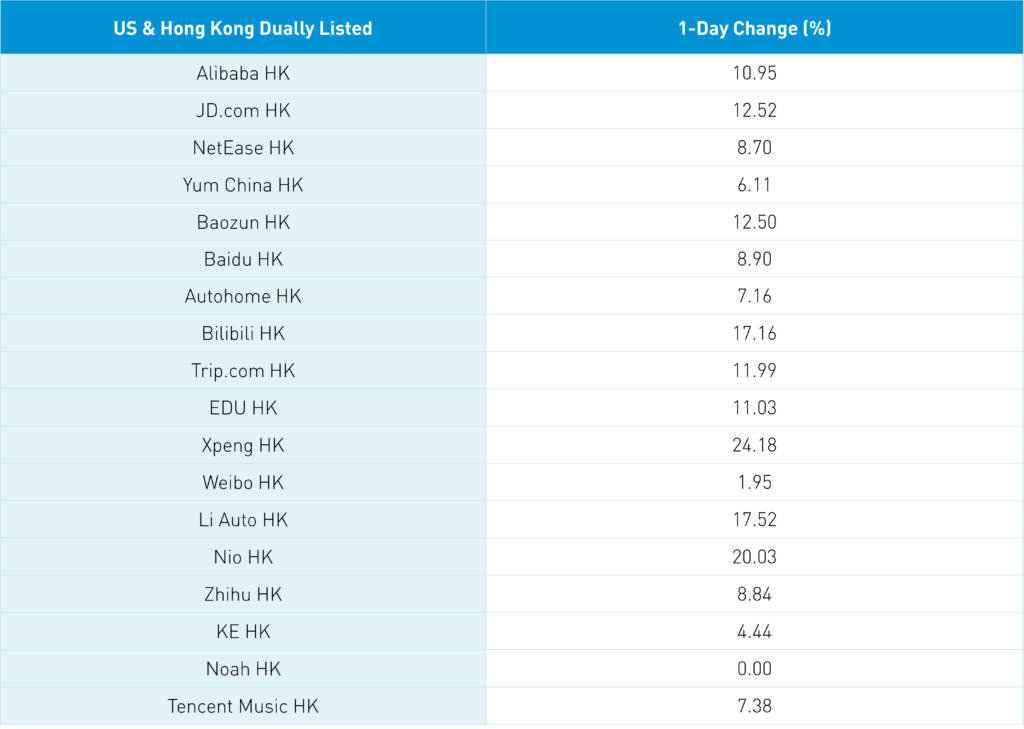

Asian equities had a positive end to a positive week except for Japan, which was off. Meanwhile, Hong Kong and China outperformed today and for the week. Bloomberg News reported during Hong Kong/China trading hours that “Dozens of US Public Company Accounting Oversight Board (PCAOB) inspectors are set to leave Hong Kong as soon as this weekend,…” PCAOB auditors arrived in Hong Kong in mid-September to do onsite audit inspections of PWC, which is Alibaba’s auditor, KPMG, which is Yum China’s auditor, and Deloitte Touch, which is JD.com’s auditor. Markets cheered the exit as a positive sign though we don’t know the outcome of their audit reviews. In theory, the companies should have no problem passing an audit review though the issue has been politicalized.

The market also cheered continued rumors of zero COVID rules being relaxed in order to prioritize the economy. At a global bank’s conference, an ex-official from China’s CDC explained what a COVID dial-back will look like. We shouldn’t expect a pull of the Band-Aid but an incremental/gradual easing. In addition to the removal of restrictions in Hong Kong despite nearly 5k new COVID cases, we had, after the close, German Chancellor Scholz announce BioNTech’s mRNA vaccine would be approved for use among ex-pats living in China. Use may be expanded beyond ex-pats over time? Scholz also announced a $17B Airbus airplane deal with a Chinese aviation company. He had a productive trip benefitting German business interests at the expense of others. We’ve had the rollout of CanSino’s inhalable vaccine approved for use first in Shanghai, followed by a dozen other cities. After the close, Reuters is reporting that inbound China visitors will have their quarantine cut, which could be announced tomorrow.

The Hong Kong market was very strong on VERY high volume of 153% of the 1-year average as 489 stocks advanced while only 21 stocks declined. Hong Kong’s most heavily traded were Tencent +7.77%, Alibab HK +10.95%, and Meituan +5.65%. Mainland investors bought $770mm of HK stock today, with Tencent seeing another strong net buy day. Short volume did increase from yesterday though short volume on internet names was quiet, which is a positive sign. We’ve seen short sellers reload/double down on rebounds, but that has not occurred this week. Mainland markets had a strong day as well on very high volume. Foreign investors bought a healthy +$1.378B of Mainland stocks today. Foreign favorites had a strong day as mega-caps had a strong day led by China’s most heavily traded Kweichow Moutai +5.35%, CATL +5.28%, and Tianqi Lithium +8.47%.

The PCAOB auditors should stay for at least one day of the Hong Kong Sevens rugby tournament after a month and a half in Hong Kong IMO. They deserve a rest!

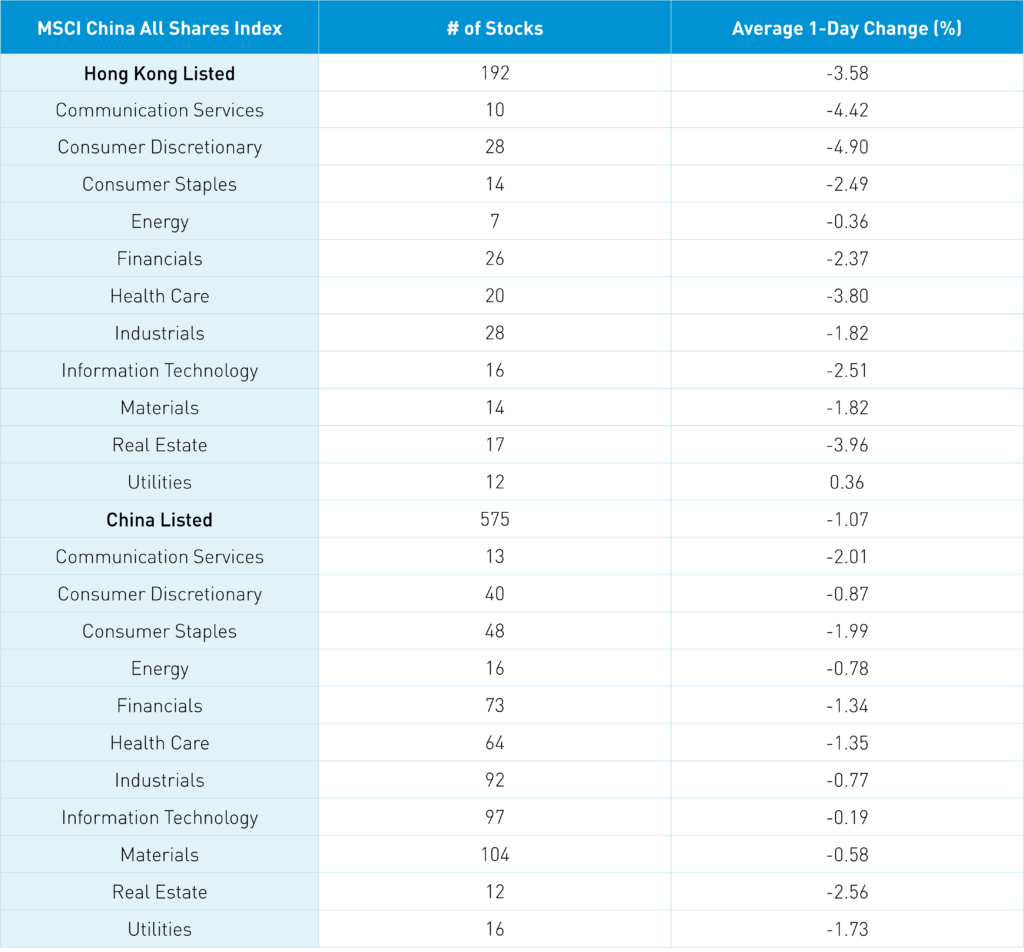

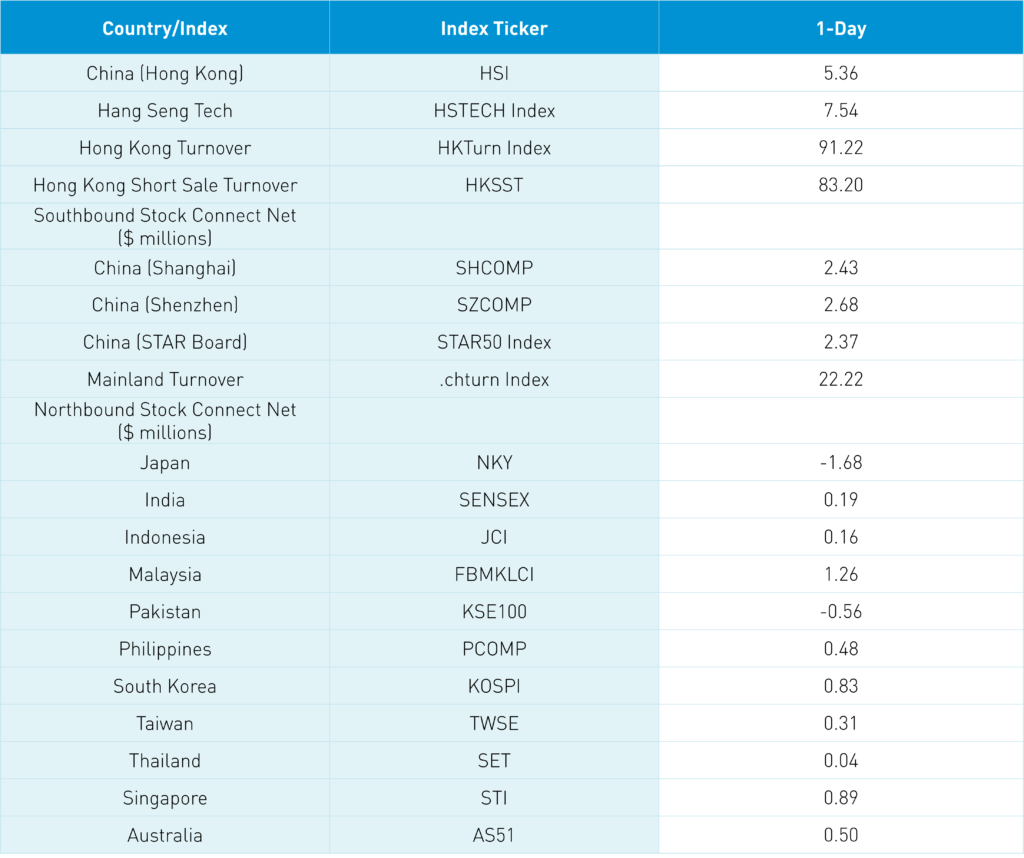

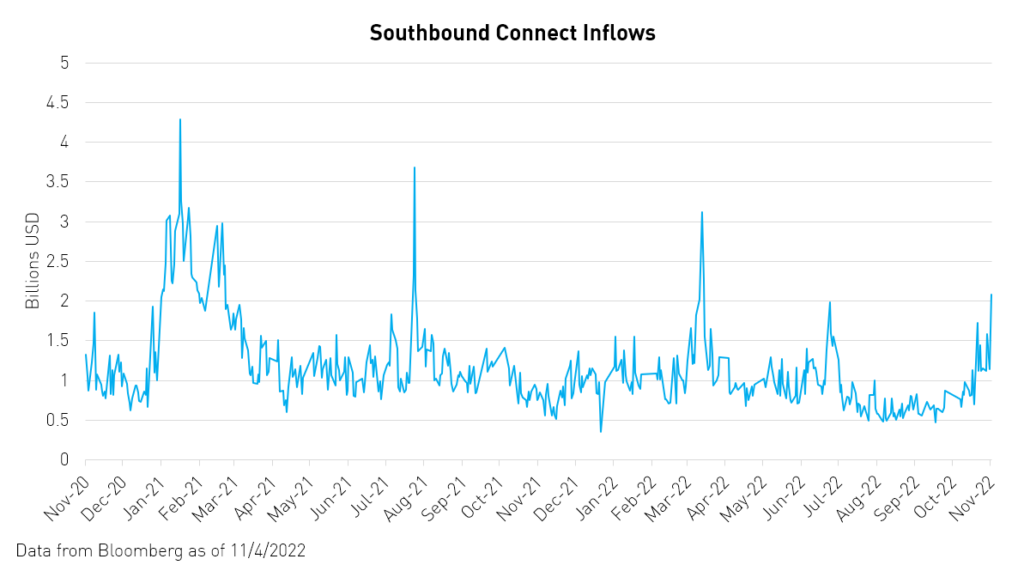

The Hang Seng and Hang Seng Tech Index gained +5.36% and +7.54% on volume +91.22% from yesterday, which is 153% of the 1-year average. 489 stocks advanced, while 21 declined! Main Board short turnover increased +83.2% from yesterday, which is 124% of the 1-year average, as 14% of turnover was short turnover today. Growth and value factors were mixed as small caps outpaced large caps. All sectors were positive, with real estate +9.15%, discretionary +8.95%, and communication +8.09%. The top sub-sectors were auto, retailers, and software, with no sub-sectors down. Southbound Stock Connect volumes were very high as mainland investors bought $770mm of Hong Kong stocks, with Tencent seeing large net buying while Meituan, CanSino Biologics, Wuxi Biologics, and Kuaishou also net buys.

Shanghai, Shenzhen, and STAR Board rose +2.43%, +2.68%, and +2.37% on volume +22.22% from yesterday, which is 111% of the 1-year average. 3,974 stocks advanced, while 632 stocks declined. Growth factors outperformed value factors as large caps outpaced small caps. All sectors were positive, with discretionary +6.06%, staples +6.04%, and materials +5.27%. The top sub-sectors were restaurants, liquor, and marine/shipping while telecom was off. Northbound Stock Connect volumes were high as foreign investors bought $1.378B of Mainland stocks. Treasury bonds sold off, CNY appreciated +0.75% versus the US dollar to 7.24 and copper +0.25%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.32 yesterday

- CNY per EUR 7.13 versus 7.13 yesterday

- Yield on 10-Year Government Bond 2.70% versus 2.68% yesterday

- Yield on 10-Year China Development Bank Bond 2.82% versus 2.79% yesterday

- Copper Price +0.25% overnight