Trip.com Financial Results Provide Important Insight into China’s Reopening

3 Min. Read Time

Key News

Asian equities were higher overnight, with China and Hong Kong underperforming. India was off for Holi, which celebrates the arrival of spring according to Google.

February trade data was cited as the culprit as imports year-to-date (YTD) fell -10.2% versus expectations of -5.5%, exports were lower -6.8% versus expectations of -9%, and trade balance of $116 billion versus expectations of $82.5 billion. Not all bad right? President Xi gave a speech highlighting the importance of China’s private sector. Trip.com’s (TCOM US, 9961 HK) better than expected Q4 financial results and strong outlook on China’s reopening didn’t improve sentiment overnight despite positive indications of China’s economy in 2023. TCOM’s results are covered in-depth below.

The Asia dollar index fell overnight, though China’s renminbi was off more falling to 6.94. We are in lull during the Dual Sessions with little significant news, still Mainland China’s decline is surprising. New Foreign Minister and ex China Ambassador Qin Gang’s first press conference had critical comments about the US. Worth noting that China exported $71 billion to the US and imported $30 billion of US goods highlighting how well businesspeople are getting along with one another.

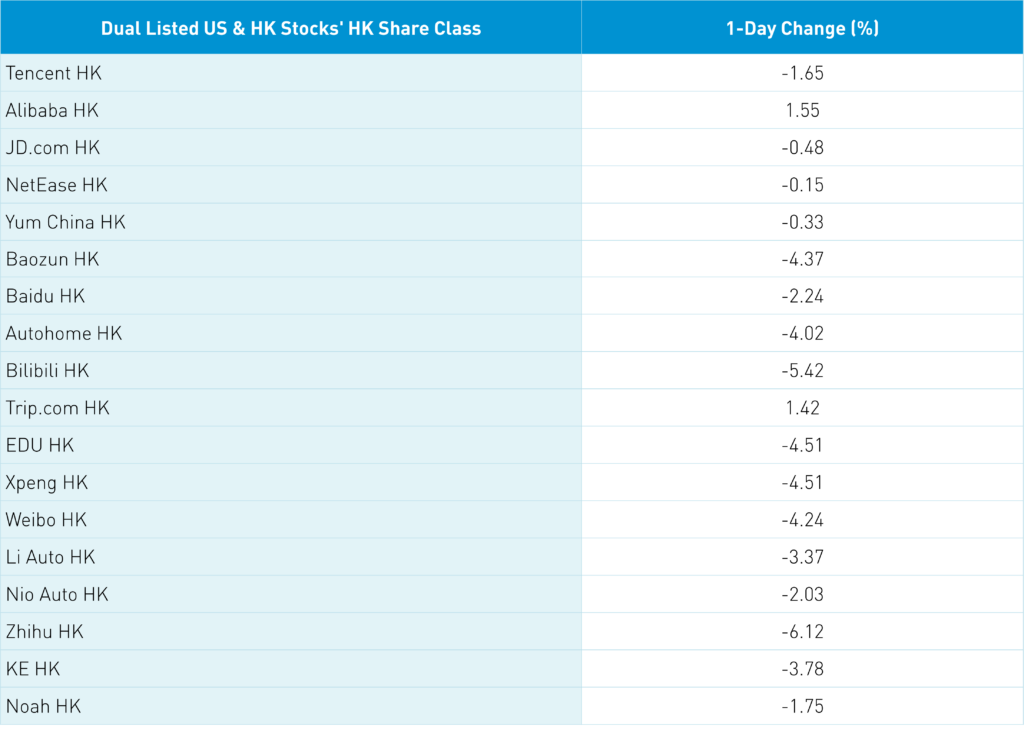

Hong Kong’s most heavily traded were Tencent -1.65%, Alibaba HK +1.55%, Meituan -3.5% after back tracking on getting into Uber like taxicab hailing, energy giant CNOOC +3.34%, and China Mobile -2.73%. The Hang Seng Index closed at 20,534 above the 20k level which will be important to watch. Hong Kong short turnover has been light which may confirm the thesis we are in a bit of a lull before we have specific economic policies outlined. Stock Connect flows, both Northbound and Southbound, were small net outflows. Mark Mobius confirmed comments on not being able to get his money out of China were resolved and more importantly didn’t involve investments in China but a bank account.

Trip.com reported Q4 financial results after the US close. The company didn’t bury the headline stating “The domestic business in China remained resilient and the international business continued to show strong recovery momentum. Outbound air-ticket bookings and hotel bookings increased by over 200% and 140% year-over-year in the fourth quarter, respectively. Overall air-ticket bookings on the Company's global platforms grew by 80% year-over-year in the fourth quarter.” Management did a great job keeping expenses down as the company faced the headwind of COVID running rampant in Q4 2022. The key is the company’s positive forward-looking views on China’s reopening and resumption of China’s love for travel. International travel has been limited as airlines are running at 15% to 20% of pre-COVID capacity. However, expectations are that by the end of June, airlines should be at 50% capacity and 80%/90% by year end. Despite the limited capacity, volume is up 40% of pre-COVID levels. Pre-COVID there were 150 million Chinese took overseas trips annually.

Revenue increased +7% year-over-year to RMB 5.031 billion ($730 million) versus analyst expectations of RMB 4.861 billion and Q4 2022’s RMB 4.682 billion.

Adjusted Net Income of RMB 498 million ($71 million) versus analyst expectations of RMB -152 million and Q4 2022’s loss of RMB -834 million.

Adjusted EPS of RMB 0.76 ($0.11) versus analyst expectations of a loss of RMB -0.25 and Q4 2022’s RMB 0.48.

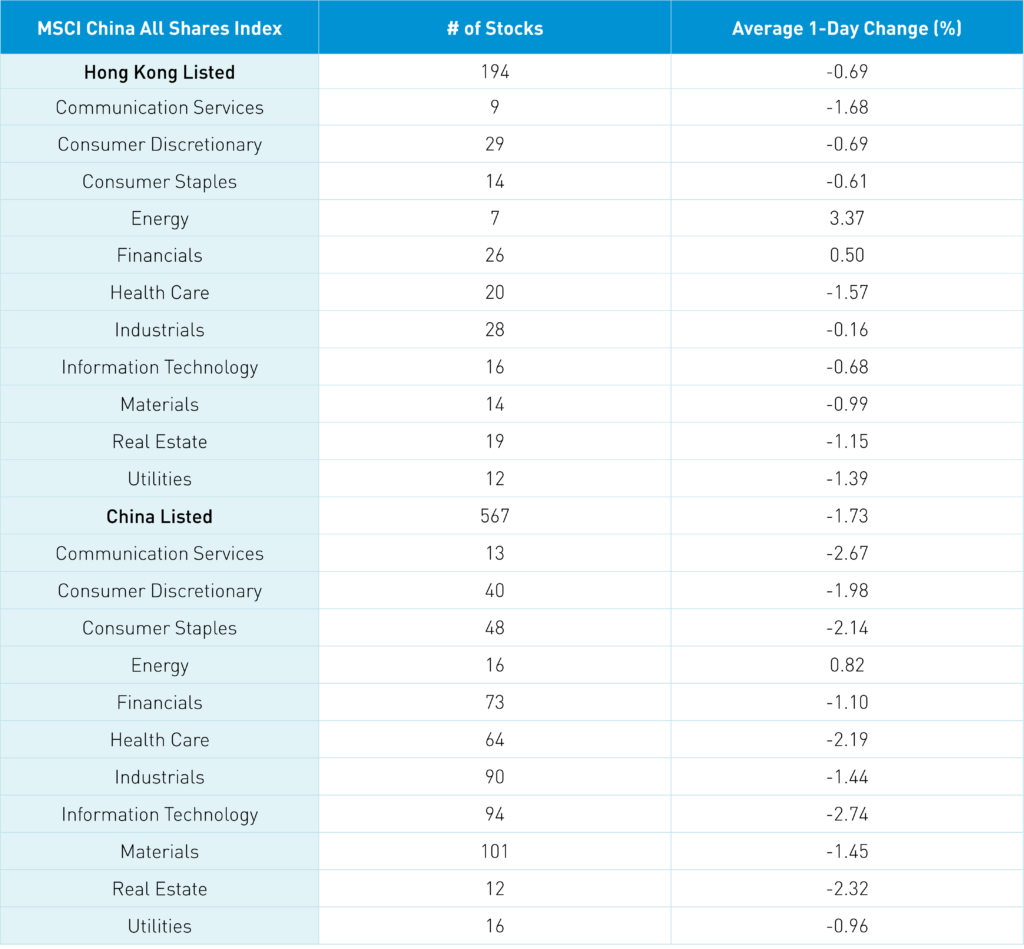

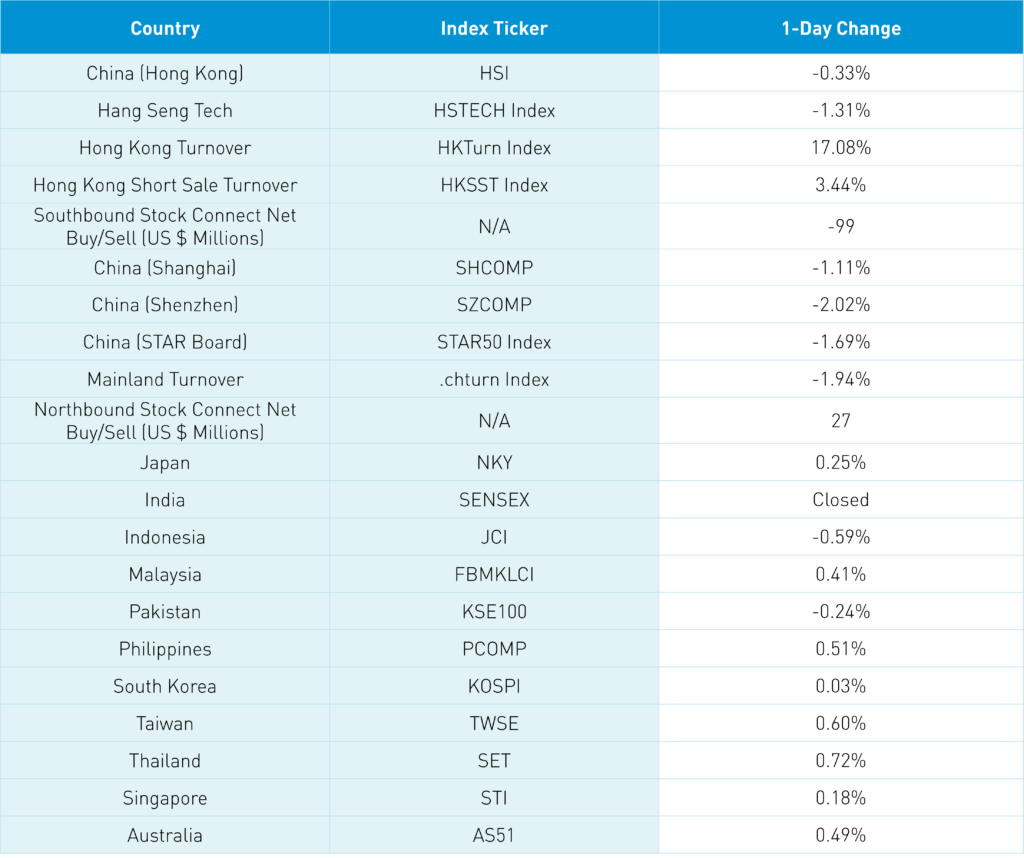

The Hang Seng and Hang Seng Tech fell -0.33% and -1.31% respectively on volume +17.08% from yesterday which is 102% of the 1-year average. 119 stocks advanced while 374 stocks declined. Main Board short turnover increased +3.43% from yesterday which is 86% of the 1-year average as 15% of turnover was short turnover. Value factors outpaced growth factors as large caps outperformed small caps. Energy and financials were the only positive sectors gaining +3.37% and +0.5% while communication fell -1.68%, healthcare closed lower -1.57%, and utilities ended -1.39%. Top sub-sectors were energy, banks, and capital goods while telecom services, household products, and media were the worst. Southbound Stock Connect volumes were light/moderate as Mainland investors sold -$99 million of Hong Kong stocks with Tencent a small net buy, Meituan a moderate net sell, and Kuiashou a small net sell.

Shanghai, Shenzhen, and STAR Board fell -1.11%, -2.02%, and -1.69% on volume -1.94% from yesterday which is 103% of the 1-year average. 412 stocks advanced while 4,453 stocks declined. Value factors “outperformed” as they fell less than growth factors and large caps “outperformed” small caps. Energy was the only positive sector gaining +0.79%, while tech -2.77%, communication -2.71%, and real estate -2.36%. Top sub-sectors were oil/gas, energy equipment, and precious metals while communication equipment, telecom, and computer hardware were the worst. Northbound Stock Connect volumes were moderate as foreign investors sold -$27 million of Mainland stocks today. CNY fell -0.14% versus the US dollar to 6.94, Treasury bonds rallied, while copper fell, and steel gained.

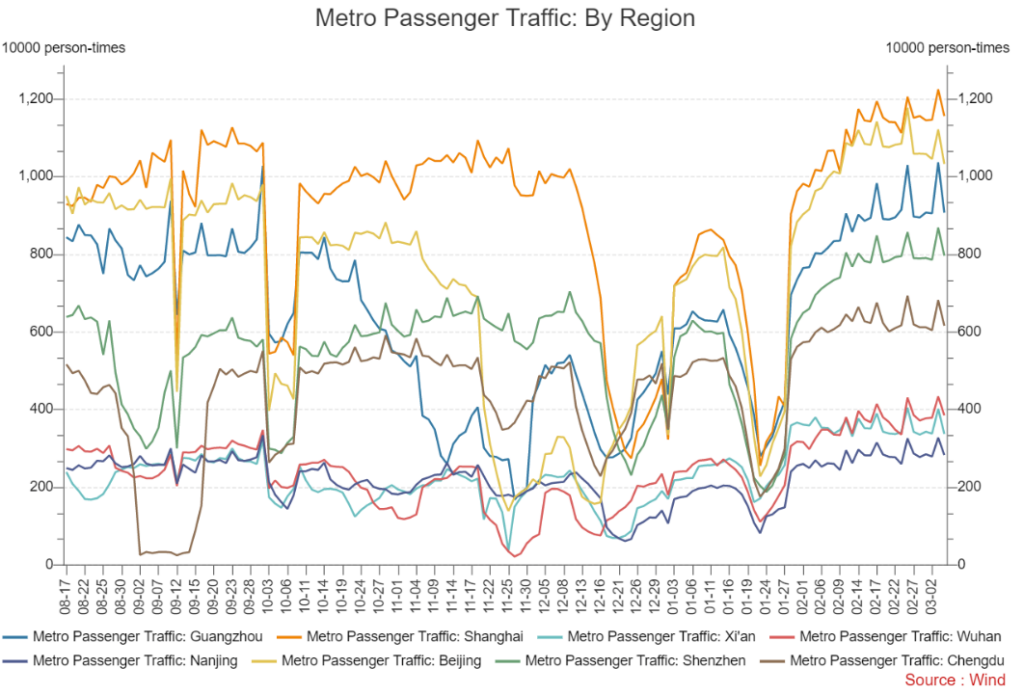

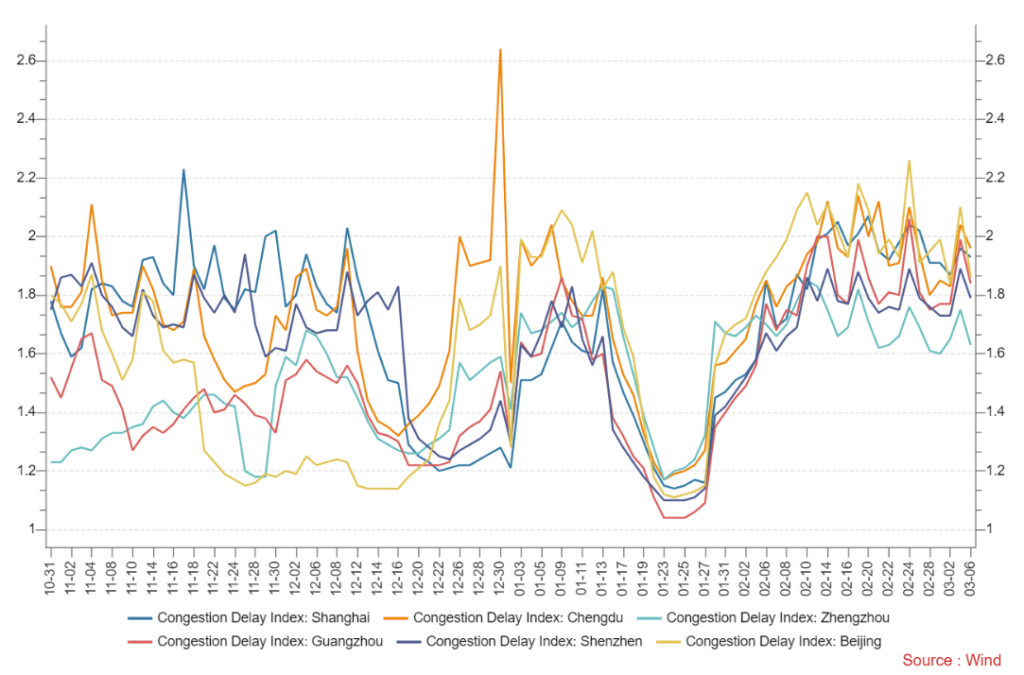

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.94 versus 6.93 yesterday

- CNY per EUR 7.39 versus 7.40 yesterday

- Yield on 10-Year Government Bond 2.87% versus 2.88% yesterday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.07% yesterday

- Copper Price -0.62% overnight

- Steel Price +0.54% overnight