CPI under 2% in China as Clean Tech & EV Outperform

3 Min. Read Time

Key News

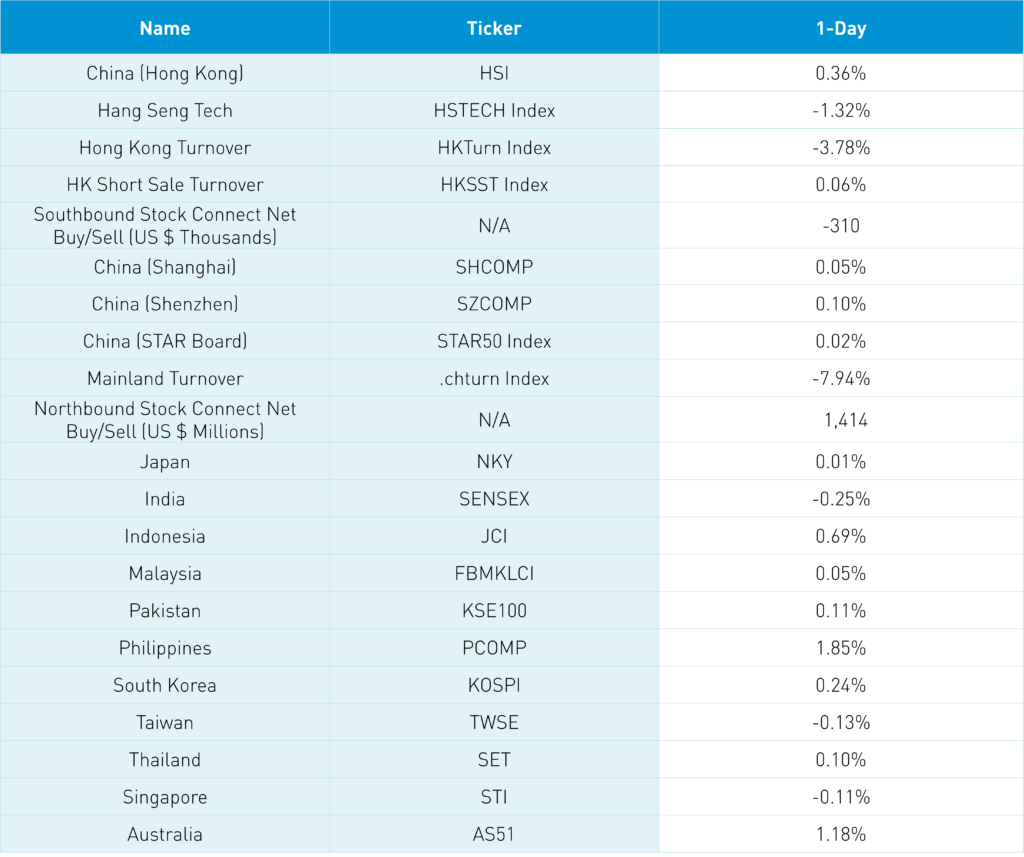

Asia equities were largely higher except for Singapore and India’s small pullback in advance of the US’ highly anticipated CPI release. Overnight China’s December CPI was released at +1.8% versus November’s +1.6%, meeting expectations of 1.8%, while PPI was -0.7% versus November’s -1.3%, which was light versus expectations of -0.1%. The inflation release gives policy ample room to continue monetary easing and pro-consumption fiscal policies against the backdrop of low consumer inflation. CNY appreciated overnight versus the US dollar closing +0.23% at 6.74.

Hong Kong and China's choppy sessions swing from positive to negative though closing positive. The Hang Seng Index turned from -0.99% to +1.23%, closing +0.36%, while the Hang Seng Tech was off +1.13%, -2.78% at one point though it closed at -1.32%. Today was almost the opposite of yesterday, as value sectors had a good day while growth stocks/sectors struggled. Hong Kong’s most heavily traded were Tencent -2.62% on a notable sell day from Mainland investors via Southbound Stock Connect, Alibaba HK -1.86% and Meiutan -0.57% while JD.com +032% and NetEase +3.73%. The big winner was auto and EV with BYD +5.25%, Nio +0.62%, and Li Auto +1.03% though Xepng -3.64% on an analyst downgrade. Short activity was moderate though NetEase Hong Kong’s turnover was short turnover versus 11% yesterday.

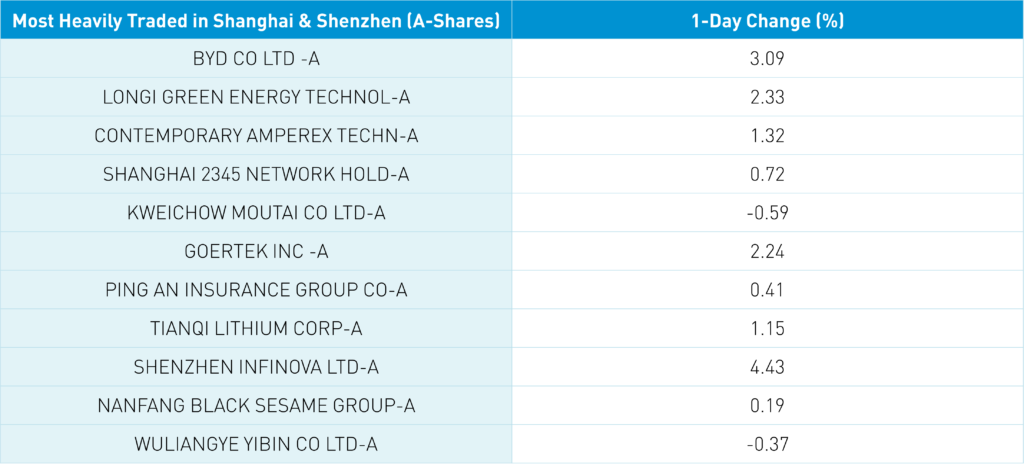

Cleantech, including electric vehicles, were the winners in the Mainland, as evidenced by the most heavily traded stocks: BYD +3.09%, LONGi Green Energy +2.33%, and CATL +1.32%. Foreign investors bought a healthy +1.414B of Mainland stocks today via Southbound Stock Connect. A Mainland media source released an article titled “China’s Regional Governments Strong Signal that Crackdown on Internet Giants Is over” after Jiangsu, Shandong, Shaanxi, Henan, Zhejiang, and Hunan provinces “…have all recently released policies flagging their support for the development of Internet platform economies,…”. The link to the article was posted on Twitter which is ahern_brendan. More real estate support from the PBOC and CBIRC though real estate was the worst performer in both Hong Kong and China.

Interestingly one broker noted the skepticism on the rally we’ve seen as they aren’t seeing buyers. That’s the pain trade higher thesis. There is a lot of scar tissue after the challenging markets in 2021 and most of 2022. I remember a story about the great commodity trader Andrew Hall, who was once called “the most successful oil trader of his generation,” who was interviewed about his bearish oil view. When they went to publish the article, the journalist touched base to confirm his quotes only to discover he was no longer short oil but long oil! Why? Hall noted his lack of emotional attachment to his positions when market conditions changed. Have you changed? Think most have changed? Me neither! Pain trade higher!

The Hang Seng and Hang Seng Tech diverged, closing +0.36% and -1.32% on volume -3.78% from yesterday, 127% of the 1-year average. 228 stocks advanced, while 250 declined. Main Board short turnover increased +0.06% from yesterday, which is 117% of the 1-year average, as 16% of turnover was short turnover. Growth and value factors were mixed as large caps outpaced small caps. The top sectors are energy +1.68%, industrials +1%, and financials +0.86%, while real estate -2.04%, communication -2.02%, and healthcare -0.8%. The top sub-sectors were auto, energy, and insurance, while software, healthcare equipment/services, and consumer services were among the worst. Southbound Stock Connect volumes were light as Mainland investors sold -$310mm of Hong Kong stock with BYD strong net buying, Xpeng small net buying, Tencent a strong net sell, Kuiashou a moderate net sell, and Meituan a small net sell.

Shanghai, Shenzhen, and STAR Board gained +0.05%, +0.1%, and +0.02% on volume -7.94% from yesterday, which is 75% of the 1-year average. 2,148 stocks advanced, while 2,388 stocks declined. Growth factors outperformed value factors as large caps outpaced small caps. The top sectors were communication +1.1%, energy +0.96%, and financials +0.84%, while real estate -1.69% and staples -0.18%. The top sub-sectors were forest, telecom, and auto, while soft drinks, restaurants, and real estate were among the worst. Northbound Stock Connect volumes were light as foreign investors bought a healthy $1.414B of Mainland stocks. CNY had another strong day versus the US dollar +0.23%, closing at 6.74, the Treasury curve steepened, and Shanghai Copper gained +1.84%.

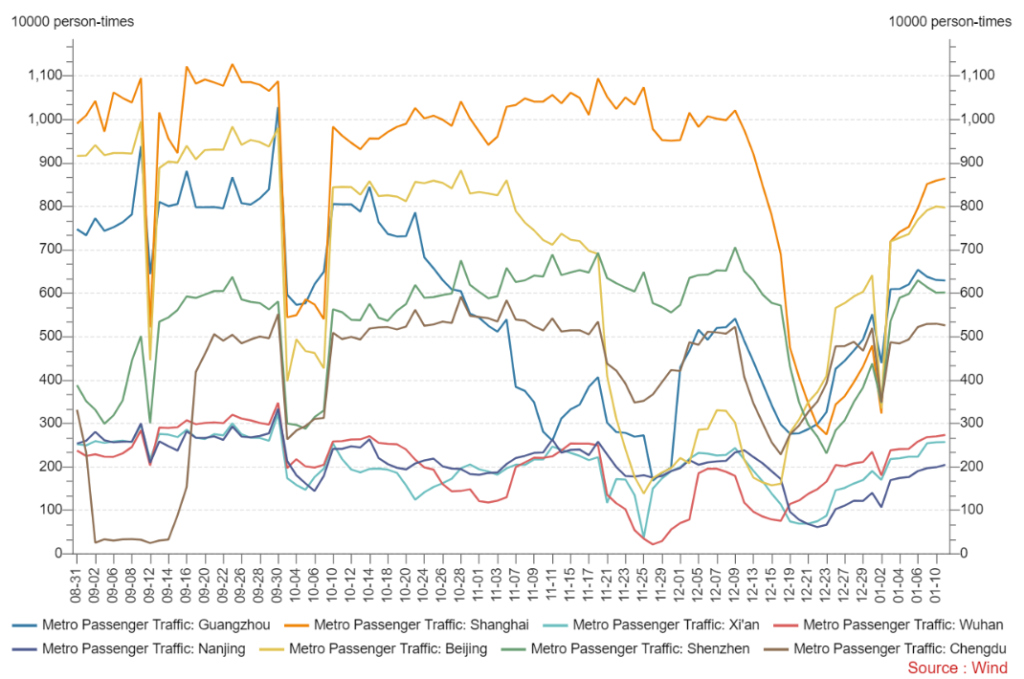

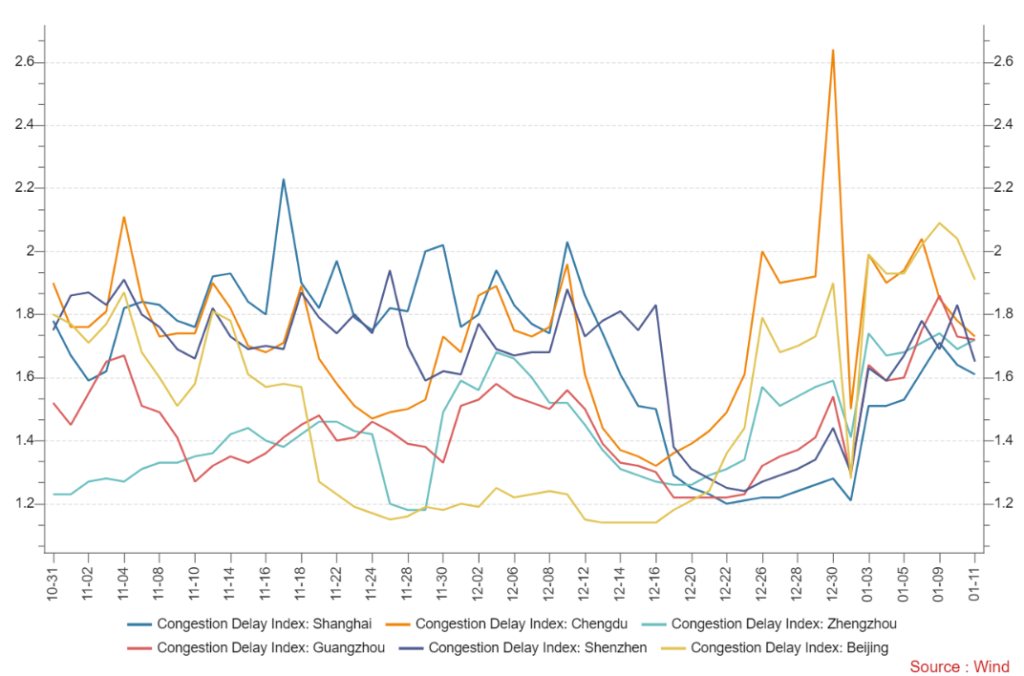

Major Chinese City Mobility Tracker

While subway trends continue to rebound, it is worth noting traffic in several cities has slowed. It is too early for Chinese New Year vacations to be starting. I will investigate further!

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.75 versus 6.77 yesterday

- CNY per EUR 7.27 versus 7.28 yesterday

- Yield on 10-Year Government Bond 2.88% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.00% versus 2.99% yesterday

- Copper Price +1.84% overnight