Markets Rise on Epic Foreign Inflow as Internet Stocks Climb the Wall of Worry, Week in Review

4 Min. Read Time

Week in Review

- China’s December CPI was released at +1.8% versus November’s +1.6%, meeting expectations of 1.8%.

- On Wednesday, The World Bank cut its 2023 global GDP growth forecast in half, though it expects China's GDP growth to be ahead of the pack.

- The China Passenger Car Association released December and 2022 sales data showing that 4 million EVs were sold in China in 2022, 5X more than in the US.

- Jack Ma relinquished most of his stake in financial technology giant Ant Group, paving the way for the final regulatory rubber stamp as well as a potential IPO.

Friday's Key News

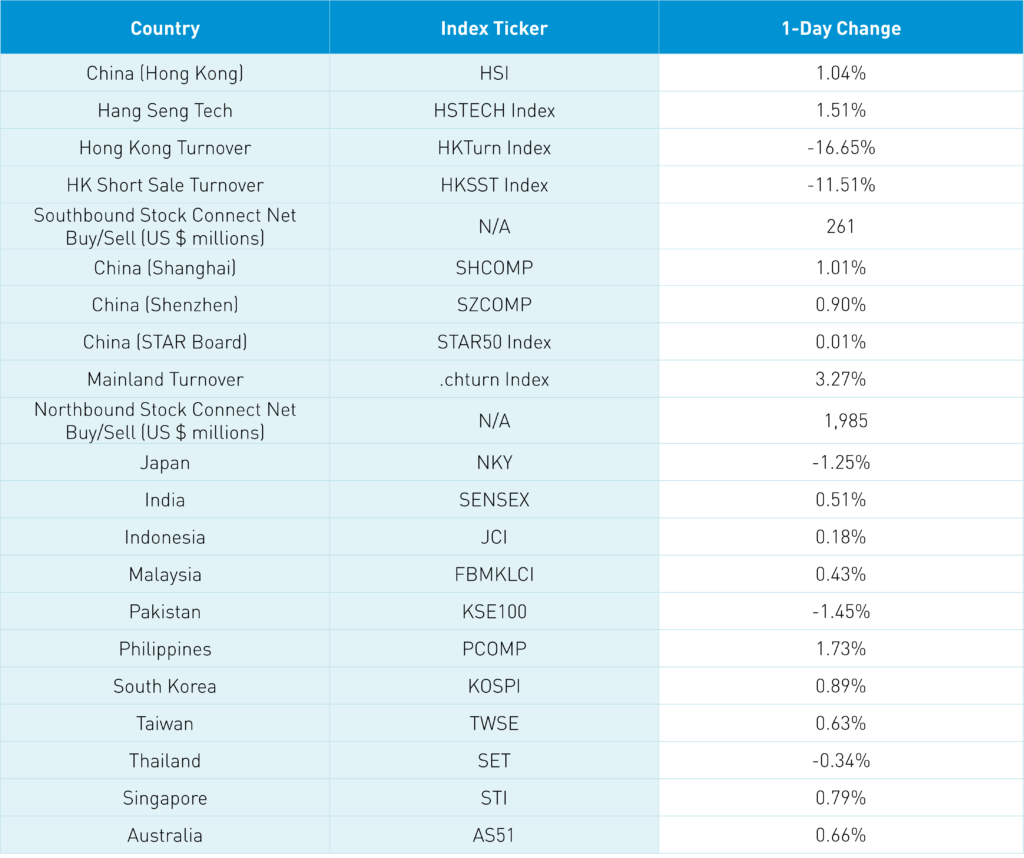

Asian equities ended the week in the green, except for Japan and Thailand, while Hong Kong, China, and the Philippines outperformed.

Global equities have had strong year-to-date performance thus far (knocking on wood). A lot of news overnight! What did our China news risk barometer do? Remember, we use China’s currency as a risk barometer to understand if “news” is impactful/something that should concern us. CNY appreciated +0.17% versus the US dollar to close at 6.72! All the negative Western media headlines? The equity market didn’t care as the Hang Seng gained +1.04%, Hang Seng Tech closed higher by +1.51%, Shanghai finished +1.01%, Shenzhen gained +0.9%, and the STAR Board was up +0.01%.

Right before the open in Hong Kong, the Financial Times released an article titled “China moves to take ‘golden shares’ in Alibaba and Tencent units”. It isn’t until several paragraphs into the article that the source of the article is revealed. Are “separate people briefed on the matter” a credible source? I have no clue, but the key is the market absolutely didn't care despite Western media pushing the FT article out. I don’t see any mention of this in Mainland media as an FYI. If true, there is an argument and an indication that the companies are in the government’s favor as their success would benefit them as well. I would think we could see local provinces supporting the companies though we’ll find out.

Hong Kong was flat, though a little wobbly at open, but rallied later in the session as Reuters reported that “Didi Global’s ride-hailing and other apps back on domestic app stores as soon as next week”. Reuters source? “Five sources told Reuters, in yet another signal that their two-year regulatory crackdown on the technology sector is ending.”

December trade data was released, showing that exports and imports declined year-over-year, though not as deeply as estimated. Remember that we should expect China’s exports to slow as global demand for the world’s factory slows. The export data is also an indication that the global economy is slowing, unfortunately. The import data was weak though falling commodity prices are a factor as, for instance, crude oil imports increased, but the value of oil imports declined due to oil’s price decline.

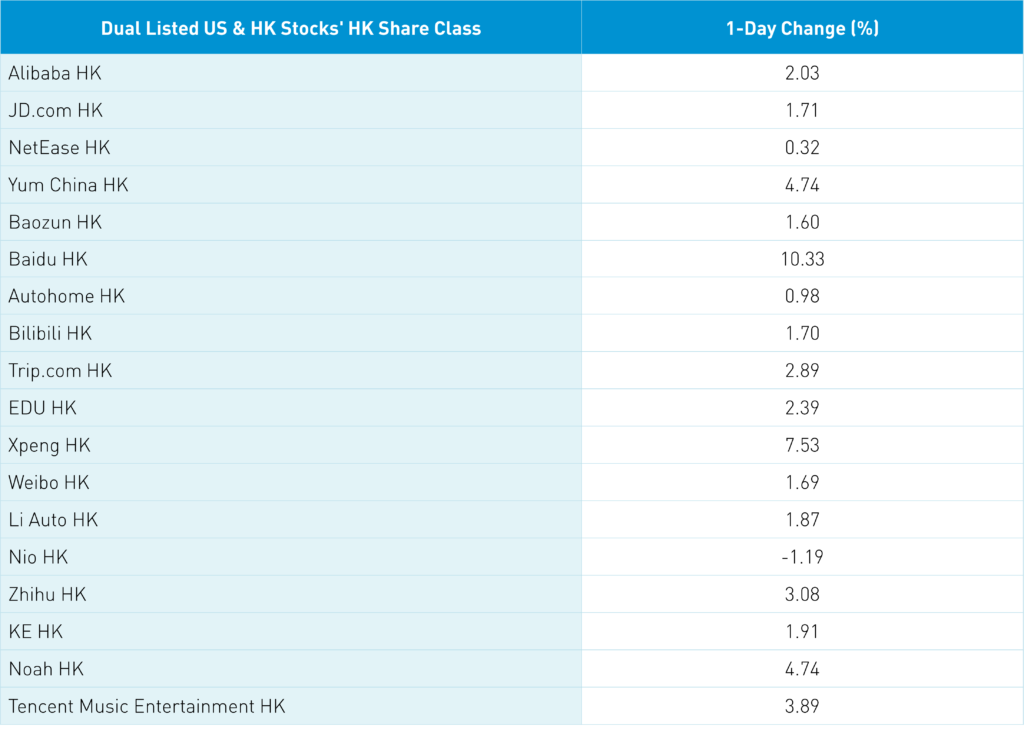

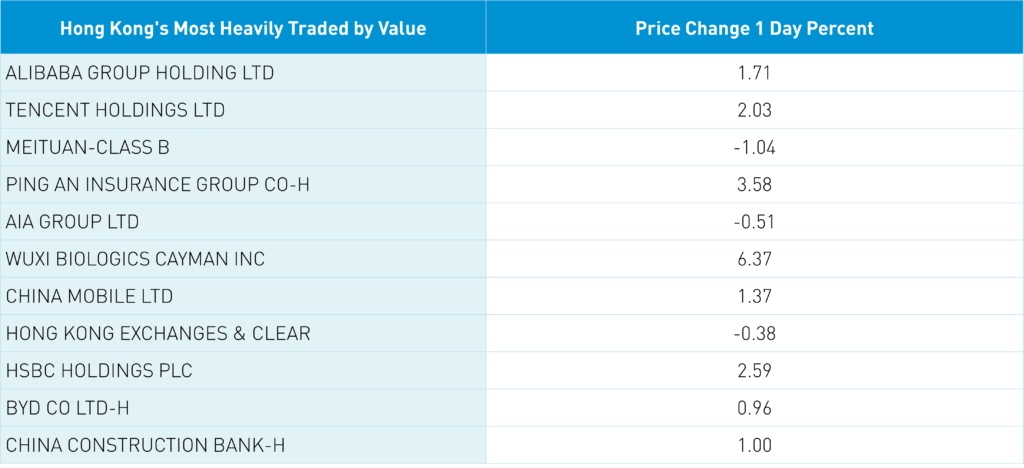

Hong Kong’s most heavily traded by value were Alibaba HK, which gained +1.71% on news it would work on smart car technology with Geely Automobile (175 HK), which fell -0.98%, Tencent +2.03% on net buying from Mainland investors, and Meituan -1.04% as US dual listed internet and electric vehicle (EV) companies along with growth plays had a strong day. Hong Kong reopening plays like Macao casinos and airlines had a good day. All sectors in Hong Kong were positive, less so utilities while advancing stocks beat decliners nearly 4 to 1. The healthcare sector in Hong Kong gained +4.6%, led by Wuxi Biologics Cayman (2269 HK), as two analysts raised their ratings/price target. Main Board's short volume increased to 17% of turnover as Alibaba’s short turnover was 23% of the total turnover, NetEase 32%, and Tencent's 17%. All sectors in China were up today as value factors outperformed.

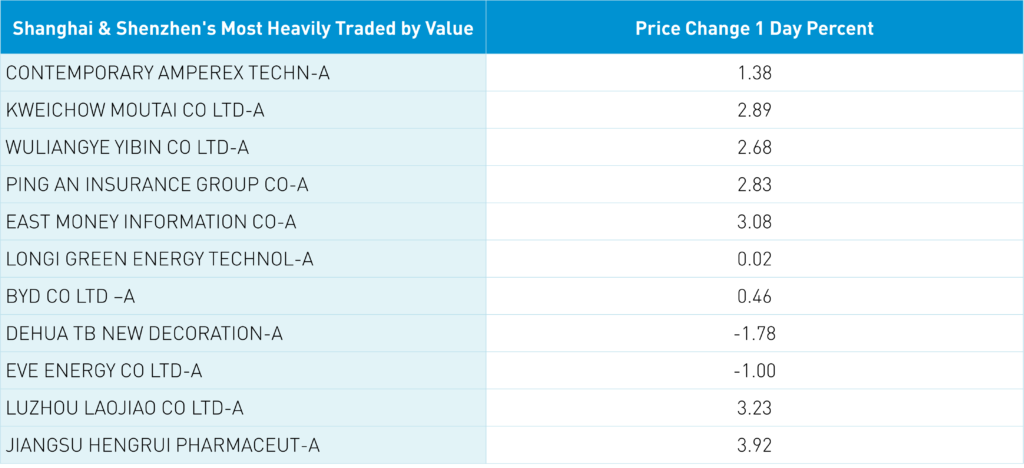

In China, talk that the PBOC will pump liquidity into the financial system in advance of Chinese New Year helped sentiment. Mainland’s most heavily traded were CATL +1.38%, Kweichow Moutai +2.89%, Wuliangye Yibin +2.68%, Ping An Insurance +2.83%, East Money +3.08%, LONGi Green Energy +0.02%, and BYD +0.46%. These are growth stocks favored by domestic and foreign investors though I would argue you don’t need an active manager to buy them! Foreign investors bought $1.984 billion of Mainland stocks via Northbound Stock Connect with a weekly total to a very large $6.519 billion. Semis were an outlier falling for the day as US meetings with Japan and the Netherlands to curb technology exports to China weighed on the space. Strong day and week!

Two Chinese airlines have stated they will delist from the NYSE. Sounds bad, right? Wrong! The two companies are State Owned Enterprises that contain sensitive information that could be revealed in an audit review conducted by the PCAOB. The PCAOB is part of the SEC i.e., the US government, in a move that we’ve seen from other SOEs. It shows that private companies are being allowed to adhere to the HFCAA. This is good news!!!

The Hang Seng and Hang Seng Tech indexes gained +1.04% and +1.51%, respectively, on volume that decreased -16.65% from yesterday, which is 106% of the 1-year average. 388 stocks advanced, while 104 stocks declined. Main Board short turnover decreased -11.56% from yesterday, which is 103% of the 1-year average as 17% of turnover was short turnover. Growth factors outperformed value factors, while small caps outpaced large caps. The top-performing sectors were healthcare +4.6%, staples +2.26%, and communication +2.12% while utilities was the only negative sector -0.32%. The top-performing subsectors were pharma/biotech, healthcare equipment, and media, while semis, food/staples, and utilities. Southbound Stock Connect volumes were light as Mainland investors bought $261 million of Hong Kong stocks, with Tencent a moderate buy, BYD a small net buy, and Meituan and Li Auto were small net sells.

Shanghai, Shenzhen, and STAR Board gained +1.01%, +0.9%, and +0.01%, respectively, on volume that increased +3.27% from yesterday, which is 77% of the 1-year average. 2,796 stocks advanced, while 1,808 stocks declined. Value factors outperformed growth factors as large caps barely edged out small caps. All sectors were positive, with consumer staples +3.33%, healthcare +3.01%, and financials +2.17% with tech +0.36%. Top sub-sectors were soft drinks, household products, and diversified financials while power generation equipment, gas industry, and communication equipment. Northbound Stock Connect volumes were light/moderate as foreign investors bought $1.984 billion of Mainland stocks. CNY had a strong move versus the US dollar, +0.17%, closing at 6.72, Treasury bonds sold off, and Shanghai copper gained +0.26%.

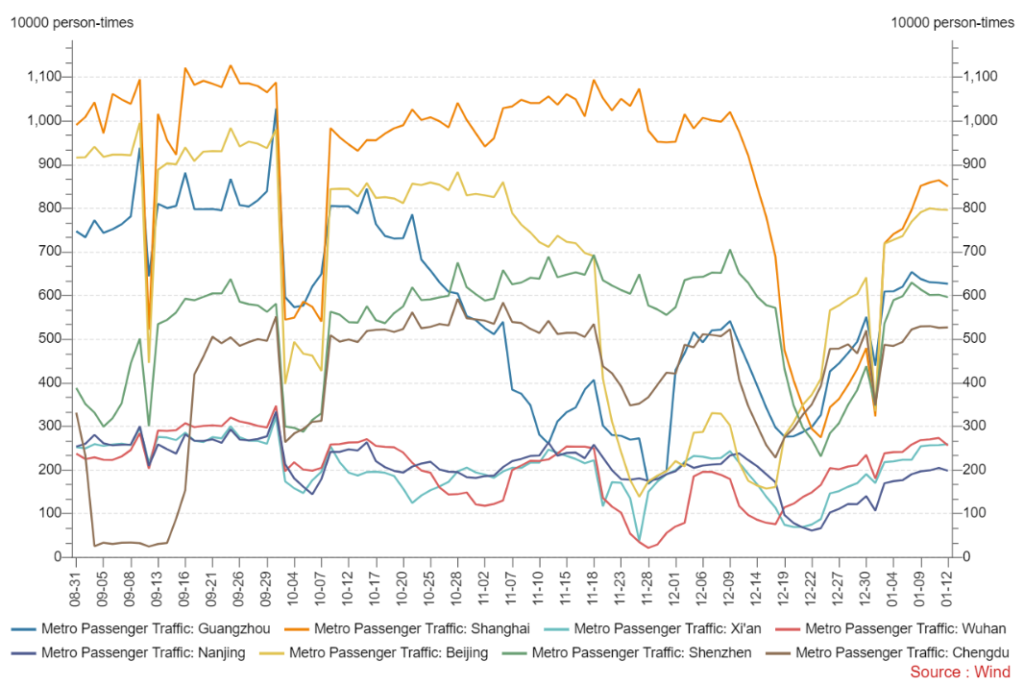

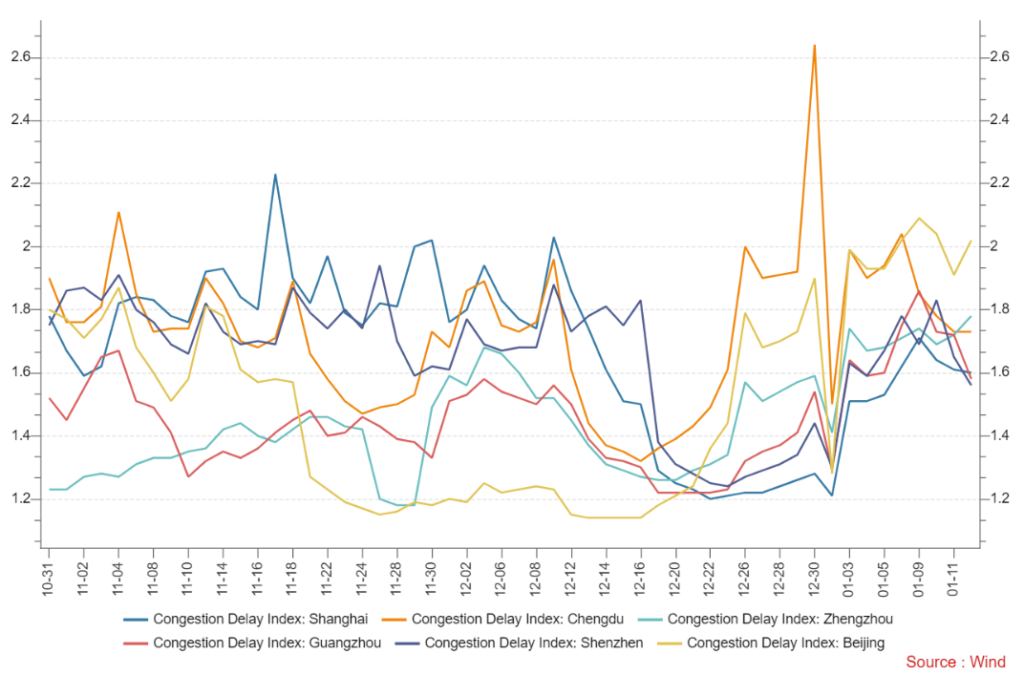

Major Chinese City Mobility Tracker

The trend continues to improve. Although traffic in Shanghai and Chengdu has rolled over, metro use remains steady in both cities. The Spring Festival/Chinese New Year travel is starting to pick up, though the market is open as a Mainland media source noted 37.88 million people traveled on just the fifth day. COVID cases continue to increase rapidly in several provinces.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.72 versus 6.75 yesterday

- CNY per EUR 7.26 versus 7.27 yesterday

- Yield on 10-Year Government Bond 2.90% versus 2.88% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.00% yesterday

- Copper Price +0.26% overnight