Mainland Investors Buy the Dip as COVID Rollback Rolls On

3 Min. Read Time

Key News

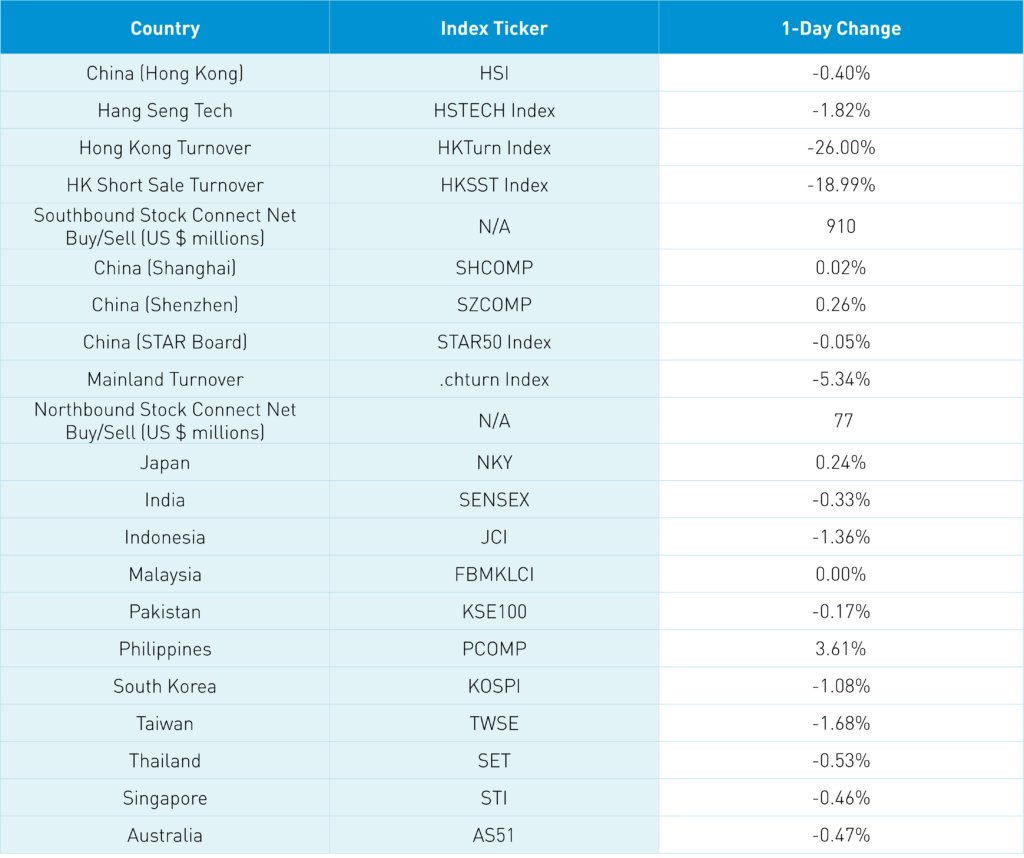

Asian equities were largely lower, as the Philippines had a great day and China posted a small gain.

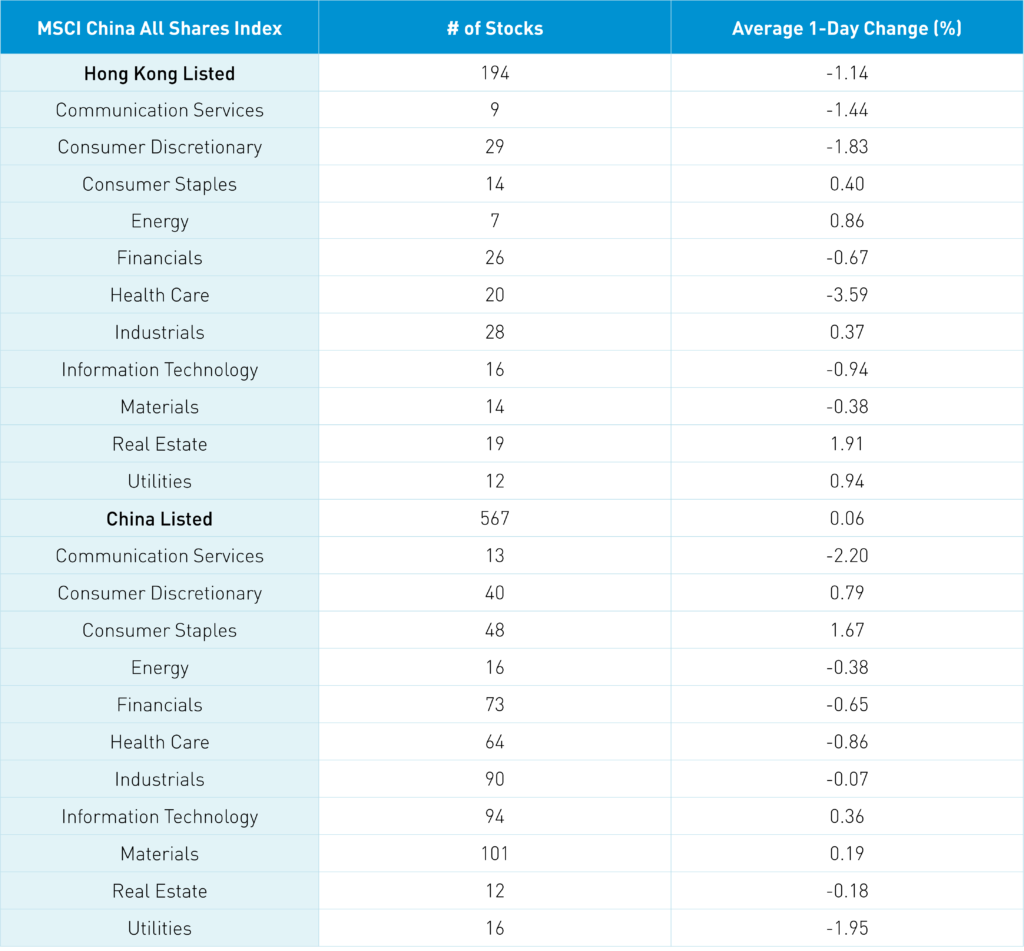

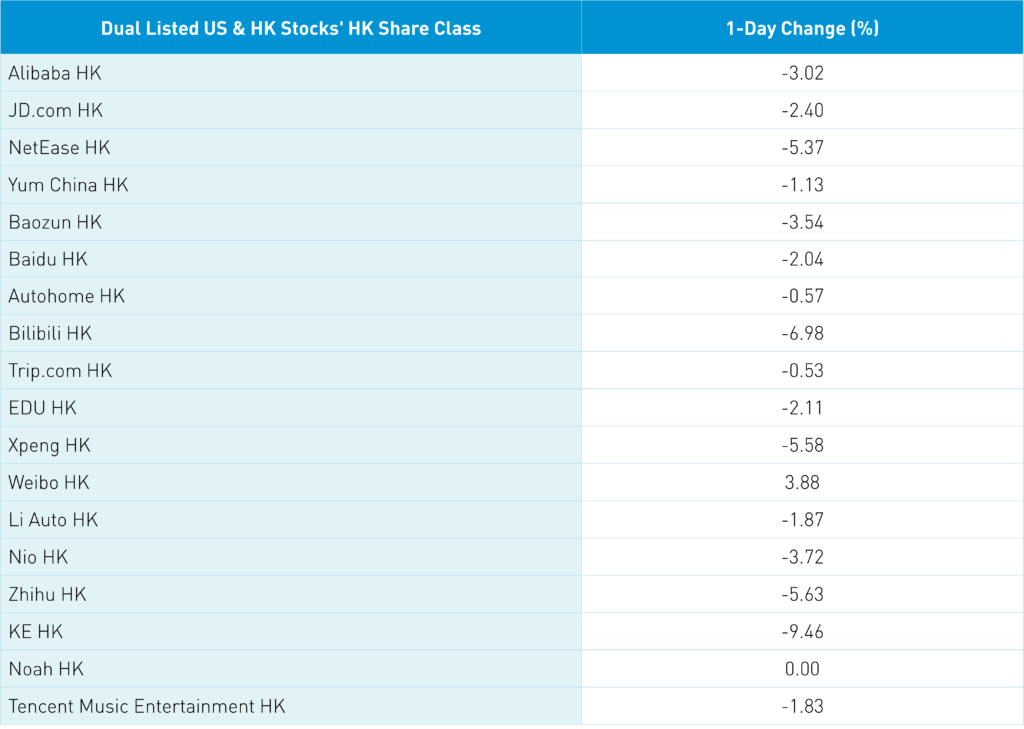

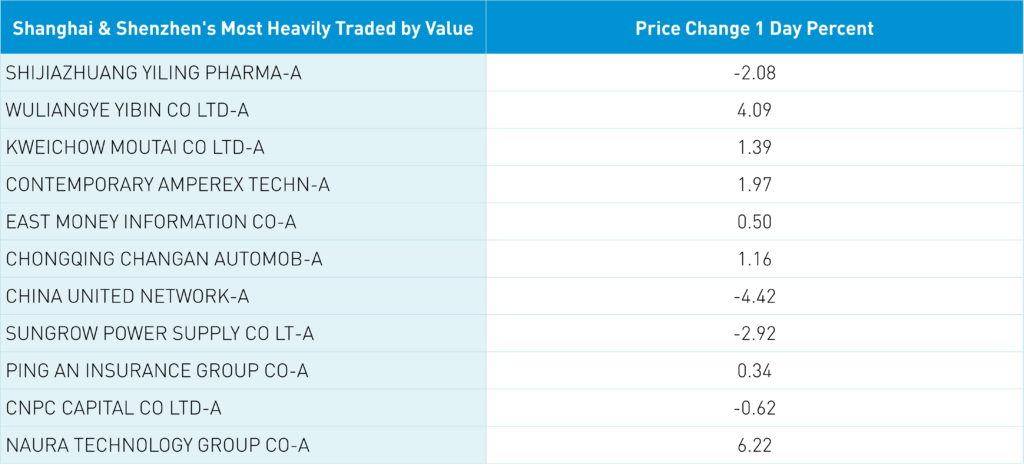

Hong Kong was off overnight though not nearly as much as US listed China ADRs fell yesterday which should lead to a rebound in the ADRs today while the Shanghai and Shenzhen managed small gains. Mainland investors bought today’s Hong Kong dip with a healthy $910 million of Hong Kong stocks bought today via Southbound Stock Connect. Hong Kong’s most heavily traded by value were Tencent -0.7%, Meituan -0.29% and Alibaba HK -3.02%. Mainland China was led by growth stocks favored by domestic and foreign investors and reopening plays with liquor stocks having a strong day. Healthcare is off as investors fund their reopening positions. Real estate was the top sector in Hong Kong based on yesterday’s news on new bank support though we did see another equity issuance announced.

China continued to roll back COVID measures across the country as Beijing’s municipal government announced negative COVID tests won’t be necessary to enter public areas. In addition, twenty cities rescinded travel restrictions for buses and subways. In watching financial TV yesterday, not one of four portfolio managers would invest in China today. I love it as such skepticism fuels bull markets. It is anticipated that new rollback measures will be announced tomorrow. Yes, there will be fits and starts to China’s COVID roll back as today alone there will be 4,988 new COVID cases along with new 22,859 asymptomatic cases. We also have an uptick in communication between the US and China as Bloomberg News has an article making the rounds this morning that “Beijing has begun cooperating with US efforts to ensure American technology isn’t routed to China’s military…”. Logical steps to ensure that semiconductor chips go into a video game console versus a nuclear warhead.

Published back in 2007, Peter Tertzakian’s fabulous book “A Thousand Barrels a Second” shaped my views of traditional energy and clean technology. By providing a history of energy transitions, the book highlights the difficulty in jumping from one energy source to a new one. It doesn’t mean these transitions don’t happen, but they take time. I fully believe in clean technology though I understand the impact infrastructure or the lack of it has on that transition. Clean energy adoption will help climate change though 100% impact jobs, towns, and even states and countries. Anyone notice where Saudi Arabia’s sovereign wealth fund is investing? It has to prepare for what the world’s energy demand will look like in a hundred years. China is well known for exporting deflation though its role in exporting clean energy like solar panels, EVs, and windmills is underestimated. Is an element of the negative China news driven by a lack of investment to prepare those jobs, towns, and states? Maybe it isn’t a defense argument, but the risk posed by China’s exports? Something to think about.

The Hang Seng and Hang Seng Tech eased -0.4% and -1.82% on volume -26% from yesterday which is 134% of the 1-year average. 237 stocks advanced while 256 stocks declined. Main Board short turnover declined -19.08% from yesterday which is 119% of the 1-year average as 15% of turnover was short turnover. Value factors outperformed growth factors while small caps outperformed large caps. Top sectors were real estate +1.9%, utilities +0.93%, and energy +0.85% while closing lower were healthcare -3.6%, discretionary -1.84%, and communication -1.45%. Top sub-sectors were household products, real estate, and food while pharma, retailers, and media were among the worst. Southbound Stock Connect volumes were 2X the 1-year average as Mainland investors bought a healthy $910 million of Hong Kong stocks with Meituan a small net sell, Tencent, and Kuaishou small net sells.

Shanghai, Shenzhen, and STAR Board were mixed +0.02%, +0.26%, and -0.05% on volume -5.34% from yesterday which is 105% of the 1-year average. 1,561 stocks advanced while 3,066 stocks declined. Growth and value factors were mixed as large caps outperformed small caps. Top sectors were staples gaining +1.68%, discretionary up +0.8%, and tech closing higher +0.37% while communication fell -2.19%, utilities fell -1.95%, and healthcare fell -0.85%. Top sub-sectors were liquor, restaurants, and chemicals while telecom, construction, and gas struggled. Northbound Stock Connect volumes were moderate as foreign investors bought $77 million of Mainland stocks. CNY fell -0.4% versus the US dollar to 6.99, Treasury bonds fell, and copper eased -0.48%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.99 versus 6.96 yesterday

- CNY per EUR 7.35 versus 7.34 yesterday

- Yield on 10-Year Government Bond 2.92% versus 2.89% yesterday

- Yield on 10-Year China Development Bank Bond 3.04% versus 3.02% yesterday

- Copper Price -0.48% overnight