Foreign Investors Buy China in Size

2 Min. Read Time

Key News

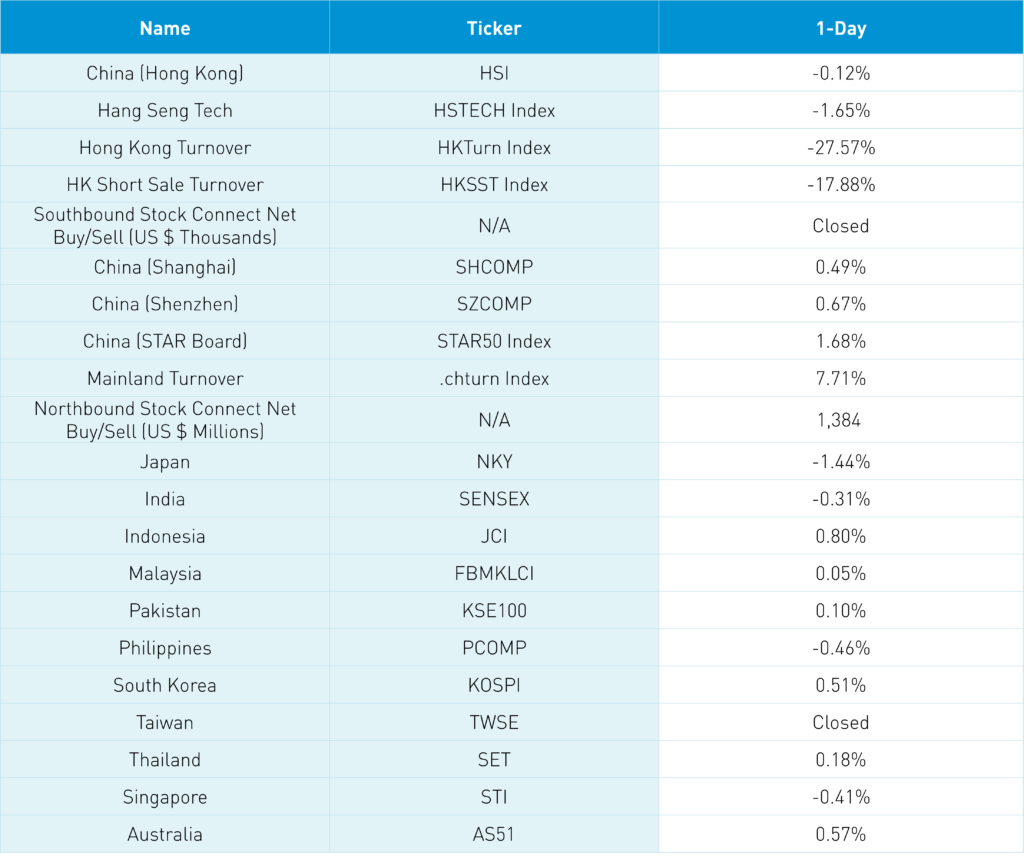

Asian equity markets were mixed as China, South Korea, and Indonesia outperformed while Hong Kong, Japan, India, and the Philippines were lower.

Shanghai and Shenzhen gained +0.49% and +0.67%, with the former clearing the 3,200 index level last week while Shenzhen closed above 2,100 overnight for the first time since mid-September. The STAR Board gained +1.68% overnight though it lags the Shanghai and Shenzhen. One factor is that most STAR Board stocks aren’t readily available via Northbound Stock Connect. Foreign investors bought $1.386B of Mainland stocks overnight, bringing the year-to-date total to $13.223B, exceeding the total for all of 2022! There are investors out there allocating to China in size!

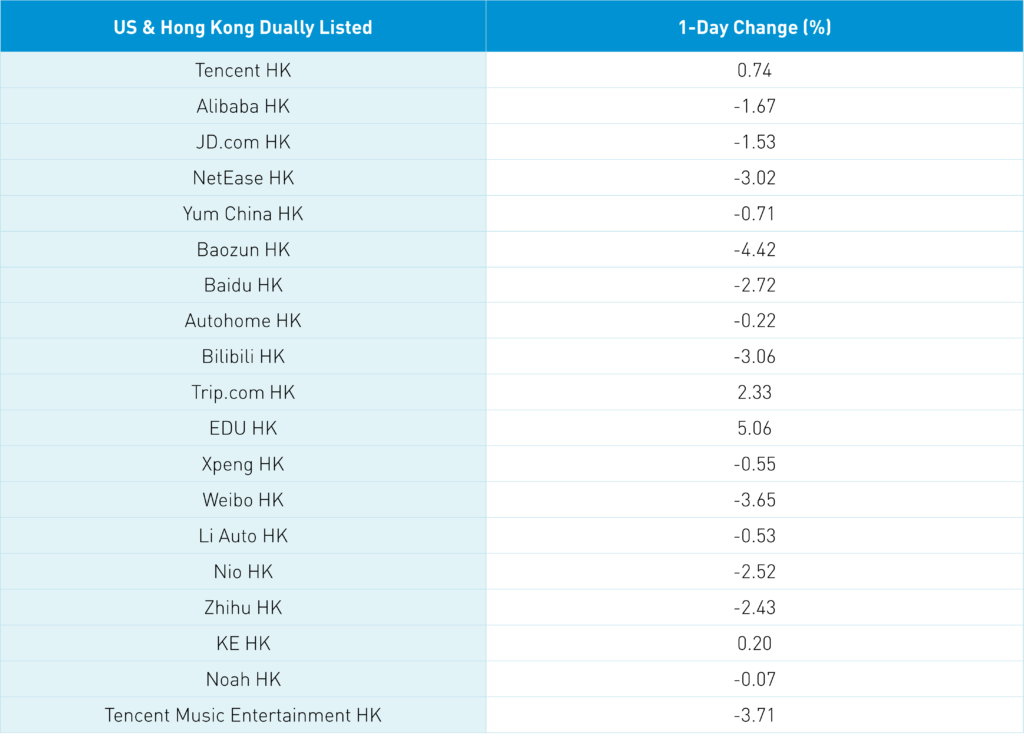

For the second day in a row, Hong Kong was after a rough day for US-China ADRs but didn’t fall as much. The Hang Seng and Hang Seng Tech were off -1.36% and -2.46% at intra-day lows but grinded higher, closing off -0.12% and -1.65%. A factor in US-China ADRs weakness was one story from a Mainland media source that the Chinese government would create a ride-hailing app that would compete with Full Truck Alliance and Didi. Many media sources pushed the story out, which hit the stocks hard. Via Twitter (ahern_brendan), I voiced my skepticism on this story as the sell-off spread to other China ADRs. This morning we have clarification from the Ministry of Transportation that they aren’t involved in the app. A factor is some profit taking before the Lunar New Year as Hong Kong’s most heavily traded were Tencent +0.74%, Alibaba HK -1.67%, Meituan -2.08, Kuaishou -6% on a big insider sell, BYD +2.26% on strong sales thus far in January and JD.com HK -1.53%. Southbound Stock Connect was closed today as volumes fell -27% from yesterday. This is why China ADRs should still relist in Hong Kong, as 1/3 of Hong Kong volume comes from investors in China.

Internet companies are having pre-quiet period conference calls with analysts before Q4 financial results in February. The key will be their outlook for Q1 and Q2 based on China’s reopening. Thus far, companies sound constructive in their outlook! Foreign direct investment in China increased +6.3% in 2022, according to a release overnight.

The Hang Seng and Hang Seng Tech fell -0.12% and -1.65% on volume -27.57% from yesterday, which is 73% of the 1-year average. 246 stocks advanced, while 244 stocks declined. Main Board short turnover declined -17.98% from yesterday, 73% of the 1-year average, as 17% of total turnover was short turnover. The top sectors were real estate -2.67%, materials +1.06%, and healthcare +0.79%, while energy -1.71%, tech -0.89%, and discretionary -0.86%. The top sub-sectors were consumer services, real estate, and diversified financials, while media, retailing, and food/staples were among the worst. Southbound Stock Connect was closed today.

Shanghai, Shenzhen, and STAR Board gained +0.49%, +0.67%, and +1.68% on volume +7.71% from yesterday, which is 75% of the 1-year average. 3,221 stocks advanced, while 1,349 stocks declined. The top sectors were communication +1.45%, healthcare +1.33%, and tech +1.24%, while utilities -1%, staples -0.89%, and industrials -0.51%. The top sub-sectors were office supplies, software, and pharma, while the forest industry, airports, and soft drinks were among the worst. Northbound Stock Connect volumes moderate/light as foreign investors bought $1.384B of Mainland stocks. CNY sold off -0.4% versus the US dollar closing at 6.78, Treasury bonds rallied, and Shanghai Copper +0.92%.

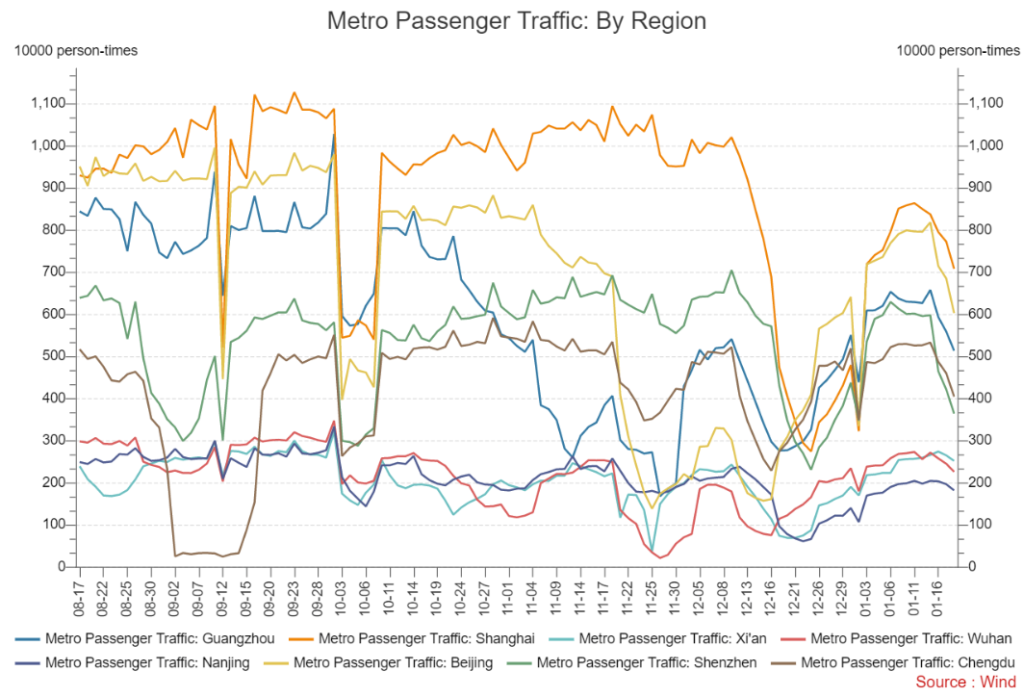

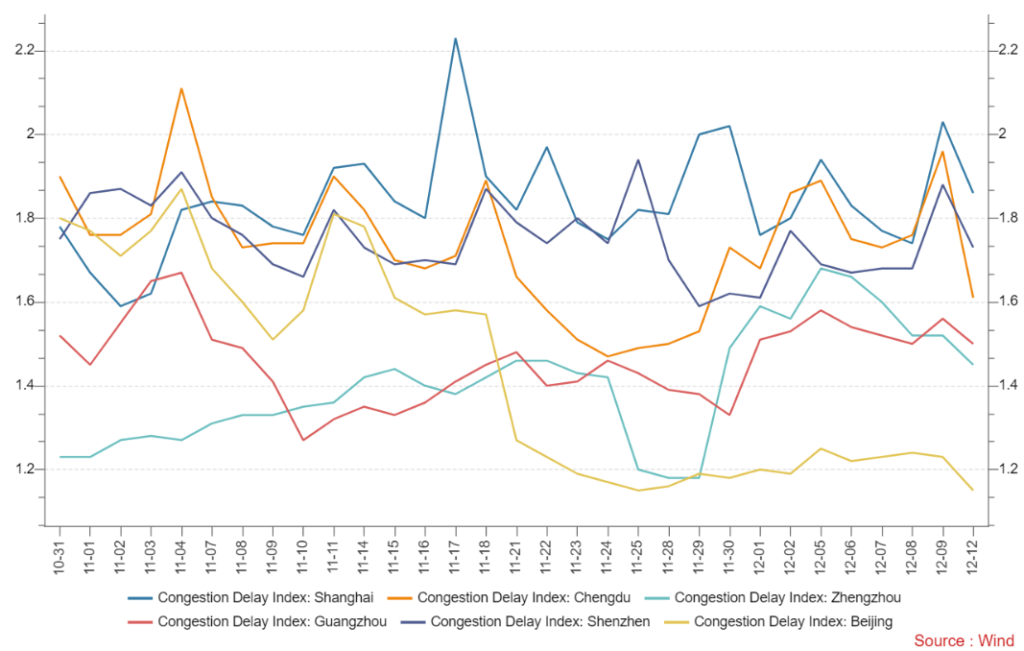

Major Chinese City Mobility Tracker

Subway and traffic are falling as people head on vacation for the Lunar New Year.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.79 versus 6.75 yesterday

- CNY per EUR 7.34 versus 7.32 yesterday

- Yield on 10-Year Government Bond 2.92% versus 2.92% yesterday

- Yield on 10-Year China Development Bank Bond 3.08% versus 3.08% yesterday

- Copper Price +0.92% overnight