Guangzhou Traffic & Metro Usage Confirms New Government COVID Policies, Week in Review

3 Min. Read Time

Week in Review

- US and Hong Kong-listed internet stocks outperformed this week on reopening speculation and earnings. Pinduoduo and Bilibili reported better-than-expected Q3 results this week as the former grew revenue by +65% year-over-year.

- Protests across China garnered significant media attention this week following an apartment building fire that killed ten with claims that covid barriers slowed firefighters' response. This will likely accelerate reopening while the government will seek to maintain dynamic zero COVID where possible.

- The National Health Commission discussed a campaign to vaccinate the elderly amid a symposium this week on reducing virus restrictions, which included remarks from Vice Premier Sun Chunlan.

- China’s November official manufacturing and non-manufacturing PMIs came in below estimates, and October’s figures, partially due to slowing external demand.

Friday’s Key News

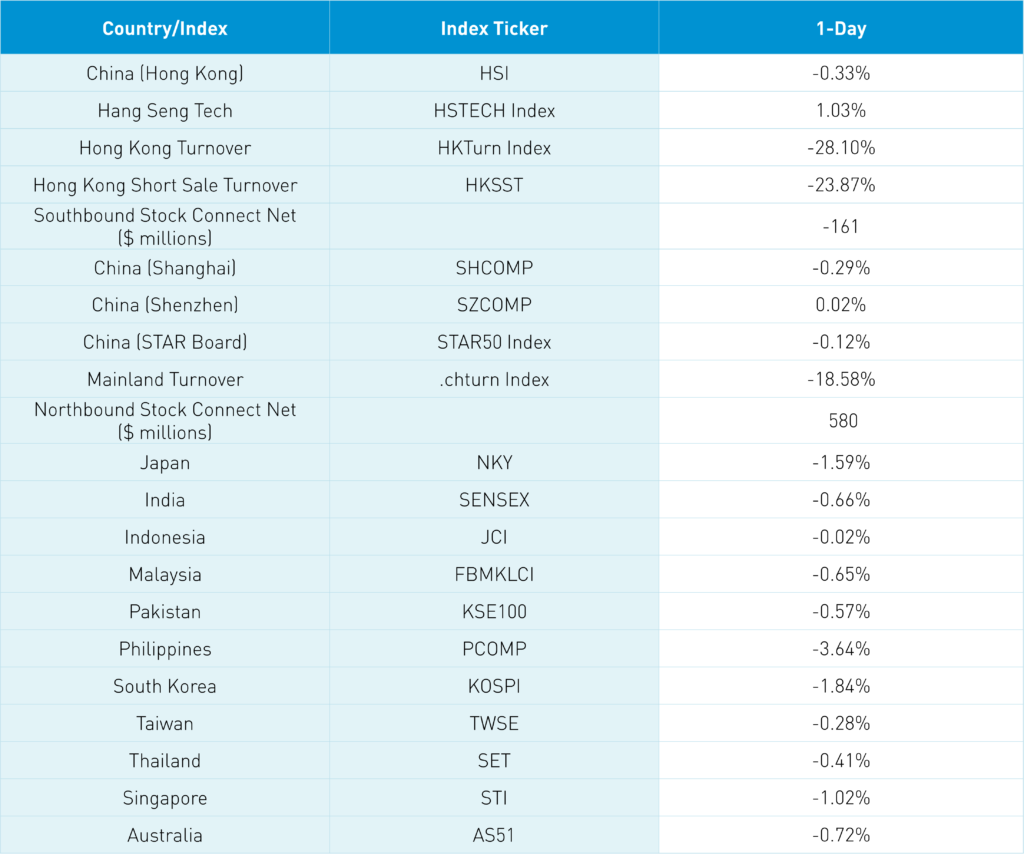

Asian equities ended a strong week off slightly in a quiet session as investors waited for today’s US payroll release. What a week and a month, for that matter.

Foreign investors added $3.7 billion worth of Mainland equities through Northbound Stock Connect. The Renminbi appreciated versus the US dollar this week, outperforming the Asia dollar index’s gain.

We released our “Back to Business” research piece yesterday, please click here to view. The article discusses how we believe China will address the “Big Three” issues for investors: US-China relations, zero COVID, and real estate.

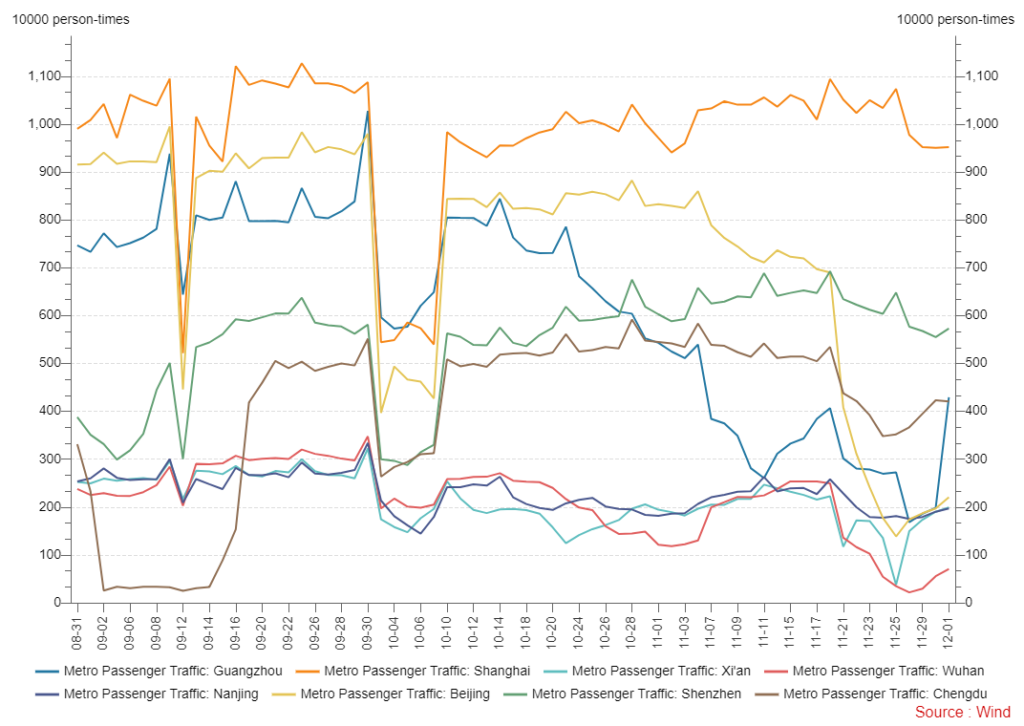

Today there were 4,233 new cases reported, along with 30,539 asymptomatic cases. However, we continue to see the loosening of zero COVID policies. For evidence, a 62-year-old government official announced that he was comfortable with the risk of contracting COVID. Meanwhile, our China Major City Mobility Tracker showed an increase in Guangzhou’s metro and vehicle traffic, confirming the government’s new stance through data. Remember that Guangzhou was an area of focus for COVID policies due to the city’s economic importance, so the city’s reopening bodes well for the rest of the country.

The European Council’s President Charles Michel met with President Xi in Beijing as the government’s charm campaign since the Party Congress in October appears to be continuing. Germany’s Chancellor Olaf Scholz traveled to China just last month.

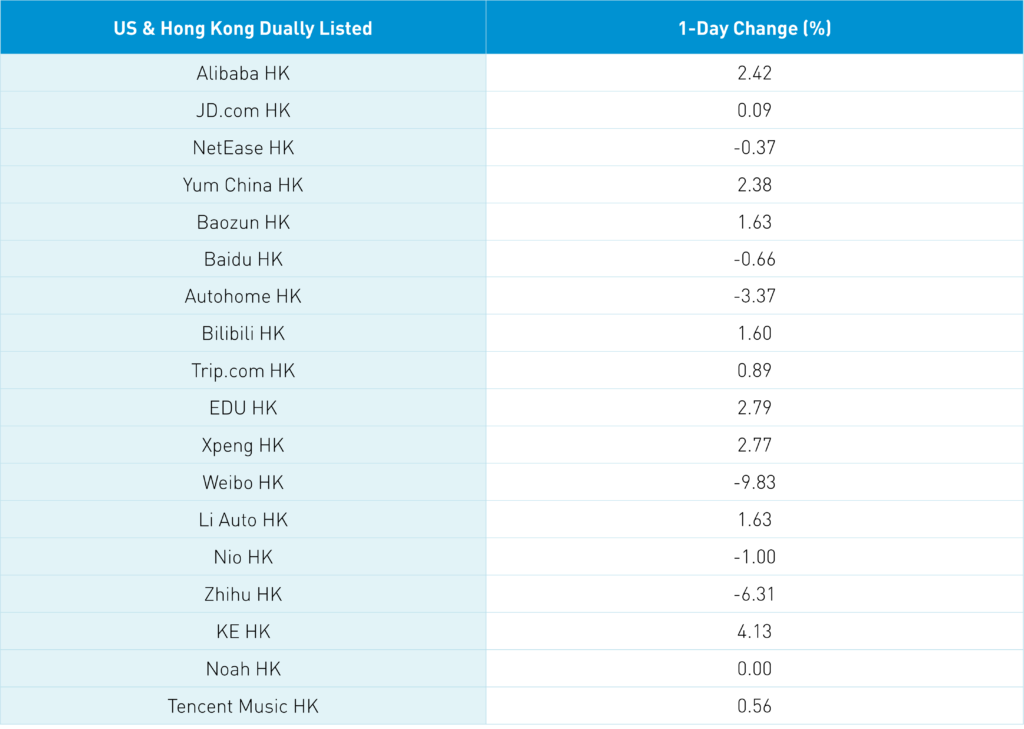

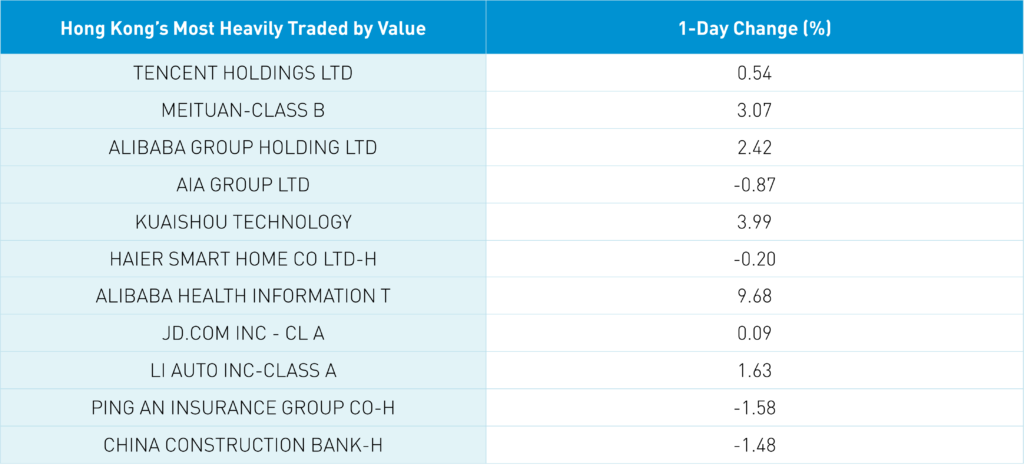

Hong Kong-listed internet stocks had a good day despite the markets being off on no news as Hong Kong’s most heavily traded stocks by value included Tencent, which gained +0.54%, Meituan, which gained +3.07%, and Alibaba, which gained +2.42%. Meanwhile, Mainland markets were mixed on light volumes.

Personal pension funds, which are similar to the US’ Individual Retirement Accounts (IRAs), were rolled out yesterday in thirty-one cities. I will do more research and see how these new investment vehicles may impact equity markets. That’s my weekend homework assignment!

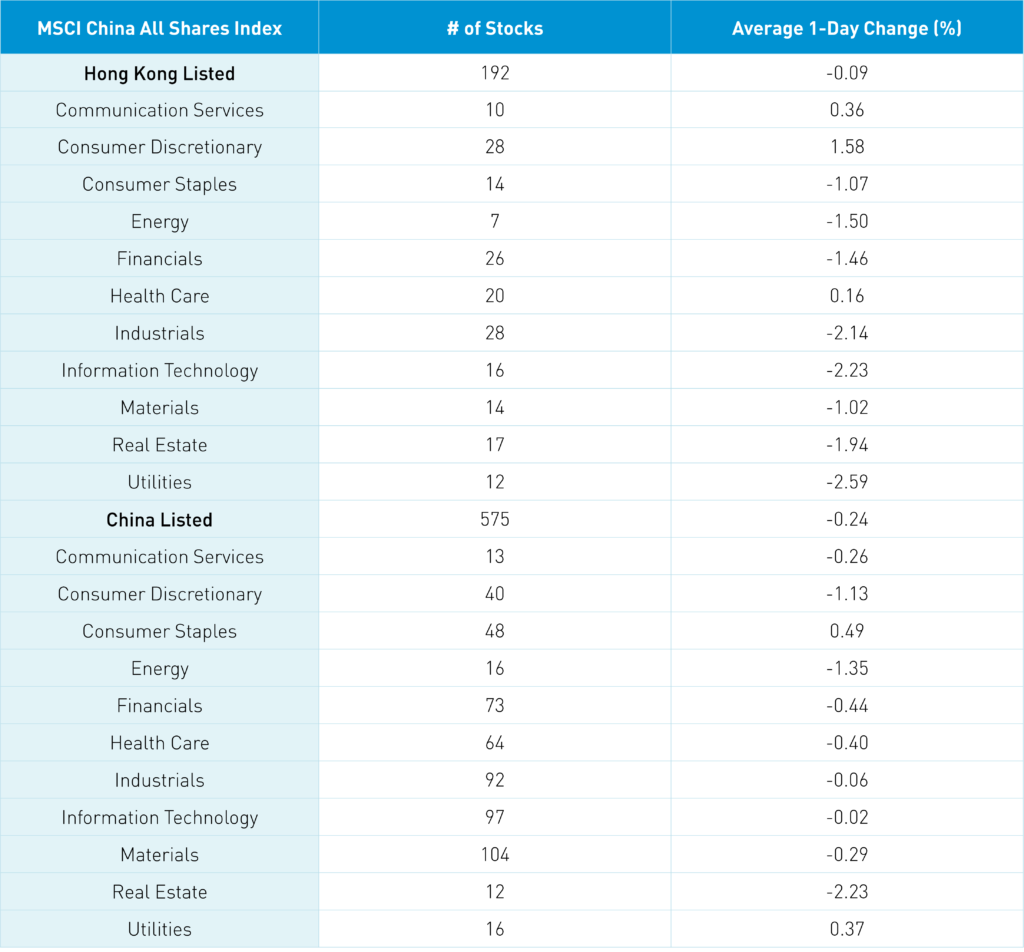

The Hang Seng and Hang Seng Tech indexes diverged to close -0.33% and +1.03%, respectively, on volume that decreased -28.1% from yesterday, which is 116% of the 1-year average. 176 stocks advanced, while 313 declined. Main Board short sale turnover declined -23.92% from yesterday, which is 101% of the 1-year average, as 15% of the total turnover was short. Growth and value factors were both down as small caps “outperformed” large caps with both down. The top-performing sectors were consumer discretionary, which gained +1.62%, communication, which gained +0.4%, and healthcare, which gained +0.2%. Meanwhile, utilities fell -2.55%, tech fell -2.19%, and industrials fell -2.1%. The top-performing subsectors were healthcare equipment, food, and retail. Meanwhile, semiconductors, utilities, and capital goods were among the worst. Southbound Stock Connect volumes were light as mainland investors sold -$161 million worth of Hong Kong stocks as Tencent and Kuaishou were slight net buys, while Meituan and Xpeng were small net sales.

Shanghai, Shenzhen, and the STAR Board diverged to close -0.29%, +0.02%, and -0.12%, respectively, on volume that decreased -18.58% from yesterday, which is 90% of the 1-year average. 2,866 stocks advanced, while 1,709 stocks declined. The top-performing sectors were consumer staples, which gained +0.63%, utilities, which gained +0.51%, and technology, which gained +0.12%. Meanwhile, real estate fell -2.1%, energy fell -1.21%, and consumer discretionary fell -0.99%. The top-performing subsectors were textiles, land transportation, and energy equipment, while shipping, precious metals, and real estate were among the worst. Northbound Stock Connect volumes were light as foreign investors bought $580 million worth of Mainland stocks. CNY appreciated slightly versus the US dollar, the Treasury yield curve steepened slightly, and copper was off -0.27%.

China Major City Mobility Tracker

Interesting to see that congestion in both Guangzhou and Zhengzhou picked up while metro usage picked up in Guangzhou as well.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.05 versus 7.05 yesterday

- CNY per EUR 7.38 versus 7.40 yesterday

- Yield on 1-Day Government Bond 1.20% versus 1.40% yesterday

- Yield on 10-Year Government Bond 2.87% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.00% versus 3.00% yesterday

- Copper Price -0.27% overnight