Positive Economic Data and Important News from Alibaba & Baidu As Markets Face European Bank Headwind

3 Min. Read Time

Key News

Asian equity markets rebounded overnight, less so India, as Silicon Valley Bank (SVB) contagion fears receded. This morning, European markets and banks sold off significantly.

The Asia Dollar Index and CNH, China’s currency that trades during US hours, are off -0.48% and -0.46% on Europe’s sell off. It is a shame as there were positive catalysts overnight, specific to Hong Kong and China, which lifted stocks. Volumes were light, indicating investors were cautious post-SVB and Fed hike uncertainty, though Hong Kong breadth swung from awful yesterday to great today.

Hong Kong Main Board short turnover increased as percentage of turnover to 19%, the highest level seen of late, though light total Hong Kong volumes were a factor.

The 1-year Medium-Term Lending Facility (MLF) rate was unchanged at 2.75% though the PBOC did add liquidity to the financial system.

Due to Chinese New Year occurring in January this year and February last year, January and February economic data was reported together on a year-to-date basis. Year-to-date as of February, retail sales have increased 3.5% year-over-year (YoY) versus expectations of 3.5%, fixed asset investment (FAI) increased 5.5% versus expectations of 4.5%, Property Investment fell -5.7% YoY versus expectations of -8.5%, and residential property sales increased 3.5% YoY. Industrial Production was a miss at +2.4% versus expectations of 2.6%. Within retail sales, online retail sales of physical goods increased by 5.3% YoY while convenience stores and specialty stores increased 10% and 3.6% YoY, restaurants sales increased +9.2%, though auto fell -9.4%, and household electronics decreased -1.9%.

The National Bureau of Statistics stated “the recovery trend of the consumer in January-February is relatively good. However, we also see that residents’ willingness to consume still needs to be enhanced, consumption conditions need to be improved… relevant policies to promote consumption will continue....”. Slow and steady with a hint of policy support coming. A Mainland media source highlighted retiring Premier Li Keqiang’s NPC speech on March 5th that focused on eight key economic areas including “expanding domestic demand, prioritize the recovery and expansion of consumption” driven by “government investment and policy incentives”. We had another reiteration of SOE reform and a commitment to “expand market access” with “equal treatment of foreign-invested enterprises.” He also mentioned stopping economic and financial risks, calling out real estate and local government debt. Renewable energy was also emphasized, as the goal is to “accelerate the development of a new energy system”.

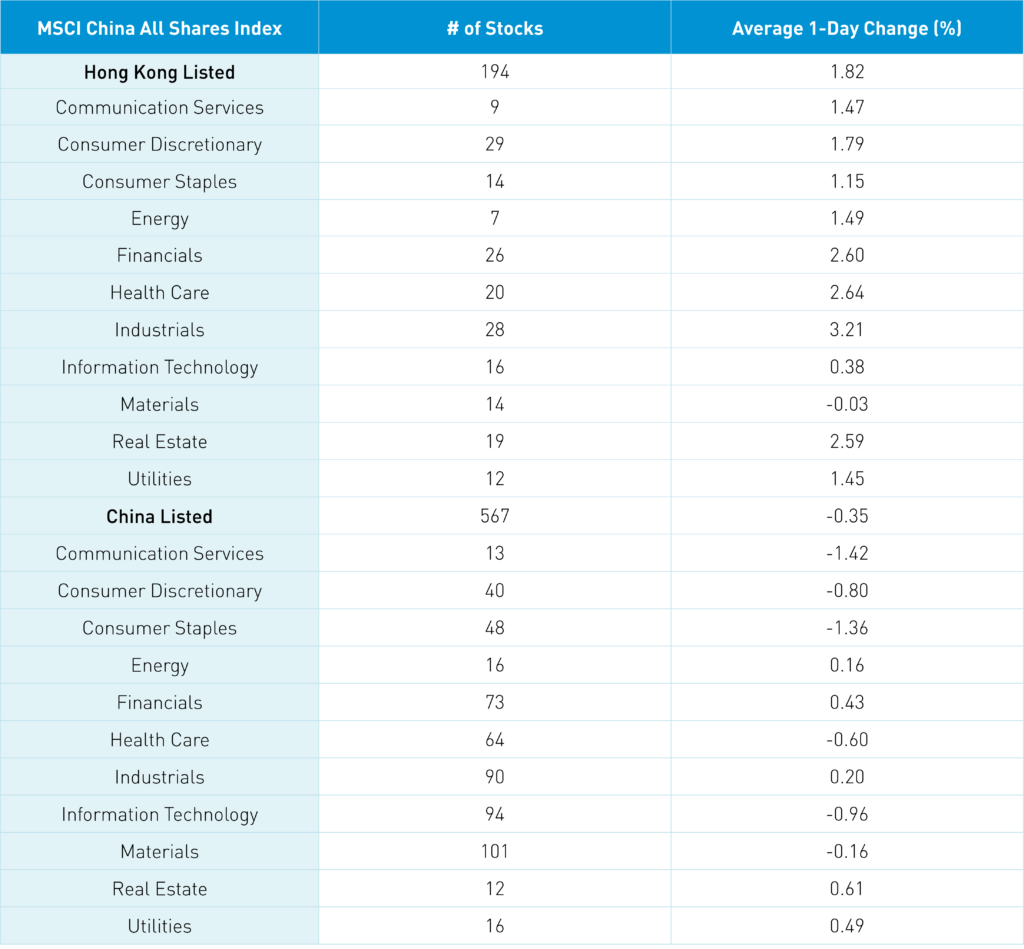

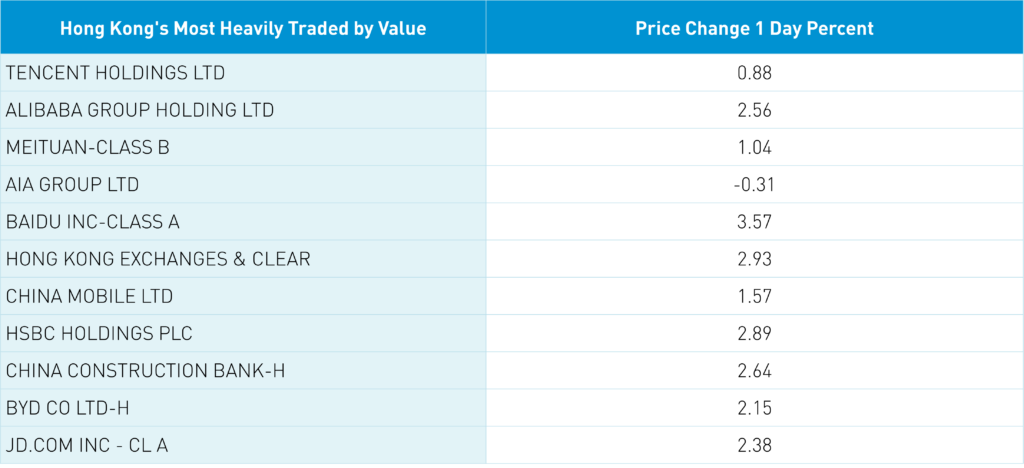

Hong Kong’s most heavily traded stocks by value were Tencent, which gained+0.88%, Alibaba, which gained +2.56%, Meituan, which gaind+1.04%, AIA, which fell -0.31%, and Baidu, which gained +3.57%. Alibaba’s local government regulator signed a well-publicized agreement on the platform economy, which should put to rest any lingering concerns on China’s internet regulation. For the naysayers, you can’t get more public than what just occurred.

Tomorrow, Baidu’s CEO Robin Li and Chief Technology Officer Haifeng Wang will hold a press conference on AI conservation powered ERNIE Bot. The launch could help jump start the company’s dominant search business by drawing in more advertising dollars. Tencent was a significant net buy from Mainland investors via Southbound Stock Connect. Shanghai and Shenzhen posted small gains as SOE reforms lifted value stocks/sectors while protecting real estate made it the best performer in China. Growth names that outperformed yesterday saw profit taking as STAR Board was off -0.6%. Foreign investors bought a healthy $475 million of Mainland stocks today.

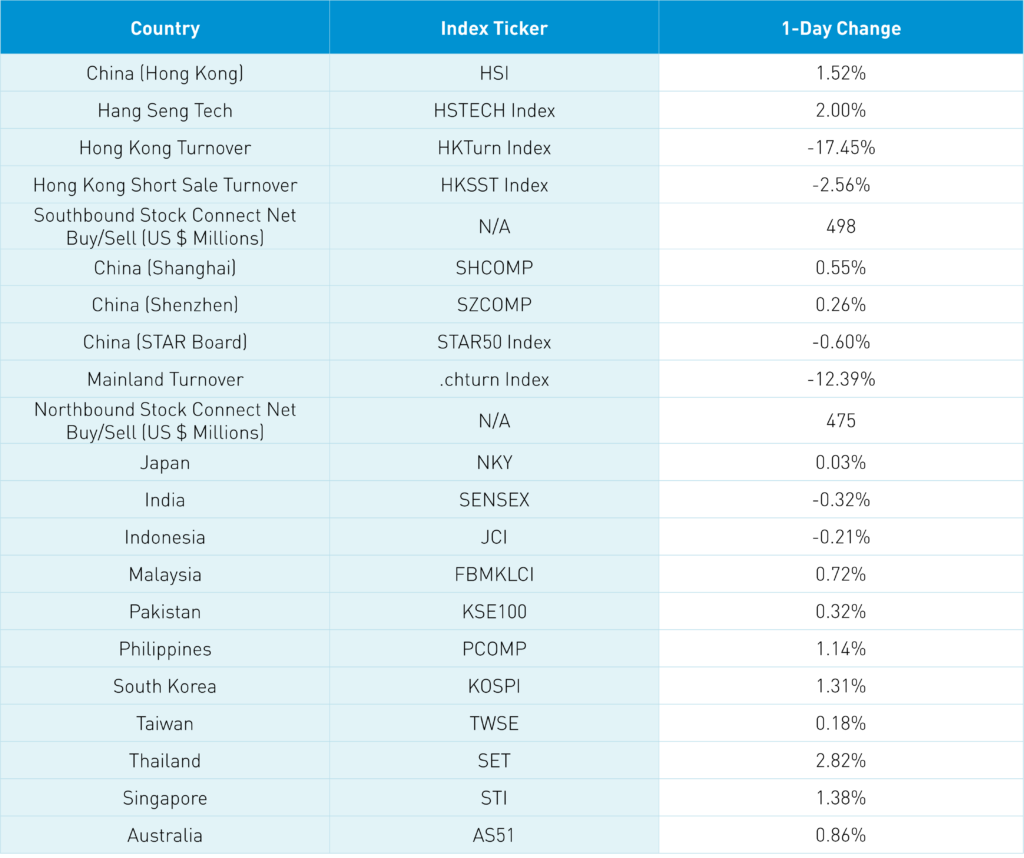

The Hang Seng and Hang Seng Tech gained +1.52% and +2% respectively on volume that decreased -17.45% from yesterday, which is 87% of the 1-year average. 415 stocks advanced, while 89 stocks declined. Main Board short turnover declined -2.57% from yesterday, which is 95% of the 1-year average as 19% of turnover was short. Value and growth factors performed well as the former outpaced the latter, while small caps outpaced large caps. The top-performing sectors were industrials, which gained+3.21%, healthcare, which gained +2.64%, and financials, which closed higher by +2.6%. Meanwhile, materials was the only down sector closing down -0.03%. Top sub-sectors were household products, capital goods, and healthcare equipment while technical hardware was the only negative sub-sector. Southbound Stock Connect volumes were light as Mainland investors bought $498 million of Hong Kong stocks with Tencent a large buy, Kuiashou a small net buy, and Meituan a small net sell.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.55%, +0.26%, and -0.6%, respectively, on volume that decreased -12.39% from yesterday, which is 91% of the 1-year average. 3,462 stocks advanced while 1,262 stocks declined. Value factors outperformed growth factors as large caps outperformed small caps. The top-performing sectors were real estate, which gained +0.64%, utilities, which gained +0.51%, and financials, which gained +0.46%. Meanwhile, communication was down -1.4%, consumer staples closed lower by -1.33%, and technology was down -0.93%. The top-performing subsectors were the marine industry, construction industry, and port industry, while software, catering/tourism, and liquor were the among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors bought $475 million of Mainland stocks. CNY fell -0.44% versus the US dollar to close at 6.90 CNY per USD, The treasury curve flattened, while Shanghai copper gained +0.76% and steel fell -0.3%.

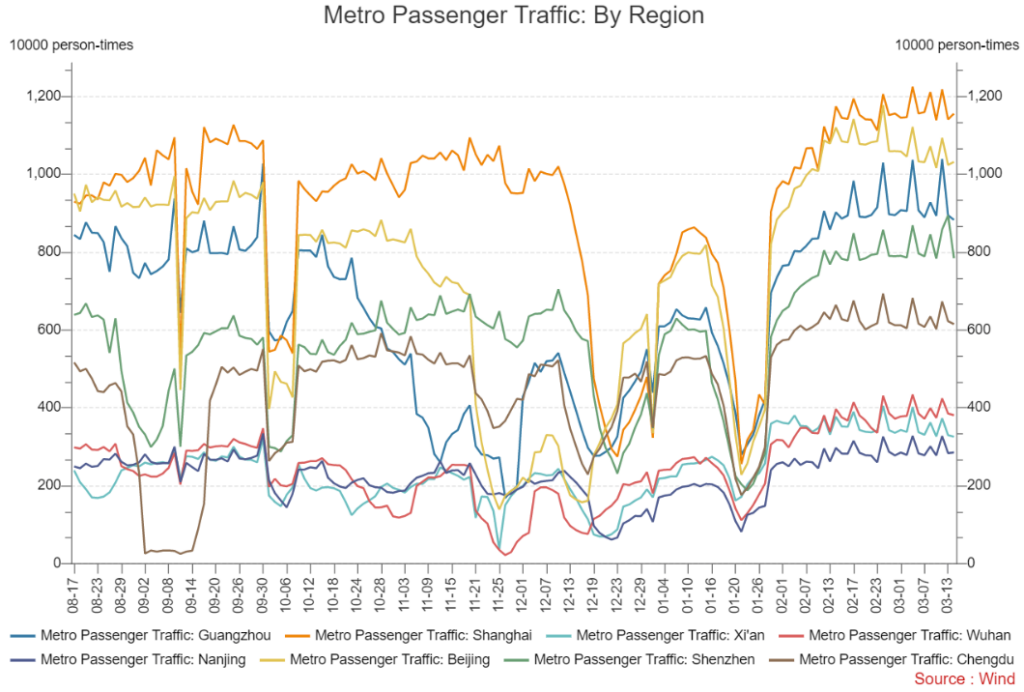

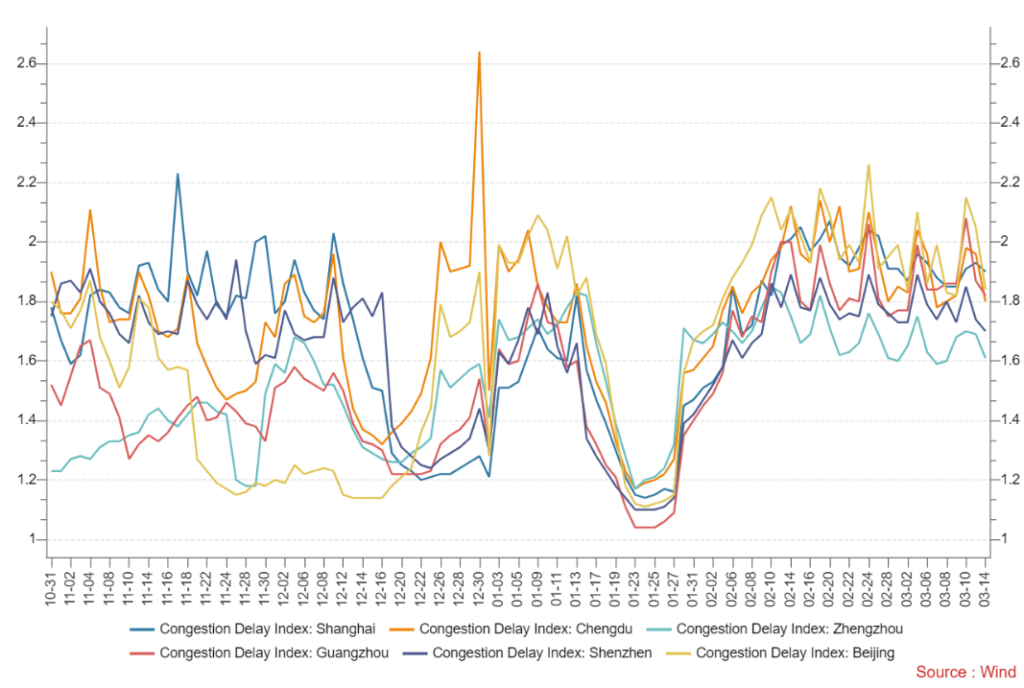

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.90 versus 6.88 yesterday

- CNY per EUR 7.36 versus 7.37 yesterday

- Yield on 10-Year Government Bond 2.86% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.06% yesterday

- Copper Price +0.76% overnight

- Steel Price -0.30% overnight